Weak manufacturing numbers along with the killing of Iran's most powerful general, has increased risk across all market sectors, reports Adam Button.

Most global indices are off their lows of the day, but the dangers surrounding the trigger of the selloff are by no means over. Adding to it today's release of the worst U.S. manufacturing ISM reading in over 10 years, and more questions arise. President Trump's ordering of the U.S. killing of Iran's most powerful general will pressure Iran into a possible retaliation on U.S. military interests in the region or those of U.S. allies. The spike in oil prices, along with the $20 jump in gold, 4% decline in bond yields and 21% jump in the VIX bear the trademark of a geopolitically driven shock to risk appetite.

But let's not forget what happened earlier in the week. China cut rates Thursday in a further boost to global growth, but PMI readings showed that manufacturing remains in a rut. We continue to keep a close watch on global manufacturing.

The global economic slowed in mid-2019 on the combination of higher interest rates and the trade war. Since then the Fed and others have lowered rates and now, we have a ceasefire in the trade war.

Leading vs Lagging

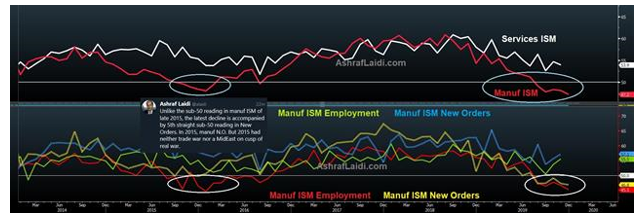

With regards to U.S. manufacturing, Ashraf reminds us that the latest deterioration in manufacturing ISM stands out from that of 2015 in that it is now joined in contraction territory by the New Orders index, which is a true leading indicator--unlike employment.

Some things like real estate have quickly turned around and stock markets are clearly pricing in more of the same, yet manufacturing is still soft. A few manufacturing surveys were out Thursday and the theme was a continued flatline.

A good spot to watch is the JPMorgan global PMI because it aggregates all the Markit indexes. It started 2018 at 54 then slowly sank to 49.3 into mid-2019. The latest number was out today at 50.1, which is barely expanding and lower than the previous month.

If the theme this year is strengthening global growth, then it has to show up in manufacturing. The market probably has two to three months of patience as the trade deal, Brexit and rate cuts work their way through, but it doesn't begin to materialize, the worries will start.

Hand-in-hand with that goes China. The Peoples Bank of China (PBOC) cut the RRR by 50 basis points Wednesday and we expect to see a cut in the LPR by 20-30 basis points in Q1. If China continues to stimulate then commodity currencies and commodities stand to benefit.

In terms of seasonals, there are some strong tendencies but lately the trends have faded. The traditional January effect is for stock market strength but that hasn't been true over the past decade. What's more true, is that risk trades do well in the first week of the month followed by softness thereafter.

In FX, it's the second weakest month for the Aussie (AUD), Canadian (CAD) and New Zealand dollars (NZD), but the past three years have bucked the trend so be wary.

One of the strongest seasonal patterns anywhere is gold in January. It's by far the best month. Crude oil, meanwhile, tends to soften in January and then rally from February through April.