Stocks are rallying from overnight lows, though still largely marking time amid ongoing Middle East concerns. Gold and silver are pulling back, while crude oil has given back some recent gains. Treasuries and the dollar are modestly lower.

The Middle East crisis continues to dominate the attention of markets. President Trump has announced a two-week deadline for diplomatic talks to proceed on the Iran-Israel conflict. The US could jump into the fray after that (or sooner) to help Israel further damage Iran’s nuclear and missile research and weapons programs. European foreign ministers and Iranian officials are holding talks in Geneva today.

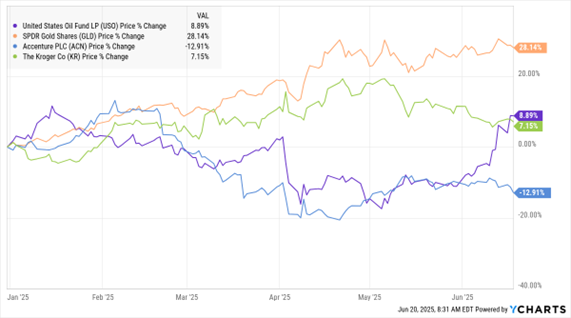

USO, GLD, ACN, KR (YTD % Change)

Data by YCharts

Crude oil markets have a $7-$8 per barrel “war premium” built into them right now. Gold has also been supported by the “safe haven” bid. Both commodities could give back some ground if we see any substantial de-escalation.

We’re in a corporate earnings lull, with the second-quarter reporting season not set to start for a couple more weeks. Analysts are expecting Q2 earnings growth of 4.9% for S&P 500 companies, down from 13.3% in Q1, according to FactSet. Still, a few reports are trickling in – and getting noticed.

Shares of the giant consulting firm Accenture (ACN) slid after contract bookings dropped 6% to $19.7 billion. It’s vulnerable to spending cutbacks by the US government given its federal contract exposure. For its part, grocery store chain Kroger Inc. (KR) raised its sales growth forecast for the year – though it highlighted how uncertain its outlook remains due to US economic concerns. Coming into today, ACN was down 12.9% while KR was up 7.1% year-to-date.