Bread Financial Holdings Inc. (BFH) successfully navigated a complex credit environment to deliver a full-year 2025 performance that met all key outlook targets. The narrative was defined by structural efficiency rather than top-line expansion, notes Philip MacKellar, editor of Contra the Heard.

Revenues remained flat compared to 2024, aligned with expectations, but EPS nearly doubled from $5.58 to $11.07. The net loss rate was 7.7%, inching out internal projections. The average loan balance nudged lower, but credit sales rose 3%.

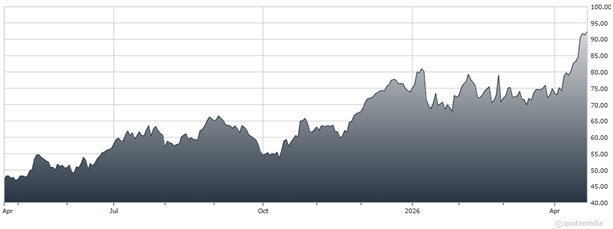

Bread Financial Holdings Inc. (BFH)

During the year, the enterprise diversified its partner portfolio through new relationships with Cricket Wireless, Crypto.com, and Vivint. At the same time, Bread fortified its presence in the home retail sector by expanding agreements with Bed Bath & Beyond, as well as Raymour & Flanigan.

Meanwhile, Bread boosted the dividend 10% and repurchased 5.7 million shares last year at an average price of $54 — a total outlay of nearly $308 million. Looking ahead, revenues and the average loan balance are projected to edge up in the low single digits this year, while the net loss rate is expected to fall slightly.

In February, the corporation unveiled a $600 million buyback on top of $165 million left over from last year. That brought the total current authorization to $765 million, roughly a quarter of the market cap. Of course, they may not deploy all this capital, but if they did, it would represent a buyback bazooka.

In January, the Trump Administration proposed a 10% cap on interest rates in an attempt to improve affordability and address falling polling numbers. So far, the idea has fizzled amid industry backlash and concern among lawmakers in Congress.

Recommended Action: Hold BFH.