Nephros, Inc. (NEPH) provides water filtration solutions for medical and commercial customers. After years of strategic resets, Nephros now operates around a focused filtration platform, combining medical-grade products for higher-sensitivity applications with commercial products, notes Faris Sleem, editor of The Bowser Report.

The company’s core business is medical filtration, where its FDA 510(k)-cleared Class II devices are used in infection control and dialysis water applications. Commercial filtration extends the business into recurring-use settings such as ice machines, coffee and tea makers, bottle fillers, food and beverage equipment, and drinking fountains.

The company is shifting toward programmatic recurring replacement demand. Nephros’ infection-control and commercial filtration products can generate recurring replacement orders, while emergency or outbreak-related demand adds episodic upside. Management is also trying to convert more one-time customers into programmatic customers, which would make revenue more predictable over time.

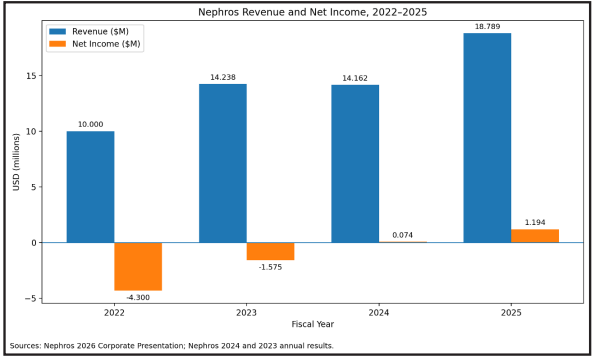

For 2025, Nephros reported revenue of $18.8 million, up from $14.2 million in 2024. Gross margin held steady at 62%, assisting net income in its rise from $74,000 to $1.2 million.

First-quarter results for 2026 were not as spectacular. Revenue continued its steady trend up, while net income and EBITDA were both down. A big factor was the decline in gross margin to 57% from 65% in the prior year period, which was largely due to the decline of the US dollar relative to the euro.

The game plan moving forward is for the company to focus on programmatic growth, which grew 23% year-over-year. Aside from potential tariff headwinds, we expect margins to hold steady and revenue growth to maintain.

Recommended Action: Buy NEPH.