It’s official: The first half of 2024 is over...and the second half is getting underway. That makes now a GREAT time to look back at which assets are winning the performance race...which are bringing up the rear...and which are stuck somewhere in between.

Here’s the MoneyShow Chart of the Week to break it all down for you!

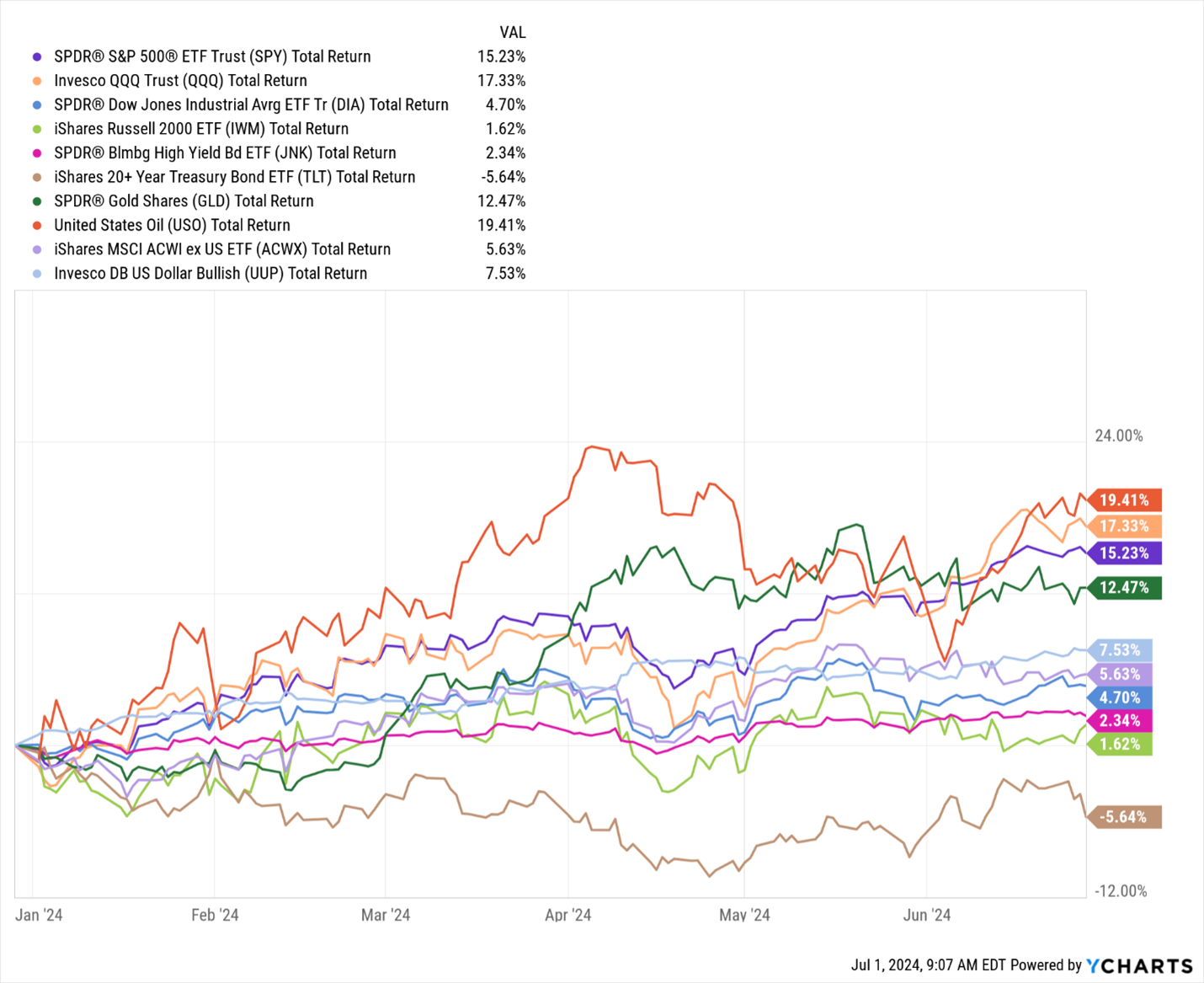

Data by YCharts

Technology stocks get all the press, and it’s easy to see why with the Invesco QQQ Trust (QQQ) spinning off a total return of 17.3% year-to-date. But the United States Oil Fund (USO) actually delivered the best performance of the ETFs I tracked: +19.4%. Go figure.

The SPDR S&P 500 ETF Trust (SPY) notched a gain of 15.2%, while the SPDR Gold Shares ETF (GLD) returned 12.4%. In part because the dollar rallied strongly – with the Invesco DB US Dollar Index Bullish Fund (UUP) up 7.5% -- global markets didn’t fare as well as US ones. The iShares MSCI ACWI ex US Index Fund (ACWX), a benchmark ETF for non-US markets, rose just 5.6% in H1.

Here at home, you know the drill: “Old Economy” stocks and small caps haven’t been keeping up with their flashier, bigger-cap brethren. That’s why the SPDR Dow Jones Industrial Average ETF (DIA) managed a gain of just 4.7%, while the iShares Russell 2000 ETF (IWM) rose a paltry 1.6%.

As for bonds? It’s a mixed bag. Riskier bonds clearly outperformed credit-risk-free government debt, with the SPDR Bloomberg High Yield Bond ETF (JNK) closing out H1 with a 2.3% gain…while the iShares 20+ Year Treasury Bond ETF (TLT) lost 5.6%.

As for S&P 500 sectors (not shown above)? The Communication Services Select Sector SPDR Fund (XLC) came in first place with a return of 19.6%, followed by the Technology Select Sector SPDR Fund (XLK) at plus-17.9%. The Real Estate Select Sector SPDR Fund (XLRE) was the only one of 11 sector funds to LOSE money at minus-2.4%. Second-worst was the Consumer Discretionary Select Sector SPDR Fund (XLY) with a 2.4% gain.

What’s the message from the Chart of the Week and the data accompanying it? The market remains in bull mode, with offensive sectors and assets outperforming defensive ones. We could use better market breadth. But the lack of it isn’t a rally killer by itself.

Unless and until the positive tone and data changes course, I’m sticking with the bullish story I’ve been telling since the beginning of 2023. Be bold. Stay bold.