Close...but no cigar. That’s how I’d characterize inflation these days, at least from a policymaker perspective.

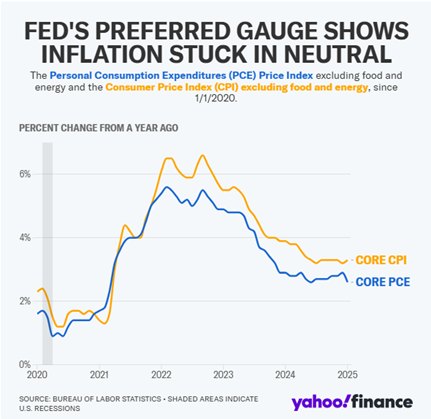

Check out the MoneyShow Chart of the Day here. It shows the year-over-year change in the two main “core” (excluding food and energy) inflation readings we get each month. One is the Consumer Price Index that was released in mid-February and the other is the Personal Consumption Expenditures Price Index that we got on Friday.

The core PCE rose just 2.6% year-over-year in January, down from 2.9% in December and the smallest increase in seven months. That’s the good news.

On the other hand, the CPI rose 3.3% YOY in January. That was up from 3.2% in December, halting progress toward the 2s. So...bad news.

Right now, the federal funds rate target range is 4.25% - 4.5%. The Federal Reserve’s next policy meeting ends on March 19. Rate futures markets are pricing in only a very small chance (less than a 7% probability) of another 25-basis point cut then. That’s far below the 31% chance being priced in at the end of January.

You have to go out to the June meeting to find the percentage of a cut being greater than a coin flip (56% as of Friday). And it’ll take more PCE-ish data – vs. CPI-ish data – to get those figures to swing further in the doves’ favor. That, in turn, means traders will be trading without the benefit of an implied “Powell Put” for at least a while longer.