The early action on “Fed Days” like this one doesn’t matter much, since it’s likely to change once we get the news later. But for now, stocks and Treasuries are modestly higher while crude oil is giving back a bit of its recent gains. The dollar, gold, and silver are flattish.

On the news front...

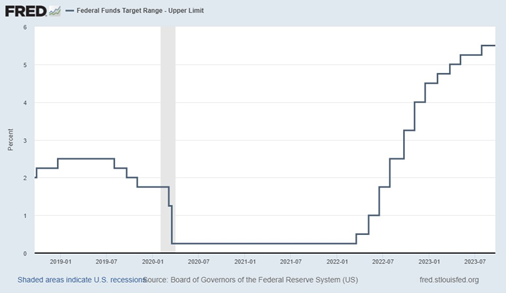

The Federal Reserve will conclude its two-day policy meeting today, then announce its interest rate decision at 2:00 pm Eastern. We’re all but guaranteed to see the second “Powell Pause” of this interest rate cycle, with the Chairman and his fellow policymakers holding rates at the current 5.25% - 5.5% range.

The Fed previously left rates unchanged at its June meeting after hiking rates 10 consecutive gatherings in a row. Then it raised them another 25 basis points in July. Many members of the Fed want to proceed more cautiously to avoid tipping the economy into a full-blown recession rather than securing a soft landing.

Federal Funds Rate Target (Upper Limit)

Another day, another successful Initial Public Offering. Not long after Arm Holdings (ARM) went public and traded well on its first day, grocery delivery firm Instacart (CART) did the same. The firm raised $660 million selling shares at $30 two days ago, then the stock opened at $42 yesterday before ultimately finishing up 12% on the day.

Not too hot, not too cold worked for Goldilocks and it worked for Wall Street here. Expect more IPOs to follow, even as the $21 billion raised so far this year pales in comparison to the $250 billion in stock sold during the Dot-Com-Bubble-like mania in 2201.

Finally, the housing market remains in the doldrums thanks to higher mortgage rates and the ongoing affordability crisis. Housing starts slumped 11.3% in August to an annualized rate of 1.28 million, the lowest since 2020. A separate index of builder optimism dropped sharply for the second month in a row.