Peace discussions, ceasefire headlines, and renewed tension around the Strait of Hormuz continued to shape the cross-asset front last week in markets. Yet despite the fog of war, the equity campaign delivered an important internal message, writes Buff Dormeier, chief technical analyst at Kingsview Partners.

The headline battlefield looked bearish. But beneath the surface, the broader ranks began to show signs of renewed strength.

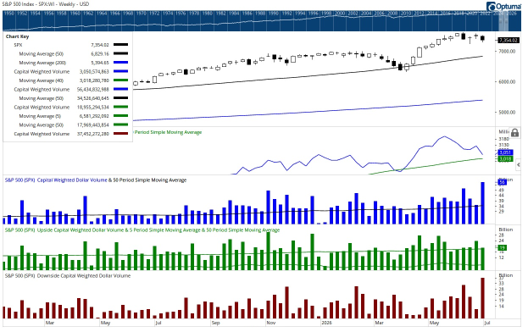

For starters, the week produced the largest downside Capital Weighted Volume reading since Aug. 2, 2024, the period that sparked our “And Then There Were None” campaign. Weekly Capital Weighted Volume was the largest since the Apr. 11, 2025 record-setting week, with 69% of volume trading to the downside. That is a heavy artillery print from the bears.

S&P 500 Index (^SPX)

Daily volume confirmed the pressure. Monday, Tuesday, and Wednesday showed 80% downside Capital Weighted Volume on average volume. Thursday, June 25h, followed with 82% downside volume on above average Capital Weighted Volume.

But the list of weakened units did not expand across the entire battlefield. Instead, the weakness was concentrated in the generals and the capital-weighted index. The troops advanced. The broader ranks held. The brass commanders gained. That is not a classic uniform retreat. It appears to be asset rotation.

This is the key distinction. The stock market appeared bearish on the surface, and the capital-weighted data clearly showed distribution. However, it may be a mistake to interpret capital-weighted weakness as a broad market failure. The NYSE Advance Decline Line, a key metric we have been waiting on for direction, finally broke out to new all-time highs. That is a major breadth development, a sign of improving broad health.

For now, the generals are under fire, but the troops have not abandoned the field. The key is to manage risk before it manages you, defend critical ground, and let volume confirm whether this is rotation or retreat.