One of the most popular exchange-traded funds (ETFs) used as underlyings for covered call writing is Invesco QQQ Trust (QQQ) which consists of 100 of the largest domestic and international non-financial companies listed on the Nasdaq exchange, asks Alan Ellman of The Blue Collar Investor.

It is the ETF I have used the most over the past two decades of option-selling. This article will highlight a methodology of incorporating the Nasdaq-100 Volatility Index (VOLQ) into a low-risk strategy targeting a 10% – 15% annualized return.

What is VOLQ?

This is a 30-day measure of the implied volatility of the Nasdaq 100 Index (NDX) as expressed by at-the-money (ATM) NDX options. It is based on one standard deviation (68% accuracy). This information can provide investors with an expected trading range of NDX over the next 30-days.

What is covered call writing?

This is a low-risk option-selling strategy where a security is purchased in 100 share increments and then call options are sold leveraging those securities. Option sellers are undertaking the obligation to sell those shares at the strike price while option buyers hold the rights to exercise the options at any time during the contract (American-style options). In return for undertaking the obligation, covered call writers are paid a premium.

Proposed QQQ/VOLQ strategy

Determine the expected trading range of QQQ over the next 30-days based on VOLQ. Use the low end of the range to determine the target premium for selling an in-the-money (ITM) call option which will bring our breakeven to that low-end price point. Any time-value component of that premium will become realized profit if share price does not dip below that deep ITM strike price.

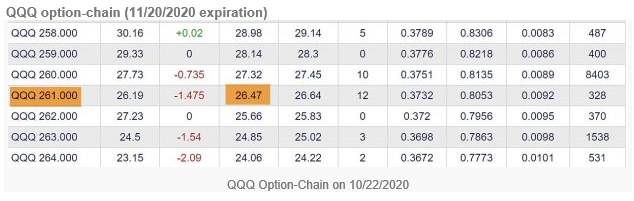

Real-life covered call trade example with QQQ on 10/22/2020 (the stats)

- QQQ is trading at $284.32

- VOLQ is listed at 32.16

- Expected 30-day % price change based on VOLQ is 9.29% (32.16/3.46), where 3.46 is the square root of 12 (# 30-day cycles in a year)

- 9.29% of $284.32 is $26.69, leaving an expected price range for QQQ between $257.63 and $311.01

- Our target premium for selling an ITM call option for QQQ is $26.69 which will bring us down to the low point of the expected range

- We must make sure there is a time-value component that will remain to meet our 10% – 15% annualized return goal range

- The intrinsic-value component of the premium will be used to “buy down” the cost basis from $284.32 to the strike price

- The $261.00 strike shows a bid price of $26.47, aligning with our target price of $26.69.

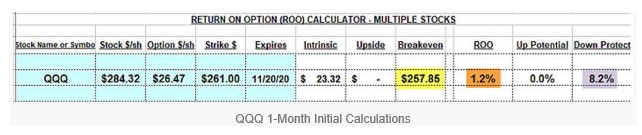

Initial covered call writing calculations using The Ellman Calculator

- The breakeven price point is $257.85, aligning with our target of $257.63

- The time-value return on the option (ROO) is 1.2%, 14.4% annualized falling within our 10% – 15% targeted annualized return goal range ($3.15/$261.00)

- Since an ITM strike was sold, there is no upside potential relating to share appreciation

- There is an 8.2% downside protection of the time-value profit (different from breakeven). This means that an investor is guaranteed a 1.2% one-month return as long as share value does not decline by more than 8.2% by contract expiration

Discussion

VOLQ can be an extremely useful tool when covered call writing with QQQ to establish a target strike price when seeking to generate significant annualized returns incorporating a low-risk, high probability approach. This strategy is especially attractive in low-interest-rate environments like we are currently experiencing.

Learn more about Alan Ellman on the Blue Collar Investor Website.