It’s no secret that for the past decade and a half, the Federal Reserve has made it its mission to create a “wealth effect” in the economy by boosting asset prices, states Jesse Felder of TheFelderReport.com.

Back in 2010, Ben Bernanke explained, “…higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion.” And so, he began a process of printing money with the explicit purpose of inflating asset prices, a policy that has been continued by each of his successors.

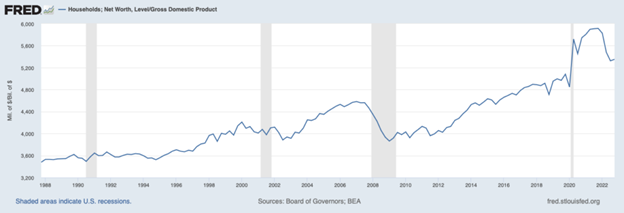

Over this time, quantitative easing, as the policy is called, has been inordinately successful in boosting asset prices while not so effective in boosting the economy. The most straightforward evidence of this is the fact that household net worth relative to the economy has soared to record highs during the QE era. If it had worked the way Bernanke intended then, after a brief surge in the ratio, it would have flattened out as growth in the economy caught up to growth in asset prices. Clearly, that didn’t happen.

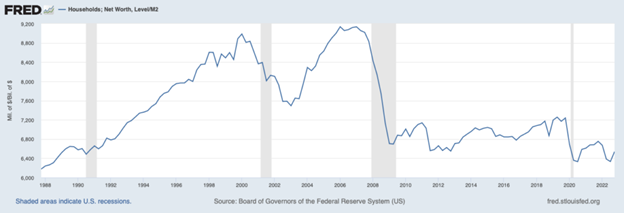

It does appear, however, as if the central bank did at least accomplish the first half of Bernanke’s mission (boosting wealth) even if it didn’t quite accomplish the second half (kickstarting a virtuous circle of economic growth). But when you look at household net worth relative to the growth in the money supply, it’s clear that the rise in the former was nothing more than an illusion. Net worth has actually declined relative to M2 since 2008 and is now back to levels not seen in the 20 years prior to that time. The truth is that there has been no “real” wealth created at all when measured this way.

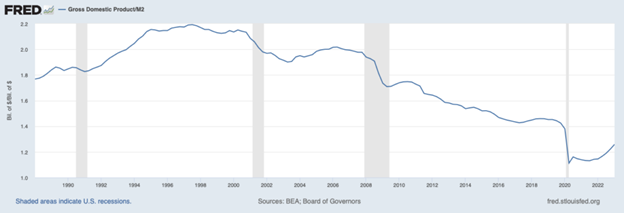

And when you deflate GDP by the growth in the money supply, the picture is even more damning. Since quantitative easing began in 2008, the trajectory of the economy in relation to the growth of M2 has been far more deeply negative than that in household net worth. The truth is that there has been no “real” growth in the economy since 2008 when it is measured in this way; in fact, the economy has been in protracted decline relative to the money supply for decades, a phenomenon that has only worsened during the QE era.

As today’s CPI report reminds us, after decades of disinflation the most recent round of money printing has led to the return of inflation. At the end of the day, it may not be the economy or household net worth but inflation that the central bank’s great monetary experiment has been most effective in stoking. Of course, history could have told us that would be the likely outcome long before Bernanke ever began firing up the printing press. And its failure to heed the warnings of history may help to explain why confidence in the Fed is now at an all-time low, a trend that may only exacerbate the inflation problem over time.

Learn more about Jesse Felder at TheFelderReport.com.