Everybody talks about Big Tech. But “Big Finance” is going to have its day in the sun sooner this earnings season. So, where do things stand with banks, brokers, insurers, and specialty lenders heading into next week’s Q2 reports?

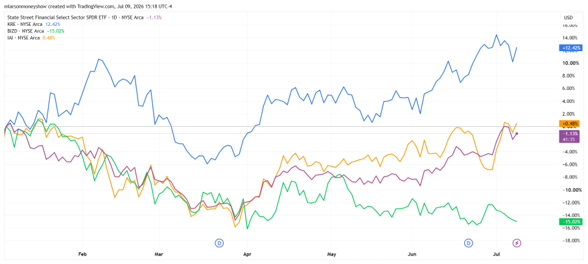

Let’s start with the MoneyShow Chart of the Day. It shows how four different sector ETFs have performed year-to-date. They include the State Street Financial Select Sector SPDR Fund (XLF), State Street SPDR S&P Regional Banking ETF (KRE), VanEck BDC Income ETF (BIZD), and iShares US Broker-Dealers ETF (IAI).

XLF, KRE, BIZD, IAI (YTD % Change)

Source: TradingView

You can see there’s a WIDE dispersion of returns. Regional banks (KRE) are leading with a gain of 12.4%. So-called Business Development Companies (BIZD) that lend to riskier or smaller companies are lagging with a loss of around 15%. The sector overall (XLF) is slightly positive on the year, while the brokerages and exchanges (IAI) are slightly negative.

If you’ve been following my work, you know the story with BDCs. They’ve been struggling for a few quarters now due to concerns about private credit risk (in other words, risk in the “non-bank lender” space). On the flip side, regional banks have performed well because of a favorable yield curve and the recent decline in oil prices, which improved the loan delinquency outlook.

Starting on Tuesday, July 14, investors will get a deluge of reports from mega-banks like JPMorgan Chase & Co. (JPM) and Bank of America Corp. (BAC). Smaller institutions will follow soon after.

Pay close attention to what executives say about loan growth, credit risk, the impact of the recent deluge of Initial Public Offerings (IPO), and core lending margins. It could be the key to the sector’s next major move – not to mention give you something to talk about until Big Tech grabs the microphone later!