Goldman Sachs’s volatility desk just noted that the CBOE Volatility Index (^VIX) is back to its lowest levels in more than a month, while one-month S&P 500 Index (^SPX) implied correlation is near its lowest level in 20 years. While a low VIX can convey a sense of market calm on the surface, implied correlation tells a different story, writes Lance Roberts, editor of the Bull Bear Report.

The VIX, based on option trading data, measures the implied volatility of the S&P 500. A low VIX means traders expect the market to be relatively calm with not much volatility. Conversely, a higher VIX reflects expectations for high levels of volatility. Today, the VIX is relatively low around 17, as S&P 500 index option trades appear complacent.

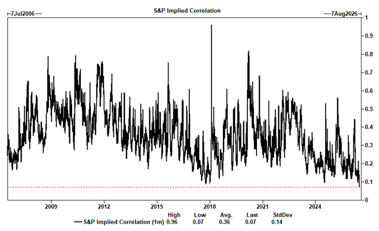

Implied correlation measures how much S&P 500 stocks are expected to move together. When implied correlation is high, as it was during Covid, the 2022 interest rate shock, and more recently at the beginning of the Iran conflict, macro forces dominate trading activity, and stocks tend to go up or down together.

When correlation is low, stocks decouple. Individual company fundamentals, technical setups, and momentum chasing drive returns. As we see in the chart here, the implied correlation is at a 20-year low.

The low VIX implies smooth sailing ahead, while a record-low implied correlation suggests the market could be at risk. Goldman is hedging the risk of a correction, i.e., an implied correlation spike.

Often, when implied correlation rises sharply from extreme lows, as it did in August 2024 during the yen carry trade unwind, the divergences that kept the index calm disappear. Stocks start moving together again, and most of the time they move down. This condition is not a warning to expect a market downdraft, but it does suggest that risk awareness is critical.