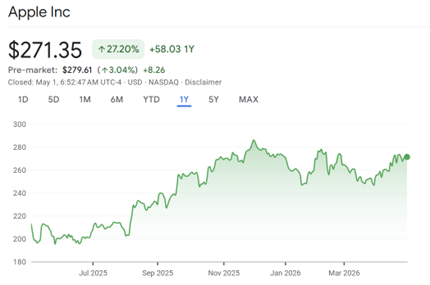

Apple Inc. (AAPL) rose last week after a quarter so good it could go in the Louvre. Apple's iPhone 17 is now the most popular in the company's history, helping to drive total revenue up 17% — much better than expected, notes Amber Kanwar, host of the In the Money with Amber Kanwar podcast.

Services revenue rose 16%, better than expected. China? That headwind a few years ago? Now up 28% from last year. Margins? Higher than they forecast even with input costs going up.

Remember this is a company that was struggling to grow sales a few years ago. Now, Apple says total sales will increase 14%-17% next quarter, which is better than the Street's 9% forecast.

Margins may be dented by rising memory prices. But other than that, there were few blemishes. It's a perfect handoff from Tim Cook to the incoming CEO John Ternus.

Now all attention turns to Apple's Worldwide Developer Conference in June. The expectation is that a better suite of AI products will be unveiled (Siri will finally get a brain!) And they will do it by spending just a fraction on AI compared to peers.

Hyperscale capex spending for 2026:

- Meta capex: $125B–$145B (midpoint ~$135B)

- Amazon capex: $200B

- Alphabet capex: $180B-$190B

- Microsoft capex: $190B

- Apple: $12.8B (estimate)