Stocks are steadying in the early going ahead of some potentially market-moving events. Gold and silver are rebounding, while the dollar is dropping notably. Crude oil is stable around $70 a barrel.

It’s “Tariff Eve,” with 25% levies set to take effect on Canadian and Mexican imports tomorrow. China’s tariff rate will also double to 20%. All told, tariffs could apply to around $1.5 TRILLION in annual imports barring a last-minute deal. Europe could be next in the line of fire, too.

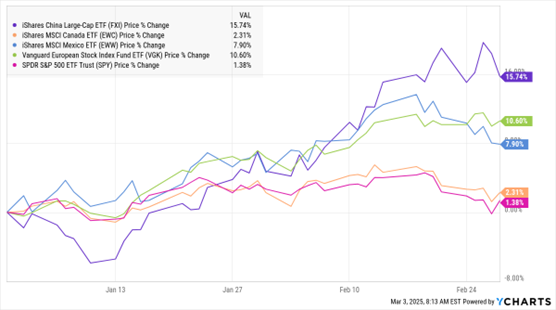

The targeted nations have said they would retaliate with tariffs on US exports, including US agricultural and food products in the case of China. Ironically, markets in many of the countries targeted by tariffs are outperforming markets in the US. The chart below shows the performance of ETFs that track stocks in China, Canada, Mexico, and Europe – along with the SPDR S&P 500 ETF (SPY).

FXI, EWC, EWW, VGK, SPY (YTD % Change)

Following a rough stretch of economic data, the February jobs report is set to be released at the end of this week. Economists think the unemployment rate will hold steady at 4%, while job creation will increase to 153,000. Any disappointment on either front could lead to increased bets on Federal Reserve interest rate cuts. Bond investors haven’t been looking for aggressive moves lately due to stalled progress on inflation.

President Trump gave cryptocurrency investors some (fleeting) relief over the weekend by pushing the idea of a Crypto Strategic Reserve again. The president suggested Sunday that any reserve could include other tokens like XRP, SOL, and ADA in addition to widely expected cryptos like Bitcoin and Ethereum.

Many cryptos surged on the news yesterday, though they gave back a chunk of those gains today. The administration’s crypto czar Davis Sacks is hosting a meeting with Trump and several industry executives this Friday.