What is behind the Q4 rally and why you need to know, asks Daniel P. Collins.

Oct. 11, 2019 is an important date top remember. You may be forgiven for not knowing exactly why, as many people don’t.

If that date doesn’t ring a bell for you, you’re not alone, the news that came out that day was meant to be routine and uneventful. Perhaps you can remember the news from Sept. 17, better, that was when the Federal Reserve’s Fed Funds rate inexplicably spiked higher causing the Fed to resume regular repos.

However, it was on Oct. 11 when the Federal Reserve announced that it would be conducting a series of “purely technical” repurchase agreements “to ensure that reserves remain ample” in the financial system (see text below).

Matt Weller, global head of market research for FOREX.com, has done some interesting analysis on how the market has reacted since that time. He noted that “these twice- or thrice-weekly $35 billion + injections of liquidity have continued since in a process that traders have sarcastically dubbed: Not Quantitative Easing,” (see Repo Agreement Operational Details below).

Weller note that the Fed’s balance sheet has grown by nearly $400 billion, which is roughly half the size it unwound since allowing its purchases that were part of Quantitative Easing 3 to roll off its balance sheet beginning in January 2018 (see chart).

If you recall QE1, QE2, Operation Twist and finally QE3 where extraordinary interventions into the fixed income markets meant to keep a weakened system afloat following the 2008 Credit Crisis. QE3 involved the Fed purchasing $80 billion worth of fixed income products to keeps rates lower. The Fed had already cut the Fed Funds rate to zero and needed an additional tool to keep long-term rates down.

The thinking was that this would help stabilize the markets, and the Fed could unwind from this extraordinary policy, which bloated its balance sheet, at a time when our economy was in better shape to handle it.

No one at the time anticipated that the zero-interest-rate policy (ZIRP) would last so long and that QE3 would continue uninterrupted. But when the Fed announced it would slowly taper the purchases which were part of QE3 back in 2013, the market reacted violently in what was dubbed “The Taper Tantrum.”

Weller notes, “While repo operations like these are a standard tool that central banks use to manage liquidity in financial systems globally, there’s no denying that we’ve seen an astoundingly consistent rally in the S&P 500 since the Fed’s announcement. As the chart below shows, the S&P 500 has closed below even its short-term 10-day moving average just five times in the 70-plus trading days since the Fed’s repo operations began (see chart)."

Weller noted that, according to Quantitative Edges, this is the fewest times that the S&P 500 has closed below its 10-day moving average over a 70-day period since 1972. That is more than 50 years. “U.S. stocks haven’t seen this consistent of a rally since most of us have been alive,” noted Weller.

While it is true that correlation does not necessarily indicate causation, this is clearly something to pay attention to.

If you recall, the current bull market was not accompanied by robust growth, particularly in the beginning. It was widely believed to be a product of low interest rate, a zero-bound Fed Funds rate (ZIRP) that persisted for nearly eight years, plus the headwinds of QE2.

It appears that the Fed may still be holding up the market, which means that traders should keep a close eye on Fed policy going forward.

Fed’s Oct. 11 Statement

Consistent with its January 2019 Statement Regarding Monetary Policy Implementation and Balance Sheet Normalization, the Committee reaffirms its intention to implement monetary policy in a regime in which an ample supply of reserves ensures that control over the level of the federal funds rate and other short-term interest rates is exercised primarily through the setting of the Federal Reserve's administered rates, and in which active management of the supply of reserves is not required. To ensure that the supply of reserves remains ample, the Committee approved by notation vote completed on October 11, 2019 the following steps:

- In light of recent and expected increases in the Federal Reserve's non-reserve liabilities, the Federal Reserve will purchase Treasury bills at least into the second quarter of next year in order to maintain over time ample reserve balances at or above the level that prevailed in early September 2019.

- In addition, the Federal Reserve will conduct term and overnight repurchase agreement operations at least through January of next year to ensure that the supply of reserves remains ample even during periods of sharp increases in non-reserve liabilities, and to mitigate the risk of money market pressures that could adversely affect policy implementation.

These actions are purely technical measures to support the effective implementation of the FOMC's monetary policy, and do not represent a change in the stance of monetary policy. The Committee will continue to monitor money market developments as it assesses the level of reserves most consistent with efficient and effective policy implementation. The Committee stands ready to adjust the details of these plans as necessary to foster efficient and effective implementation of monetary policy.

In connection with these plans, the Federal Open Market Committee voted unanimously to authorize and direct the Federal Reserve Bank of New York, until instructed otherwise, to execute transactions in the System Open Market Account in accordance with the following domestic policy directive:

"Effective October 15, 2019, the Federal Open Market Committee directs the Desk to undertake open market operations as necessary to maintain the federal funds rate in a target range of 1-3/4 to 2 percent. In light of recent and expected increases in the Federal Reserve's non-reserve liabilities, the Committee directs the Desk to purchase Treasury bills at least into the second quarter of next year to maintain over time ample reserve balances at or above the level that prevailed in early September 2019. The Committee also directs the Desk to conduct term and overnight repurchase agreement operations at least through January of next year to ensure that the supply of reserves remains ample even during periods of sharp increases in non-reserve liabilities, and to mitigate the risk of money market pressures that could adversely affect policy implementation. In addition, the Committee directs the Desk to conduct overnight reverse repurchase operations (and reverse repurchase operations with maturities of more than one day when necessary to accommodate weekend, holiday, or similar trading conventions) at an offering rate of 1.70 percent, in amounts limited only by the value of Treasury securities held outright in the System Open Market Account that are available for such operations and by a per-counterparty limit of $30 billion per day.

The Committee directs the Desk to continue rolling over at auction all principal payments from the Federal Reserve's holdings of Treasury securities and to continue reinvesting all principal payments from the Federal Reserve's holdings of agency debt and agency mortgage-backed securities received during each calendar month. Principal payments from agency debt and agency mortgage-backed securities up to $20 billion per month will continue to be reinvested in Treasury securities to roughly match the maturity composition of Treasury securities outstanding; principal payments in excess of $20 billion per month will continue to be reinvested in agency mortgage-backed securities. Small deviations from these amounts for operational reasons are acceptable.

The Committee also directs the Desk to engage in dollar roll and coupon swap transactions as necessary to facilitate settlement of the Federal Reserve's agency mortgage-backed securities transactions."

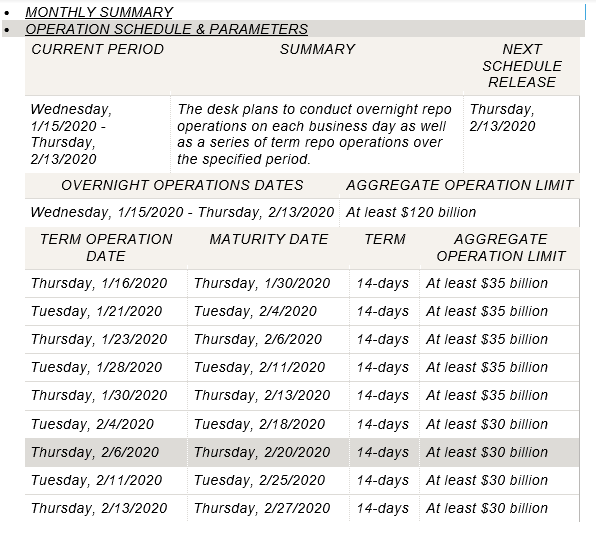

Repurchase Agreement Operational Details

In accordance with the most recent Federal Open Market Committee (FOMC) directive, the Open Market Trading Desk (the Desk) at the Federal Reserve Bank of New York will conduct a series of overnight and term repurchase agreement operations (repos) to ensure that the supply of reserves remains ample even during periods of sharp increases in non-reserve liabilities, and to mitigate the risk of money market pressures that could adversely affect policy implementation.

Securities eligible as collateral for both overnight and term operations include Treasury, agency debt, and agency mortgage-backed securities. Primary Dealers will be permitted to submit up to two propositions per security type. The minimum bid rate for term repo operations is based on prevailing market rates that reflect market expectations for the path of the federal funds rate over a similar tenor to that of the repo operation. This is a technical parameter and no inference should be drawn about the Federal Reserve’s views on the current or future stance of monetary policy based on the minimum bid rate.

The operation schedule and parameters are subject to change. The Desk will update the operation schedule and parameters table below daily to reflect the operational details for the following business day’s operations.

Schedule of Overnight and Term Repurchase Agreement Operations