The main goal of covered-call writing is to generate option premium cash flow. Many investors also seek to develop dividend income in addition to the option premium revenue, explains Alan Ellman of The Blue Collar Investor.

One security that presents a unique scenario is iShares 20+ Year Treasury Bond ETF (TLT). This exchange-traded fund produces dividend income 12 times a year with ex-dividend dates on the 1st of every month. Ex-dividend dates are the main reason for early exercise of our options so how are we going to capture both premium and dividend income with ex-dates coming up in the middle of all monthly contracts?

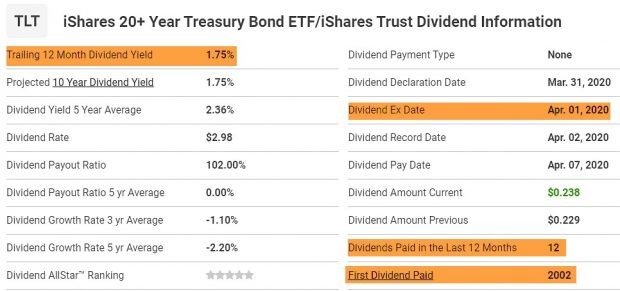

TLT Dividend Information: dividendinvestor.com

TLT: Dividend Information

The screenshot shows:

- 12 dividends per year

- Ex-date on the 1st of the month

- Annualized trailing 12-month yield is 1.75%

- Dividend income since 2002

TLT One-Week Option Chain

TLT: 1-Week Option-Chain on 4/17/2020

Trade Structuring Using the Ellman Calculator

TLT Calculations Using The Ellman Calculator

The spreadsheet shows:

- 1% one-week initial time-value returns (52% annualized)

- 0.6% downside protection of the time-value profit for the $169.00 strike

- 0.5% upside potential for the $171.00 strike

Our best calculator for covered-call writing and selling cash-secured puts is the new Elite-Plus Calculator.

Crafting the Strategy to Avoid Ex-Dividend Dates

We never have a covered-call option in place the week of the ex-date. This means that of the 52 weeks in a calendar year, we use only 40 of those weeks to write options or 77% of the time. This will reduce our potential annualized premium yield from 52% to 40%. Of course, many factors will determine final outcomes, but we are at an excellent starting point. In addition to premium income, we add in the 1.75% dividend income we receive divided on a monthly basis. The pay dates come after the ex-dates.

Discussion

When seeking to generate both premium and dividend income, we must factor in ex-dividend dates. Securities with weekly options like TLT allow us to write calls each week and simply avoid the weeks of the ex-dates. This strategy approach applies to securities that provide quarterly dividends where we can use monthly options eight months of the year and turn to weeklys in the contract months of the ex-dates for those securities that also have weekly options.

Learn more about Alan Ellman on the Blue Collar Investor Website.