I’ve had precious little personal experience with cannabis, but an increasingly cannabis-friendly Capital Hill makes me think it’s time to educate myself, asserts Adam Johnson, editor of Bullseye Brief.

The House recently passed a bill to make marijuana fully legal on a federal basis, and debate now moves to the Senate. Federal legalization would be a game-changer, facilitating interstate commerce, normalized banking, institutional stock ownership and an influx of tax revenue.

Since only five states still consider marijuana 100% illegal, while a majority allow doctor-prescribed medical use, I think mainstream acceptance is well on its way. In this brave new world, I want to own the highest quality, best established operator in the sector… and its stock could double from here.

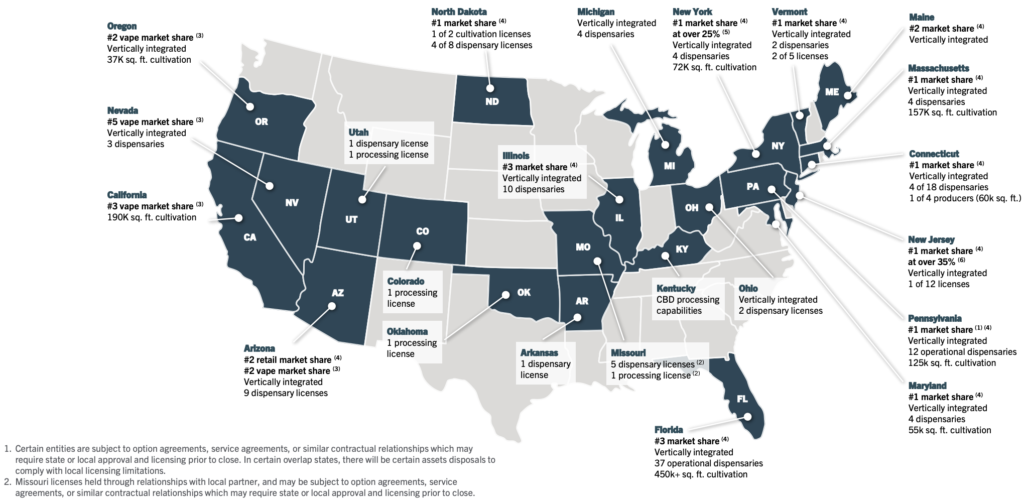

Curaleaf Holdings, Inc. (CURLF) operates the country’s largest vertically-integrated cannabis business, with cultivation facilities and retail dispensaries across 23 states.

The company also maintains a robust third-party distribution platform using 2,000 vendors. Sales grew 161% last year and are on track to double this year, powered by nineteen regional acquisitions since its IPO in 2018.

No competitor can match Curaleaf’s estimated $1.3B in sales this year, and its localized capability has become a significant strategic advantage, since Federal regulations currently forbid interstate commerce of marijuana and products containing THC (only CBD-infused products can move freely).

Marijuana is relatively simple business. You grow the plant, harvest its buds, then extract the two defining chemicals (CBD and THC) to make edibles and essential oils… or you simply chop those buds into tobacco and smoke it.

While CBD is legal and relieves pain, THC is not yet federally legal and does a lot more than relive pain. When doctors prescribe marijuana for medical use, the product typically contains both chemicals. Curaleaf’s diverse line of marijuana products serve both medical and recreational clients.

The Curaleaf investment thesis is straightforward: Curaleaf is already the #1 integrated cannabis operator in the US, the global cannabis market is expanding quickly, and the stock is cheap. Several key facts and figures lend support.

• Presence & Breadth – 30 growing facilities and 102 retail locations across 23 states with 2,000 wholesale partners.

• Capital Acceleration – Cash generation (EBITDA) goes from $144M in 2020 to $375M this year and $575M in 2022.

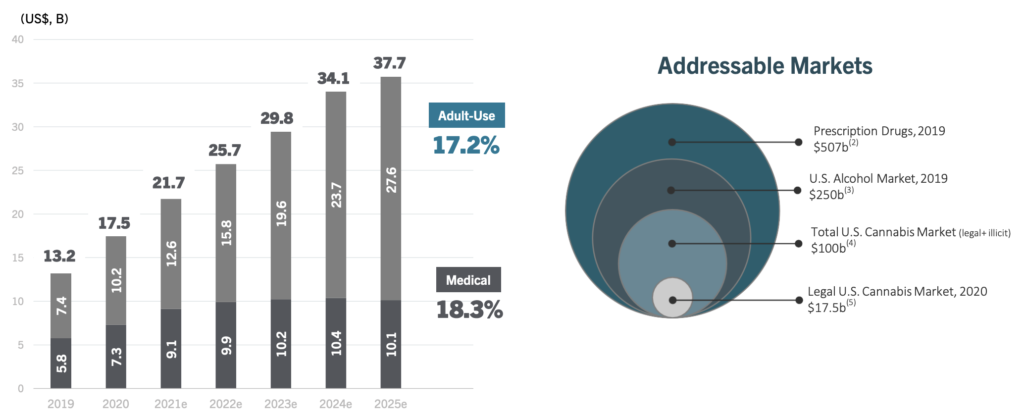

• Industry Growth – The Cannabis industry is expected to double in size by 2025 ($37B) and create 300k new jobs.

Curaleaf shares trade about 5 times next year’s estimated sales, which is in the middle of where peers trade (2-8x). Arguably, its dominant footprint and superior sales growth should command a premium, but its status as a serial acquirer means that it’s always adding to its share count, even if deals are typically accretive. I’m applying a multiple of 6.5x, since that’s where established liquor producers trade… I think that’s a fair comp.

I also look three years out to 2024 sales, since sales are growing so quickly. If federal legalization occurs next year, likely attracting an influx of institutional capital, I think the multiple will re-rate higher, and my target will prove low.

I like owning CURLF at the lower end of its recent trading range, which also coincides with an upward-sloping 200-day moving average and a longer-term trend line. I like seeing convergence of multiple support levels.

My target of $29 derives from multiplying projected 2024 revenues of $2.9B by an assigned Price to Sales multiple of 6.5x, discounted at 3% annually and divided by shares outstanding. $29 = (($2.9B x 91%) x 6.5) / 610M.