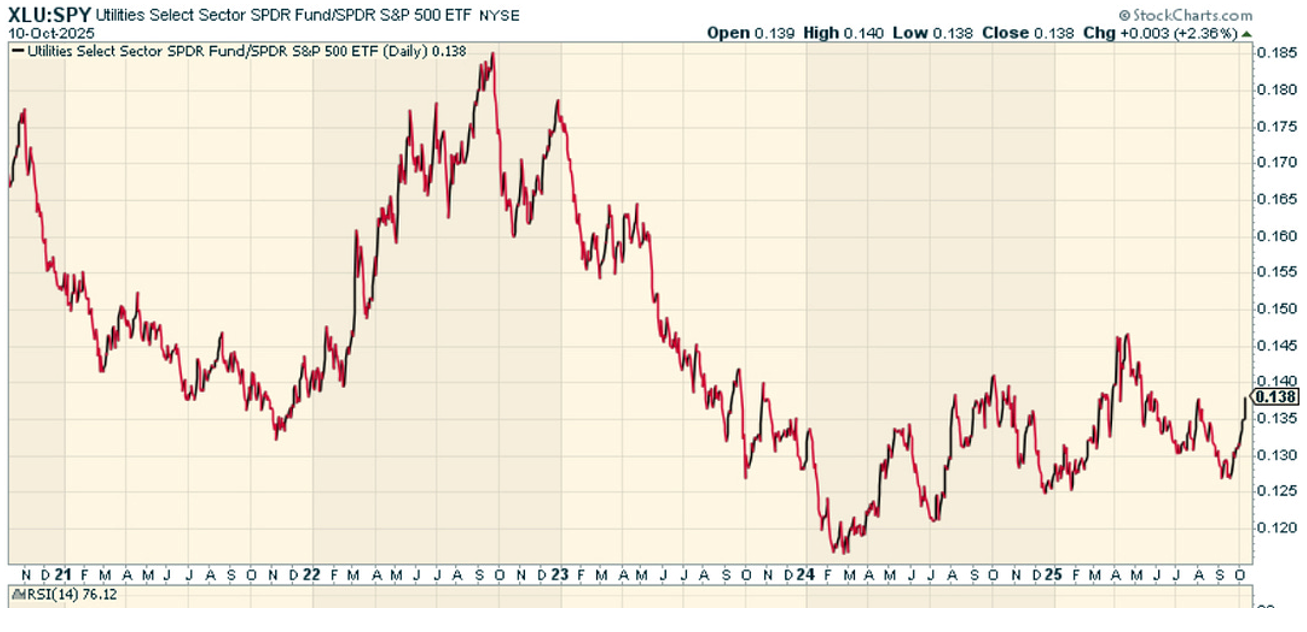

Utilities tend to do better than other stocks in the weeks leading up to volatility spikes, providing an early warning smart money is getting ready for a move to defense. The sell-off on Friday, Oct. 10 confirmed in dramatic fashion, writes Michael Gayed, editor of The Lead-Lag Report.

The chart here — a plot of the Utilities Select Sector SPDR Fund (XLU)/SPDR S&P 500 ETF (SPY) ratio over time — showed utilities pressing higher compared to the broader market, indicating that risk-averse flows had started weeks ago. That ratio’s tendency to tilt higher was exactly the sort of defensive signal we’ve seen in the past prior to surprise equity drops.

The carnage Friday was particularly brutal for regional banks. The SPDR S&P Regional Banking ETF (KRE) fell 4% on the day, notching its eighth decline in ten days and a combined two-week loss of more than 6%. The collapse is not due to tariffs. It’s symptomatic of deposit-cost pressure, soft loan demand, and heavy exposure to commercial real estate — particularly offices that are still under refinancing stress.

At the same time, we have seen this chasm emerge between private credit stress and public equity optimism. The private credit market includes more than $2 trillion of assets (as an estimate). It experienced a breakout year in 2021–22, frequently under covenant-light or payment-in-kind agreements.

As those loans mature — or refinance at far higher rates and with volatile corporate earnings — they are poorly positioned. Rolling defaults are expected to rise until the 2026–27 timeframe. This stress has not been fully priced in by public equities.

So, we have a divergence: Credit markets are marking down risk, while indices are being lifted by a narrow group of winners. The sell-off that began Friday may be the beginning of stocks catching down to credit reality.