Headline GDP figure doesn’t give true picture and market seems to know it, writes Matt Weller.

Throughout this week, we’ve been highlighting today’s Q1 U.S .GDP report as a potential market-mover for everything from forex to the S&P 500 and beyond.

Late last week, we highlighted the potential for a stronger-than-anticipated GDP reading, and the initial headline certainly supported that view. Overall, the Bureau of Economic Analysis BEA estimated that the U.S. economy grew at a 3.2% annualized rate in Q1, well above expectations of 2.2% growth. While President Trump will no doubt extol the headline growth, the details are less impressive under the hood. For one, the strong GDP reading was boosted by inventory growth (+0.65% to the headline), with inventories rising to their highest levels since 2015. In addition, external trade added substantially to the bottom line. Given the mean-reverting nature of inventories and the ongoing trade war with China, both of these supportive factors may reverse to become headwinds in the coming quarters.

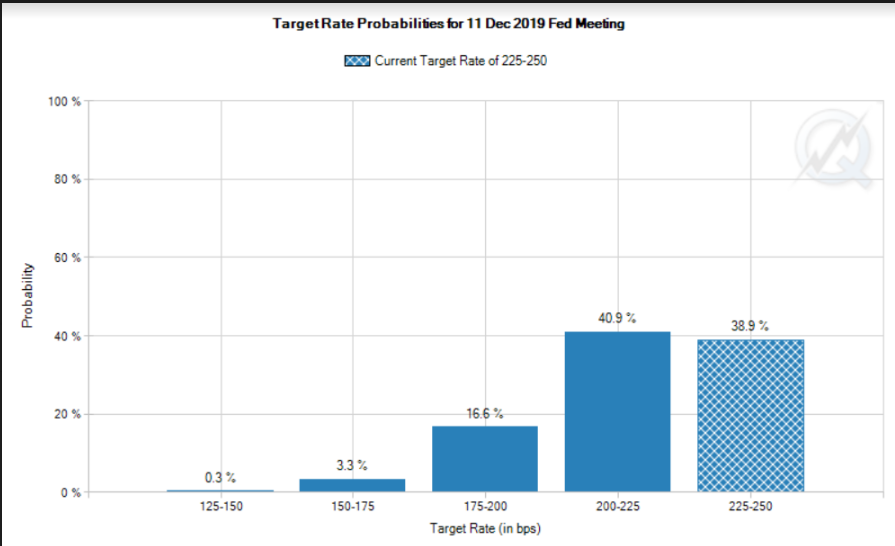

Perhaps most importantly for the Federal Reserve, the accompanying inflation data came in lighter than anticipated: the GDP price index rose just 0.9% vs. 1.2% eyed, while the GDP deflator rose just 0.6%, well below the 1.3% reading anticipated. In other words, this is not the type of “strong” growth that will scare the Fed into raising interest rates any time soon. Fed Funds futures traders agree, with the CME’s Fed watch tool showing the odds of a rate cut by year-end essentially unchanged from pre-release levels near 60%.

Source: CME FedWatch, FOREX.com

Market Reaction

The U.S. dollar initially spiked higher on the news, with the U.S. Dollar Index hitting a 23-month high by a single pip at 98.33 before pulling back. As we go to press, the indicator is trading back at 98.00, down slightly from pre-release levels. U.S. stock index futures spiked on the news, with the S&P 500 and DJIA now pointing to flat opens. The biggest relative move we’ve seen is in Treasury yields, with the two-year yield shedding a quick 3 basis points back to 2.29% and the benchmark 10-year tenor seeing a similar drop to 2.50%.