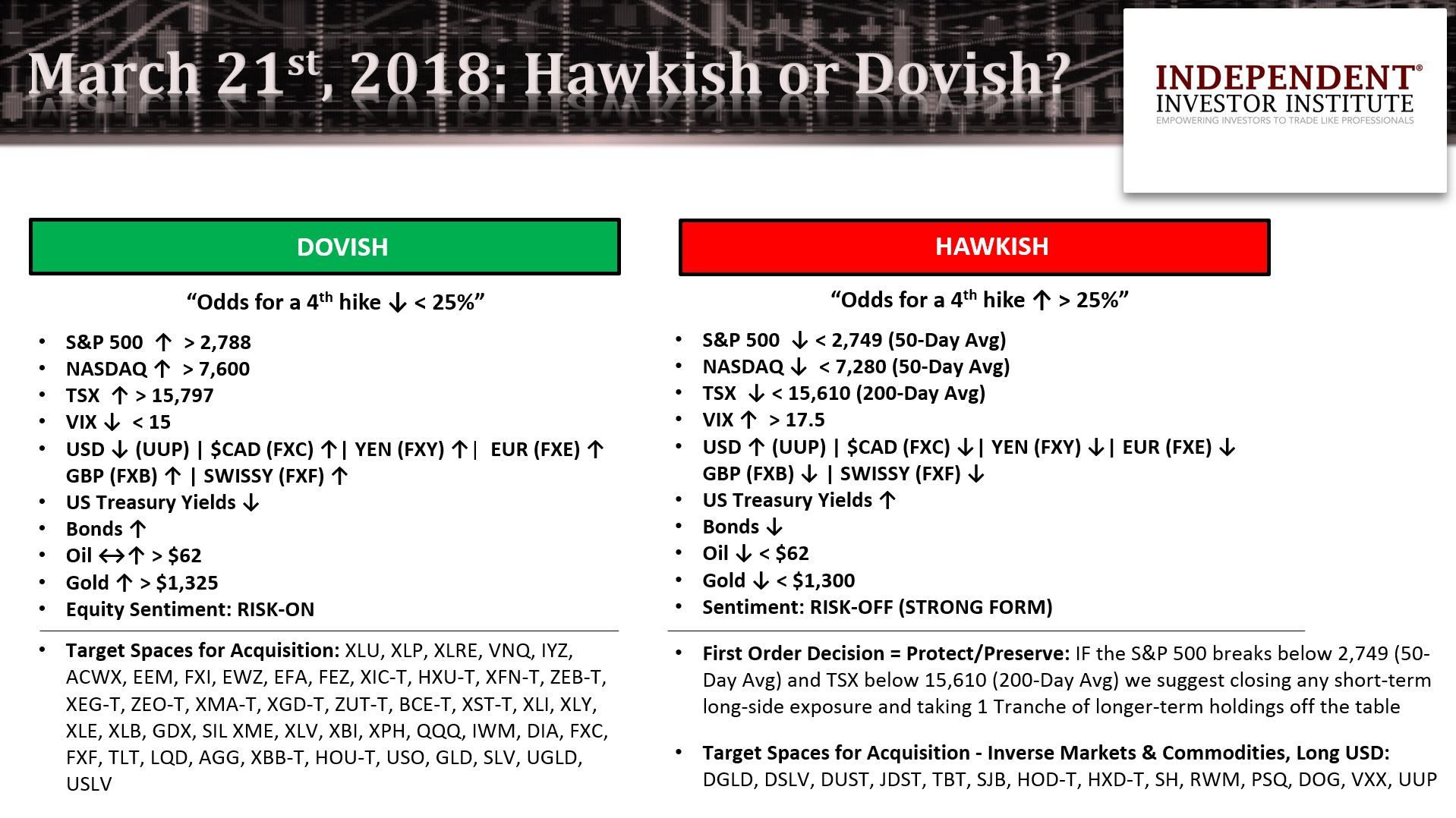

Wednesday, March 21 is the pivot for the week as either Powell is perceived as hawkish and odds for a 4th rate hike in 2018 to grow beyond the 25% they sit at or Mr. Market sees enough. Dovishness to keep-the-faith even for a week or two, writes Ziad Jasani Monday.

View his video commentary here

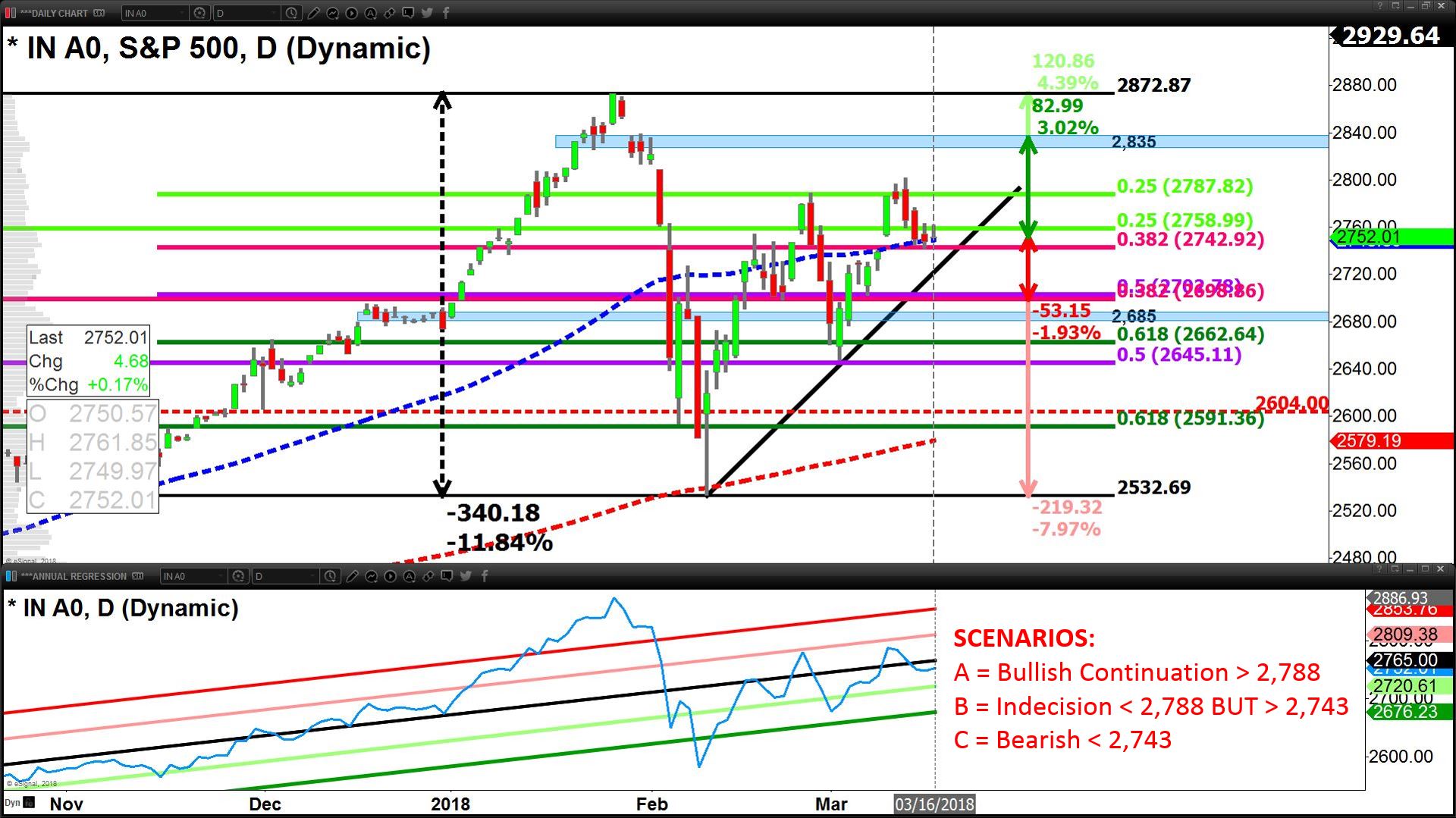

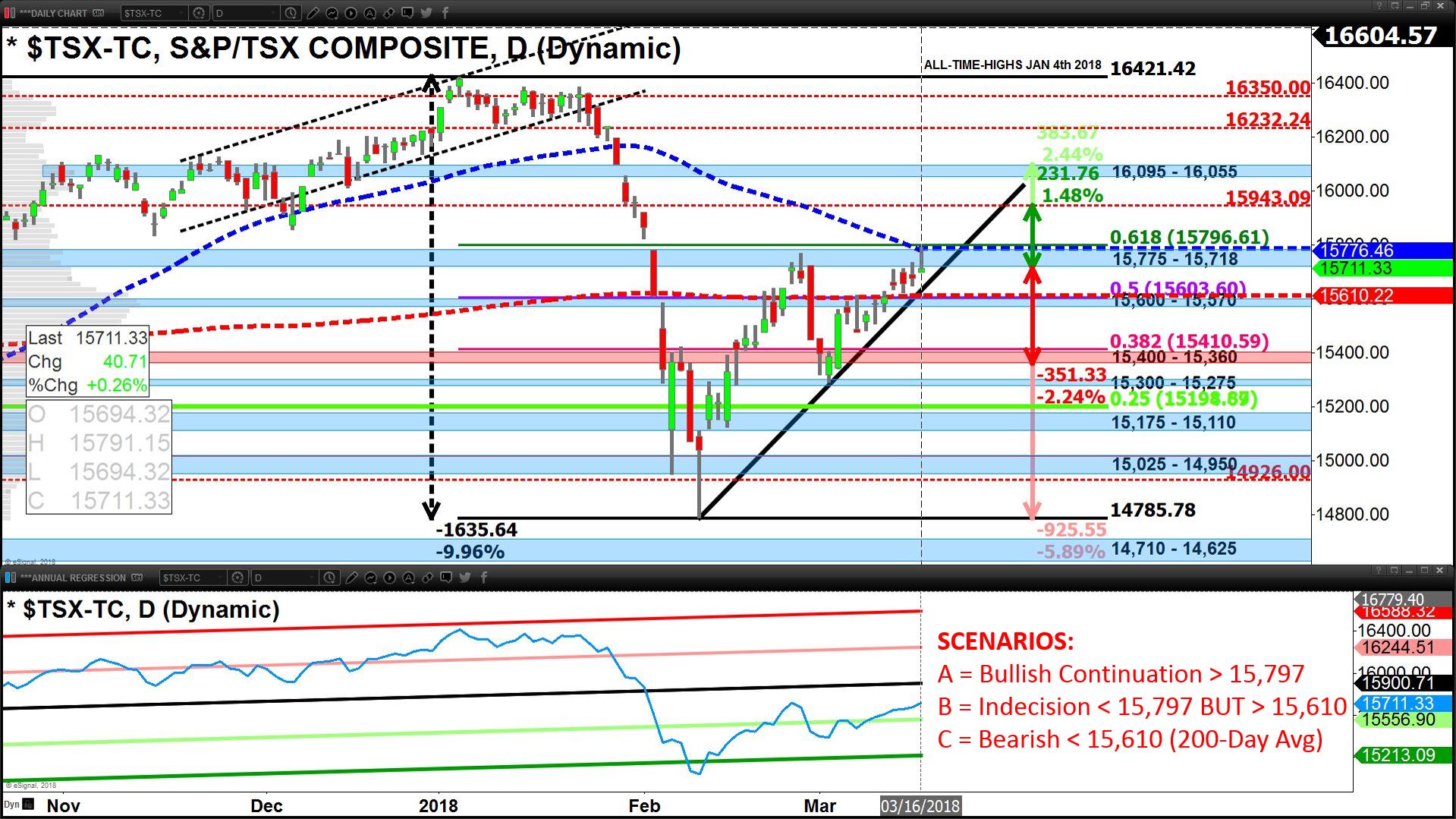

We ended last week with U.S. markets holding above support at its 50-day average S&P 500 (SPX) 2,749, and S&P 500/Toronto (TSX) in a range below its 50-day average (15,776) but above its 200-day average (15,610).

Inflationary pressures did not break the market last week.

However, White House woes, UK/Russia, trade wars (U.S.-China), bitcoin-battery on ad-pull-backs and GDP forecasters lowering calls (Atlanta Fed Q1 2018 = +1.8%) prevented markets from carrying the Feb. 9 bounce forward.

Should we stay, or should we go? This week is likely to pivot on Wednesday, March 2 at 2 pm (EDT) when we hear from the Fed and new Chair Powell.

We ended last week with the Hold decision in U.S. markets for those playing out the Feb. 9/March 2 macro-market swing-low and accumulated some short-term TSX-Risk (XFN-T, ZEB-T, XEG-T, ZEO-T) Friday morning (March 16).

Macro-Variable analysis on March 16 implied the following behaviors over Monday/Tuesday (March 19 & 20):

• U.S. dollar (USD) ↓ (Euro, Yen & CAD ↑)

• U.S. Treasury yields ↔↓ & Bonds ↔↑

• Commodities ↑ (Oil, Nat gas, Copper, Precious Metals)

• Equities ↑ (Commodity-laden markets & Defensive Sectors outperform)

• Our Trading Community voted on Scenario B for the week (see chart above).

Wednesday, March 21 is the pivot for the week as either Powell is perceived as hawkish and odds for a 4th rate hike in 2018 to grow beyond the 25% they sit at or Mr. Market sees enough.

Dovishness to keep-the-faith even for a week or two and allow for a retest of late Jan. 2018 highs.

The charts are set up to expect Dovishness. Why? Bonds have broken down-trends, the yield curve compressed over the last week, and tields are highly overbought while bonds are oversold: 10-year U.S. Treasury yield, Global Bond Market, AGG, XBB-T.

However, logic would dictate that the Fed leans hawkish, as inflationary pressures are mounting and there are less doves on the voting roster this go around.

View the Independent Investor Institute trading ideas and strategies videos here.