Converting a covered call trade to a collar trade can help maintain opportunity while locking in some unrealized profits, explains Alan Ellman.

When we sell an in-the-money or at-the-money strike and share price moves up substantially, we have an unrealized maximum return. While we can simply take a profit, there is a better choice for greater profits by converting this position to a collar trade.

On April 5, 2019, a subscriber (Doug) wrote to me about such a situation he was in with Alexion Pharmaceuticals, Inc. (ALXN). He was considering buying a protective put to protect part of the unrealized profit and thought that this would be a better approach than closing both legs of the covered call trade. If a protective put is added to a covered call trade, it is then considered a collar trade where the call limits share value appreciation and the put limits share loss to the downside.

Doug’s (my subscribers) trades

- 3/15/2019: Buy 100 x ALXN at $135.18

- 3/15/2019: Sell-to-open 1 x $135.00 4/18/2019 call at $5.11

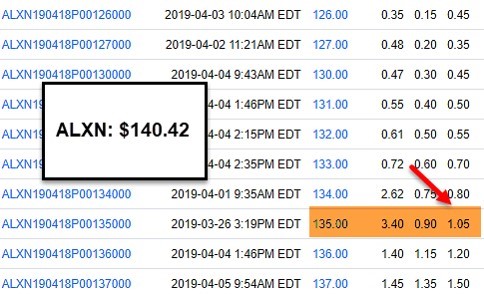

- 4/4/2019: ALXN trading at $140.42

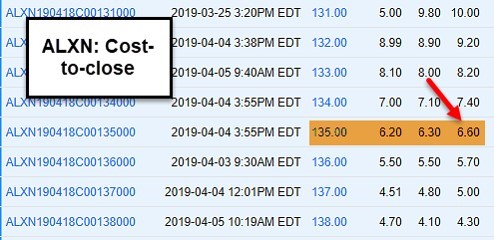

- 4/4/2019: The cost-to-close the $135.00 short call is $6.60

- 4/4/2019: The cost to buy a $135.00 protective put is $1.05

Doug’s initial time value return (ROO) using the multiple tab of The Ellman Calculator

Initial Calculations

The yellow cell shows an initial one-month time value return of 3.7%. Since this is a near-the-money strike, there is no upside potential and negligible (0.1%) downside protection.

The option chain below shows the cost of a protective put.

Put Option Chain

The brown-highlighted row shows an ask price of $1.05 for the $135 protective put. Calculations for collar trades will be facilitated by using the BCI Collar Calculator.

Calculations and the decision-making process

Protective put: $1.05 presents about 0.8% of our initial investment, lowering our returns from 3.7% to 2.9%, not bad.

The option chain below shows the cost-to-close the $135 short call.

Cost-To-Close Option Chain

The brown cell shows an ask price of $6.60. With the stock trading at $140.42, the intrinsic value of this premium is $5.42, leaving the time-value cost-to-close at $1.18 ($6.60 – $5.42). The time-value cost-to-close is $13 per contract greater than the cost of the protective put. Since we are currently mid-contract with two weeks remaining until expiration, closing the entire position (known as the mid-contract unwind exit strategy in the BCI methodology) at the cost of $13 per contract makes sense since we are in a position to generate more than $13 per contract by using this now freed up capital to enter a new position, with a new underlying, and generate a second income stream in the same contract month with the same cash investment.

Discussion

When a strike moves deep in-the-money, purchasing a protective put will definitely lock in a percentage of the current unrealized profit. As the time value approaches zero, the mid-contract unwind exit strategy may be an even better choice. There is also a third possible choice and that to take no action and continue to monitor our position. In this case, I would favor the mid-contract unwind exit strategy.

Use the multiple tab of the Ellman Calculator to calculate initial option returns (ROO), upside potential (for out-of-the-money strikes) and downside protection (for in-the-money strikes). The breakeven price point is also calculated.