The market knows that renegotiating trade deals and the TPP presumes that there will be some adjustment for a situation related almost solely to currency exchange rates (including Canada) and not just a policy to flood our markets, says Gene Inger of The Inger Letter.

Perceptions of protectionism as a prosperity killer are valid only with a myopic viewpoint globally. To wit: India (the most egregious for years), China, and many others put tariffs on American goods for decades (except often for food because they needed it and had no capacity to compete with us or provide for themselves without our agricultural products).

At the same time, the United States was asked or presumed naive to just let in or allow untaxed or even subsidized goods or even services taking advantage of our lows and consumer demand, with no restrictions.

This, of course, was noble on the part of America in the post-war era but not for decades beyond. I was impressed that even Wilbur Ross pointed this out in his Friday media interviews because it is exactly what I’d decried for years with respect to the inertia of America’s trade policies.

Now, just to be clear as we need not review what’s already well-known (my own call for a renaissance of American manufacturing and capital repatriation even before the election in 2016). There are too broad or too vague discussions about what may be forthcoming from the president this week, and some of it makes a difference.

The global trade war issue is an issue on top of a difficult market prior to this. Curiously, rumors of the White House considering reentering the Trans-Pacific Partnership surfaced this week too; but was ignored as the focus moved to a global series of tariff applications. Of course, it would go further than impacting the nominal price of a soda can or car or truck, and yes there could be varying dislocations.

And that’s the difference. We simply cannot do this successfully with our Canadian neighbors in particular. That’s because they are presently paying a premium to buy American semiconductors and certain other products, because of the strong US dollar (USD/CAD) vs. a weaker Loony (Canadian dollar). That approximate 30% swing can be viewed in the same extreme that we’re viewing prices of steel or aluminum from their mills (lumber too).

My point is that Canada is not a low-cost producer like Asian countries, nor is it subsidizing products particularly. Mostly wages and prices are a close match for the United States now, and that means it’s currency, not tariff issues.

I think the stock market knows this and presumes that by the time the policy is really defined there will be some adjustment for a situation related almost solely to currency exchange rates, and not just a policy to flood our markets.

The service end of this can relate for instance to foreign airlines. In particular two stand out as unfair competition: Emirates Air and on a smaller basis, Etihad. American and European carriers are fighting their government (sort of family) subsidies which allow them to offer superb service, but at operating costs normal carriers can't compete with. Now it isn’t likely you'll put a tariff on them, but fewer landing slots is a way.

I suspect if Canada and maybe Mexico to a degree is exempted with a provision that deflects concern of back-door chain trans-shipments (such as originate in Asia and hopscotch thrrough Canada or Mexico), the edge comes off this particular concern.

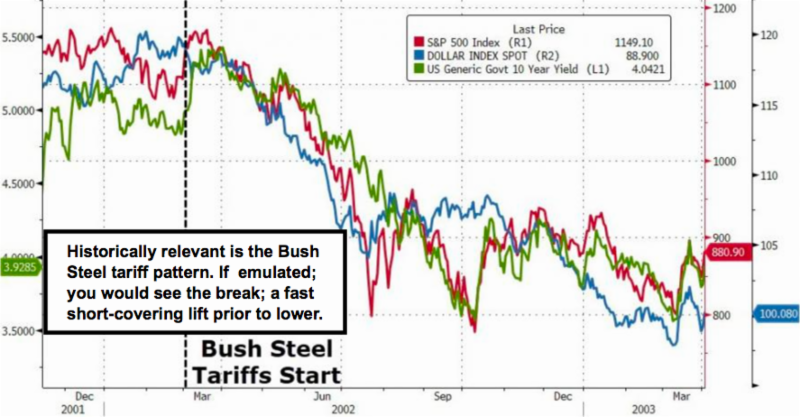

In-sum: what ultimately happens from the more-than-hubris-based shift on trade is some sort of compromise. It really is America’s overdue retaliation to trade wars aimed at the U.S., and actually at Europe too, for many years. Again Art of The Deal is not really a repeat of action that was attempted under George W. Bush.

Ideally, I’d like to see an update to NAFTA and the U.S. rejoining the TPP with better terms. And the tariffs threat, or even actual implementations, can lead to that. There’s a prospect that the U.S. already tried and failed in the past year’s efforts to renegotiate NAFTA. Now, this pressure is likely to bring negotiators closer to making a proper deal. That part isn’t in any of the public discussions, but the simplicity of foreign exchange should be, given that there is a vast difference between dumping steel, for instance, trans-shipment, or for that matter currency exchange rate impacts, which do not relate to subsidies or nefarious export shipping.

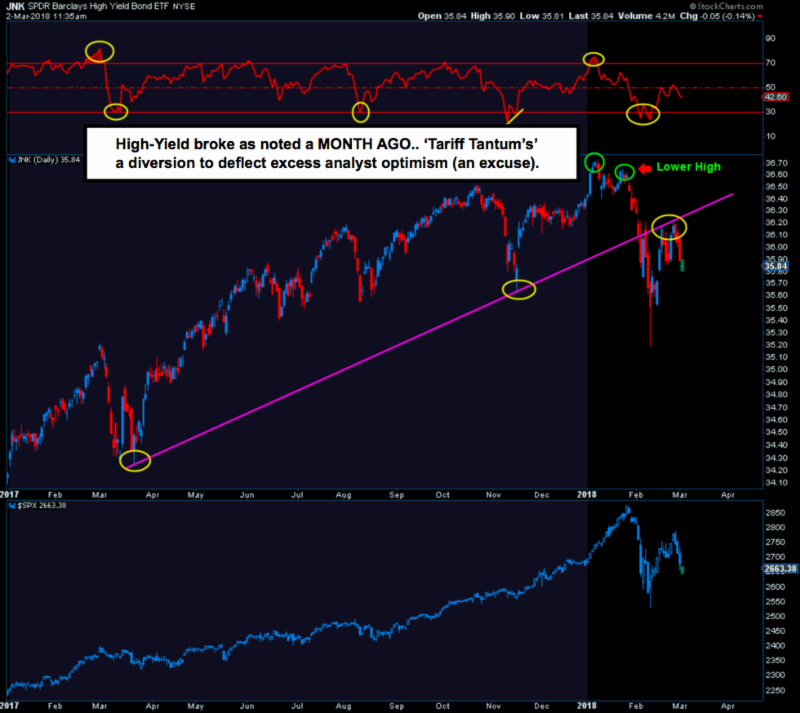

Bottom line: The tariff issue is all the rage now, but the market break began weeks ago. It had an automatic rally that burst above the resistance levels and exhausted that short-covering and reversed up to down earlier last week, in line with projections.

Sure, the trade war fears surfaced and accelerated already defensive markets, both from a technical and monetary basis. Everyone seemed to overlook NY Fed's Dudley suggesting four rate hikes would be fair and logical this year.