Technically, crude oil appears to have set bottom, but more interestingly is the question of how the U.S. will respond to Saudi & Russian provocations, asks Al Brooks.

Crude oil futures had an extreme sell climax last week. It might have to go sideways for a long time before there is much of a reversal.

The monthly chart of crude oil has been in a bear trend for 12 years (see below). This year’s selloff is the third leg down from the 2008 high. This month reversed up strongly after breaking below the bear channel.

Furthermore, the low was a measured move down from the height of the 2015 to 2020 trading range. Finally, the low was from single digits. Ten dollars is an important Big Round Number and therefore psychological support.

Last week is a reasonable candidate for the end of the current leg down. A bear trend ends when no one is left to sell at the low. The bears see that it is getting too easy to sell at the low. Good fill, bad trade. Too many buyers down there. They conclude that they need to sell higher and therefore stop selling near the low.

Additionally, at the bottom of a sell climax, the bears have huge profits. Since their stop is far above, they become eager to reduce their risk. They look for a sell climax at support and then take profits. That reduces their position size, which means their risk is less.

The bulls see the reversal up and they begin to buy. The result is a sharp short covering rally. For example, the May contract rallied $50 in its final 24 hours. Also, the June contract went up more than 100% in 24 hours this week.

What happens after a sell climax?

When the bears take profits, they want to be confident that the bear trend has not become a bull trend. At a minimum, they want to see at least two attempts at a trend reversal. After those two legs up, they will begin to sell again if they think the rally is failing.

That means that the minimum rally will have at least a couple legs up and last at least 10 days. That is about two weeks. It could be much more, but usually not much less.

About 20% of the time, when there is a reversal up from a sell climax, the V bottom reversal grows into a bull trend. What usually happens is that the rally has a couple legs up. Traders then look for a resumption of the bear trend. If that second selloff reverses again, there is a 40% chance of it growing into a bull trend. More often, there are additional legs up and down and the bear trend evolves into a trading range.

Every trading range always has both buy and sell signals. But crude oil is unlikely to fall much below $10. That means there will eventually be a bull trend.

However, the trading range could last many months and possibly years before a significant bull trend begins. If the range is tight, traders call that a “dead money” market. There is little profit potential and many traders will choose to trade other markets.

Traders should expect crude oil to be a trader’s market for a long time. They will buy low, sell high, and take quick profits, betting on a trading range and against a trend.

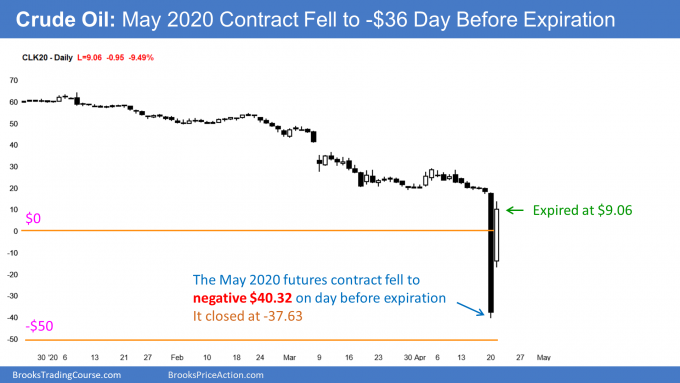

Crude oil daily chart: Fell below zero this week!

The daily chart of the May futures contract expired on Tuesday at $10.01. What is noteworthy is that it traded down to far below zero on Monday. It closed on Monday at -$37.63 a barrel. That means that at that moment, the oil producers were willing to pay $37.63 to anyone willing to take the oil off their hands. They had determined that it was better financially to pay someone to take the crude oil than it was for them to keep it.

There are many factors involved. An obvious one is that they clearly did not have the ability to store it because all of their storage tanks were full.

Another important factor is that taking crude oil from below the surface of the earth is not the same as getting water from a faucet. You cannot instantly turn it off and then on. If that were the case, they would have done it.

Why don’t the oil producers cut the supply of oil?

There are two primary reasons for the oversupply. One is you. How many miles have you driven over the past couple months? Compare that to last year at this time. Consumption is much less.

The other reason is less certain and it has to do with Saudi Arabia and Russia. The news says they are squabbling over reducing supply. It is being reported that they cannot come to an agreement about cuts that would be big enough to raise prices. Okay, fair enough.

Follow the money

There is uncertainy to it. That has to do with intent. It would benefit both countries if the U.S. crude oil production was severely curtailed. One way that could happen is if lots of U.S. oil producers ceased to exist. That could happen if oil prices stay this low for several months.

Why wouldn’t the Saudi and Russian oil companies go bankrupt as well? Because they are effectively owned by their governments and those governments will not let that happen.

Saudi Arabia and Russia could quickly make the price go up by greatly cutting supply. Why are they not doing that when the low prices are also hurting their economies? It must be that they see the low oil prices as benefiting them in the long run.

This is an old fashioned price war. Those wars are fought to drive a competitor out of business. Short-term pain for long-term gain. This is what Saudi Arabia through OPEC did five years at the Thanksgiving Day OPEC meeting—in the midst of falling crude oil prices, it decided not to cut production, but to increase it to drive the higher cost producers out. It kind of worked, thought the U.S. frackers who were targeted were more resilient than the Saudis counting in, Once the competitor is gone, you get his market share and you are free to greatly raise the price without the fear of competition.

Saudi Arabia denies that this is their motive. President Trump is on good terms with Russian President Putin, but if you follow the money, the path leads to this conclusion, despite the denials.

Where are Washington and the media?

What is surprising to me is that I haven’t heard anything bold coming out of Washington about fighting back. A price war is an actual form of war, and it therefore requires a strong defense. For example, the Federal Reserve says it is willing to print infinite dollars to save the economy. Why hasn’t the Secretary of Energy said that the Army Corps of Engineers will build infinite oil storage tanks to fight back?

I really don’t understand why I haven’t heard any bold statement from Washington to the effect that the Saudis and Russians have crossed a line and that our government would do whatever is necessary to defend our interests. In part, it is because the pandemic is consuming everyone’s attention. But what is happening to oil is very important, and our government is failing to address it.

There has been some talk about paying U.S. oil producers to stop producing, like grain incentives, but the idea does not appear to be gaining traction.

The press is ignoring the problem. I assume it is a combination of the pandemic and schadenfreude. Energy has done many things over the years that have angered environmentalists and the media. Maybe the media is quietly enjoying hearing the powerful voice of the fossil fuel industry become a lot quieter.

Trading Room

Traders can see the end of the day bar-by-bar price action report by signing up for free at BrooksPriceAction.com. I talk about the detailed E-mini price action real-time throughout the day in the BrooksPriceAction.com trading room. We offer a two-day free trial.