There’s a market that just “blew up.” But I’m not talking about stocks. I’m talking about government bonds. Last Friday and this Monday, the yield on the 10-year Treasury note shot up to 2.97% from 2.85%, writes Mike Larson Wednesday.

Since bond prices move in the opposite direction of yields, the price of U.S. Treasury bond futures tanked more than two-and-a-half points.

Things were even worse in Japan, though. Government bond yields shot up the most in almost two years over there.

Just because stocks weren’t the asset taken to the woodshed this time around doesn’t mean they’ve been immune from increasing turmoil. Six months ago, stocks got rocked with the Dow Industrials (DJI) plunging more than 1,000 points in a single day ... twice. It ultimately shed more than 3,200 points from high to low.

Then there’s the volatility market. It went ballistic in February. Following a record-breaking streak of all-time lows and extreme stability, the CBOE Volatility Index soared from around 10 to more than 50 in just a few days.

That was the highest intraday reading since China’s surprise yuan devaluation in August 2015. It absolutely destroyed shareholders in so-called inverse volatility exchange-traded products, with a handful of them losing more than 90% of their value in less than 24 hours!

Three different markets. Three different tantrums. But they all stem from the same underlying, driving force – and that force is only getting more powerful with time!

It goes back to what I wrote in May: Central banks the world over are slowly but surely turning off the flood of excess liquidity into markets. First, they’re raising interest rates. Second, they’re dialing back Quantitative Easing, or QE, programs in which they bought trillions of dollars in bonds and stocks. The process even has a nickname: “Quantitative Tightening,” or QT.

It was concern about the latter that knocked the bond market for a loop. Media “trial balloons” out of Japan suggested that country’s central bank was trying to figure out a way to dial back its stimulus. Bank of Japan policymakers hold their next meeting on July 30-31, and several options are reportedly on the table.

Why is that such a big deal? Enough to set off the worst yield surge since 2016?

Bank of Japan, Public Domain

Because the BOJ has Hoovered up so many Japanese government bonds that it owns almost half the entire market!

This has crowded out many of the private pension funds, money managers and others who would normally be in there, actively buying and selling.

In fact, there were six times this year when not one single Japanese 10-year bond changed hands in the regular trading session. That’s like if the NYSE opened, and everyone just decided to play Fortnite on their phones all day rather than enter BUY and SELL orders!

Japan hasn’t just destroyed liquidity and private market price discovery in bonds though. It has also been actively buying more than $54 billion a year in stock ETFs. Result: The BOJ is now one of the top 10 shareholders in around 40% of the publicly traded companies in Japan, with a total portfolio of more than $227 billion.

In sum, regardless of exactly what kind of QT the BOJ does or when it does it, it’s going to roil the markets. And the BOJ isn’t alone. The U.S. Federal Reserve is well along the QT path, having already shrunk its balance sheet by more than $220 billion from peak levels. The European Central Bank also recently said it would slash its QE program in half in October, then eliminate it altogether in December.

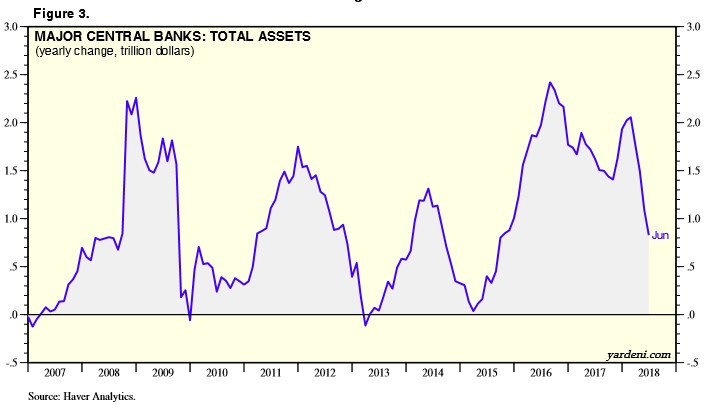

You can already see in this chart from Yardeni Research that we’re seeing growth in total central bank assets slow dramatically. That line will continue to plunge toward the zero mark as 2018 wears on thanks to those revised plans.

No one can say for certain how much of the explosive rally in assets of all kinds since 2009 was “real” vs. central-bank-driven “fluff.” I certainly have my opinions, which I’ve shared with readers like you. And I continue to give my Safe Money subscribers investments that are set to thrive in exactly these kinds of conditions. Learn more about my approach here.

But it’s 100% clear to me that, as QT intensifies, we’ll see more tumult, more volatility and more market chaos. Just like the kind we’ve already seen three times in three different markets in just the first seven months of 2018.

This is exactly why I continue to recommend holding a higher percentage of cash in your portfolio and hedging against downside risk with tools like inverse ETFs. It’s also why you should stick with only the highest-quality, fundamentally strongest stocks as identified by our time-tested Weiss Ratings system.

Until next time,

Mike Larson

Join me at the MoneyShow San Francisco August 23-25. You can see my speaking schedule, and get registered for free, by clicking here!

Check out Mike’s short video interview, Conservative Stock Picks for 2018 at MoneyShow Las Vegas here.

Duration: 3:33

Recorded: May 14, 2018

Check out Mike’s short video interview What Investors Are Doing Wrong and How to Fix It at MoneyShow Las Vegas here:

Duration: 2:22

Recorded: May 14, 2018.