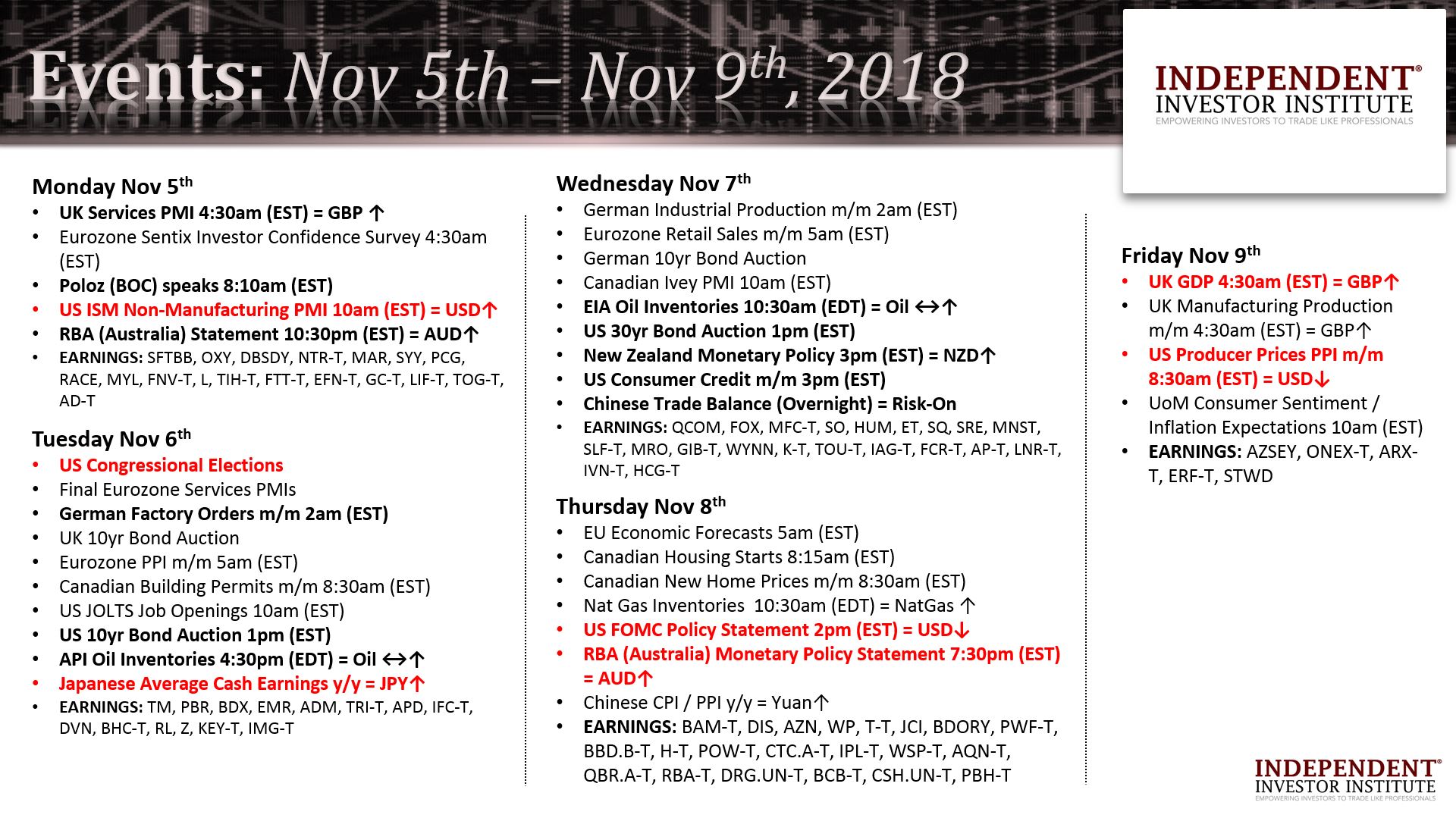

As we enter the most important week to shape risk-sentiment into year’s end we are well aware that financial markets have signaled a transition in the real economy, writes Ziad Jasani Monday from Toronto with a video.

View my weekly strategy session video here.

Recorded: Nov. 2, 2018.

Duration: 2:06:14.

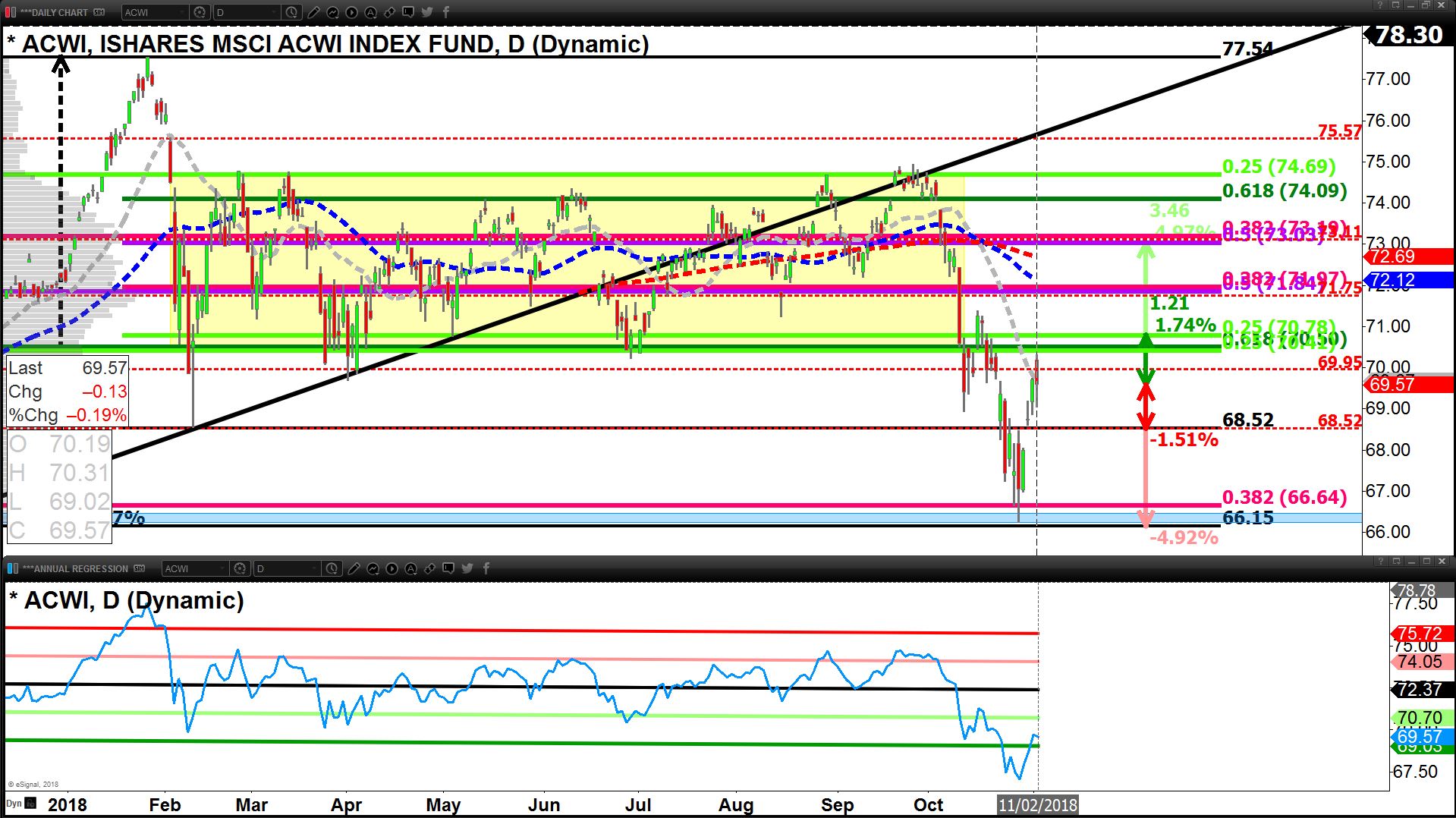

The Global Equity Market (ACWI) broke long-term up-trends mid-summer, driven by rising rates, trade wars, and growth slowing for markets outside of North America (most notably in China).

Through Octo-bear, the 8-month-long consolidation pattern global equity markets have been traversing since Feb. 2018 also gave way (yellow zone on ACWI chart).

Longer-term investors within our Independent Investor Institute Community have been de-risking since late September 2018 and since October 12 we’ve been hunting for a bounce.

Why? Earnings continue to float-the-boat, and institutions have not capitulated.

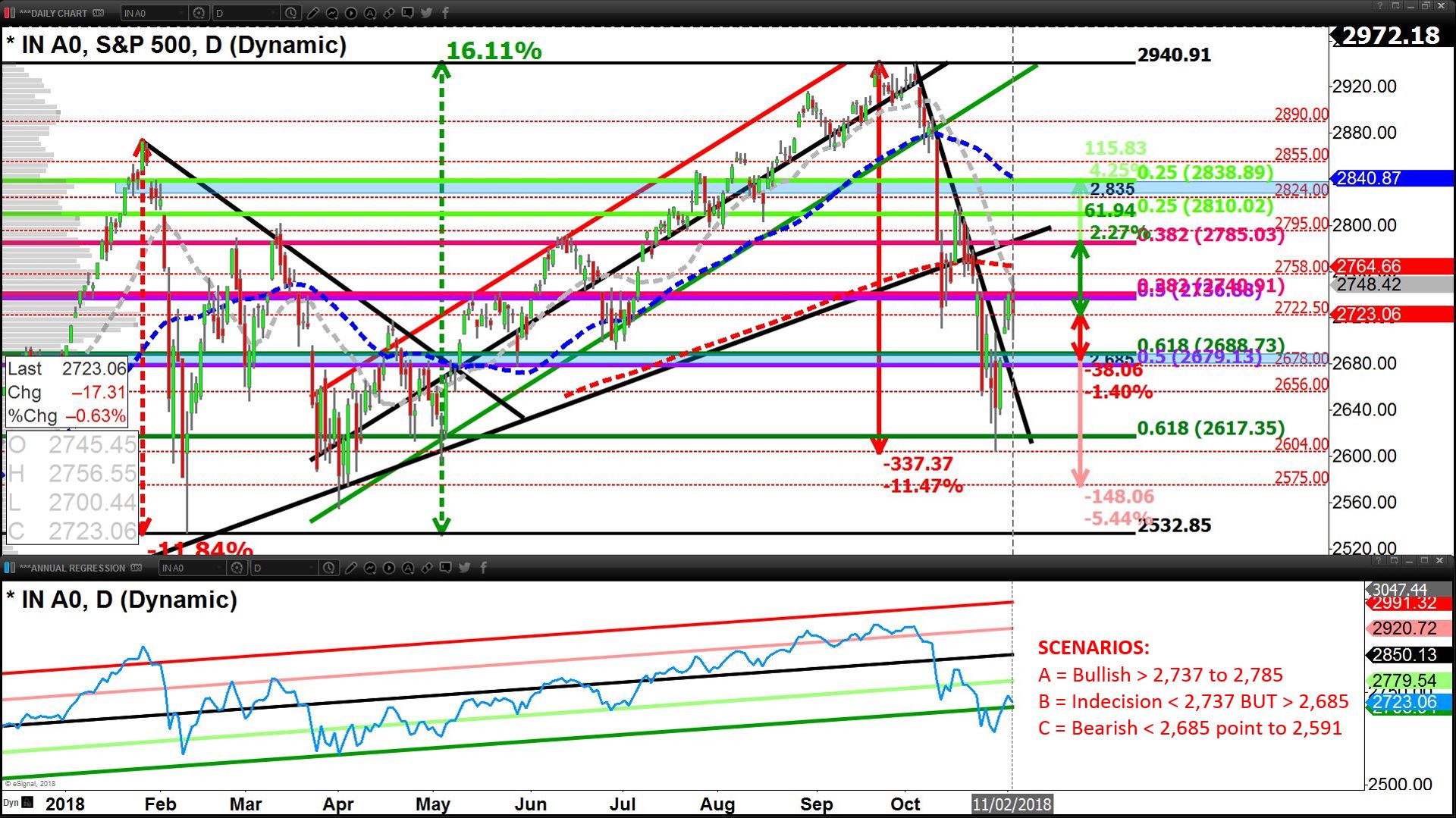

On Tuesday, October 30 we legged in, then received confirmation on October 31 of reaching escape-velocity as the S&P 500 Futures broke above 2,701.

We then received follow-through into the November 1 close with the S&P 500 (SPX) closing above its 50% retracement line for the years range (2,737); ahead of Apple (AAPL) earnings.

Our strategy focused on Index, Sector and Growth-Based Trades (SPY, QQQ, IWM, DIA, EWC, XIC-T, EEM, SPHB, MTUM, XBI, IBB, XLY, XLI, XLK, IYW, IVW).

Furthermore, we expressed clear intent to exit these trades (partially or wholly) in after-hours Thursday, Nov. 1, if AAPL disappointed markets. AAPL’s disappointing guidance on the heels of Amazon (AMZN) and Alphabet (GOOGL) shook many of us out of positions in afterhours.

Then, the volatility on Friday, Nov. 2 forced the majority of our positions to be stopped-out with profit.

Yet, we ended last week with the call for this bounce to likely continue and to be on-the-ready to re-engage in the aforementioned spaces.

This week hinges on midterms and monetary policy, while the earnings back-drop remains positive and markets speculate on whether Trump and Xi play-nice into the Buenos Aires G20 Summit (Nov. 30).

If the S&P 500 Futures Index is able to hold above 2,701 overnight Tuesday, Nov. 6, we are likely to be in short-term buy-mode overnight and into the open Nov. 7.

We are then expecting a less hawkish statement from Powell on Thursday, Nov. 8 serving to stabilize the fragile Bond Market, and uplift Equities and Commodities (globally).

Having reduced our long-term exposure once (Sept. 2018), we remain on alert to further reduce if our swing-barometer (S&P 500) should find itself below 2,685 (and the TSX < 14,926) through midterms.

The ingoing position of Currency Markets suggests the USD (UUP) is more likely to point into week’s end, but is more likely to see a rise into midweek first; supporting a pause in the Equity-bounce to start the week, and keeping us away from further accumulation of precious metals.

We look to Powell on Nov. 8 to give us a break-out on Gold, Silver and Miners before we act. We maintain our exposure to currencies on the other side of the USD to start the week (FXE, FXB, FXA, FXC, FXY) and look to build these positions post midterms and Powell if the EUR/USD is able to surmount 1.145 and Commodities (DBC) are in a bounce.

The Commodity Complex (DBC) is nearing a short-term oversold-bounce, yet Oil remains in a pervasive down-trend as Persian pumps continue (Iran) to flow and the global-growth-outlook softens.

A bottom and bounce for Oil in the $61.75-$60.35 area is expected; and likely timed with Inventories midweek. Natural Gas was held long over the weekend (UNG, HNU-T) above $3.27, we look to build the position above $3.52 or cut it under $3.39.

Base Metals (DBB), led by Copper (CPER), are more likely tied to the flight-path of equities, requiring patience and hold-decisions while Copper > $2.79- $2.77. The longer-term picture for Commodities (DBC), having broken long-term up-trend channels, reinforces our suggestion that financial markets are signaling a transition for the real economy.

The Global Bond Market (BND+BNDX), has once again returned to a perilous spot (short-term). On the heels of a strong U.S. Payrolls report the 10-year U.S. Treasury yield shot +2.2% higher on Nov. 2, adding instability to the fragile Equity Market bounce, which was damaged the day before by AAPL.

If Trump keeps the Senate but has his power tapered in the House, one of the outcomes includes a bid to Bonds, as the consensus for slower growth would build. This could actually serve to stabilize Bonds and support Equity bounce continuing.

Enjoy a complimentary no strings attached 30-day subscription to Ziad Jasani’s Daily Insights. Simply send Ziad an email with FREE TRIAL in the subject: ziad.jasani@educatedtrader.com