War, unfortunately, is often bullish for stocks, writes Joe Duarte.

War, unfortunately, is often bullish for stocks. World War II was bullish for stocks. More recently, in 1991, the first Gulf War spawned an impressive bull market. And while investors made money on both wars, it should be noted that the Gulf War bull market was born after a mini-bear market in the late summer of 1990 took nearly 20% off of the major stock indexes, and WWII came in the wake of the Great Depression.

Flash forward to the early days of 2020, when sabers between Iran and the United States, with Iraq in the middle, are rattling. Moreover, in contrast to 1991 stocks are trading near the top of a bull market while the U.S. economy is showing signs of slowing.

Therefore, because this time may be different, investors should prepare for a bumpy ride while considering the following questions:

- Will there be a long term escalation of hostilities between the United States and Iran?

- Will this situation have meaningful negative effects on individual companies with stout products and management – and will the algos be able to discern the finer points of such a complex landscape?

- Can the Fed drain its recent liquidity flood from the system under the current circumstances?

- What happens if the currency markets decide to get volatile? And

- How with the algorithmic traders play this uncertain market situation?

We are likely to have some fairly clear answers in the next few days, but it is important to consider the fact that if the Markets-Economy-Life (MEL) system falls out of the edge of chaos where complex systems operate at their best, into chaos where events are predictably unpredictable, then all bets are off and little will make sense. If that’s the direction of events, the best course of action will be to move out of the markets into cash until things change.

Where Things Stand

Last week I noted: “as each day passes, it becomes clear that we are at the Edge of Chaos, a place from where things emerge and complex adaptive systems, such as the Markets-Economy-Life (MEL) ecosystem move on to their next level of complexity, which is often a surprisingly positive development.” I also noted, “Even in a cautiously optimistic analysis it is important to keep an eye on where unexpected negative events that derail markets may come from.”

And of course, right on cue, at the start of the 2020 election year, here we are on the verge of war with Iran.

Certainly, it is early in the U.S.-Iran situation and things could certainly get better or worse in a hurry, since these situations can be fluid. However, and this may be a temporary phenomenon, the first trading day after the escalation of what has been a simmering situation between the two countries could have been a lot worse. Nevertheless, this is not a time to be careless or cavalier. Instead, extreme watchfulness and planning is called for on the part of all investors.

Watch Out for the Fed and the Effect on MEL

Of course, no one knows how this will turn out. Only one thing is certain, whatever comes out of the actions that will be taken by the United States, Iran and other countries in the next few days will affect the Markets-Economy-Life (MEL) ecosystem.

One of the easier things to overlook when faced with a market that is reeling from a geopolitical crisis is the activity of the Federal Reserve. Indeed, the Fed has been very market friendly over the last few weeks pumping big money into the Repo market and seeming to have stopped what might have bee a major liquidity crisis. This liquidity infusion has been a big positive for stock prices over the last few weeks.

Unfortunately, the U.S. central bank is set to start draining liquidity from said market within days, which means that if they don’t change their mind, we could see another layer of worry added to the uncertainty of the U.S.-Iran situation. We’ll know early in the week as the Repo market data is revealed early in the mornings.

In other words, it is possible that on top of the rising mess in the Middle East, the financial markets could again be blindsided by a liquidity crisis which could easily spread into the economy as 401(K) plans start to feel the stress of falling equity prices, confidence crashes, and people’s financial decisions such as purchasing homes are put on hold.

Keep an Eye on Economic Data & Currency Markets

There is a rising tide of anecdotal data that suggests the economy is slowing such as falling truck sales, rapid declines in ocean freight, and wobbly PMI numbers. We’ve also seen somewhat disappointing housing data, while consumer confidence failed to meet expectations last week. Nevertheless, the markets pretty much followed a familiar script when the news hit the wires.

Among the winning sectors on Friday Jan. 3 were: Oil Service (OSX), Utilities (UTY), Homebuilders (SPHB) and Real Estate Investment Trusts (DJR). Meanwhile the Airlines (XAL), Banking (BKX), Biotech (BTK) took on some heavy selling.

On a sector basis it’s not surprising for oil service stocks to rally as the possibility that Iran may attack oil infrastructure comes to mind. The same can be said for interest sensitive sectors such as homebuilders, utilities, and REITs to have rallied as bond yields plummeted. On the losing side, banks have done poorly lately when bond yields fall, and biotech was ripe for a pullback after its big yearend rally.

What was most interesting was the action in individual stocks. For example, the Pharmaceutical sector as represented by the NYSE Arca Pharmaceutical Index(DRG) came out a loser for the day, but individual stocks such as Eli Lilly (LLY), Pfizer (PFE) and Merck (MRK) held up fairly well (see chart), which suggests that we are in the early stages of a Golden Age of Science. We noted this last week, and it passed its first test as investors, algos included, may be patient for a bit longer on these stocks.

So the question for investors now is whether the likely increase in uncertainty in the Middle East will start being reflected in stocks of companies who are in strong product cycles such as large pharmaceutical firms with current blockbusters, such as Merck’s cancer killer Keytruda, and Lilly and Pfizer’s potential pain management blockbuster Tanezumab, a late in development monoclonal antibody which blocks nerve growth factor, a chemical which is critical in the chronic pain generation pathway will be able to survive what could be a very volatile market over the next few weeks.

Finally, big market crises – remember the Thai Baht and the Ruble disasters in the late 1990s- develop when currency markets join stocks and bonds in the fray. Certainly the U.S. Dollar Index (USD) had a nice day as traders found refuge in the dollar. Thus, at this point, there is no indication that currency markets are malfunctioning (see chart). Nevertheless, with the presence of algos in all markets, trends can when bad things happen, the odds of contagion rise.

Bonds Take the Lead – NYAD Holds Up

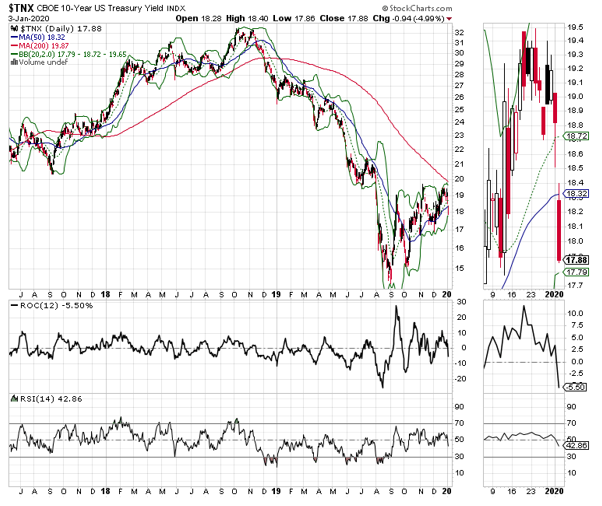

The big market news wasn’t so much the decline in the S&P 500 (SPX) and the Nasdaq 100 (NDX) indexes in response to the U.S.-Iran situation, but how the U.S. Ten Year Note Yield (TNX) collapsed; closing the week below 1.8% after flirting with the 2% yield area for most of December (see chart).

It’s a tough call whether TNX fell due to a flight to safety, in response to a very weak PMI number released on the same day the Iran situation expanded, or both; but further weakness in bond yields will likely have an effect on key stock market sectors and other markets such as currencies and commodities.

Luckily, the NYSE Advance Decline line (NYAD) pulled back on Jan. 3, but did not break down, which is a positive for now, especially after NYAD made a new intraweek high.

Moreover, both SPX and NDX still have a lot to room to fall before reaching the key support levels of their 50-day moving averages (see chart).

Will They Buy This Dip Too?

Investors have been conditioned to buy every single dip in the stock market over the last 10 years, and recent history shows that, sadly, wars can be profitable for investors. Thus, it would not be surprising to see money start moving into stocks over the next few days if the situation really heats up.

But since the market’s job is to make most of us look stupid, it is plausible to consider that this dip, much as the mini-bear market of late 2018 proved, may not be one to buy, at least not yet. Moreover, at this point, there is no hurry to jump into this market as geopolitical tempers heat up and things could get worse.

Therefore, as I noted last week, it still makes sense to stick with what’s working, take some profits, to consider hedging or tightening stops, and to explore undervalued stocks whose turn around plans are starting to bear fruit as long as they hold up.

Moreover, it is always plausible but difficult to predict whether the current situation may force active traders into a 100 percent cash position soon.

Joe Duarte is author of Trading Options for Dummies, and The Everything Guide to Investing in your 20s & 30s at Amazon. To receive Joe’s exclusive stock, option, and ETF recommendations, in your mailbox every week visit here.

Join Joe at the MoneyShow Orlando Feb. 6-8 where he will be discussing the ins and outs of the Markets-Economy-Life ecosystem (MEL) and how he uses it to pick winning stocks.