There are clearly reasons to continue giving this bull market the benefit of doubt, but the risks are rising and that means a defensive approach is warranted, cautions Jim Stack, market historian, money manager and editor of InvesTech Research.

The persistently strong economy and lack of definitive bearish technical warning flags currently give credence to a positive outlook. However, the monetary climate is becoming less accommodative, and that’s more critical in determining our strategy at this stage, particularly given the public’s addiction to ultra-low interest rates.

While we won’t rule out another rally to new bull market highs as the year progresses, one should be cautious in committing new or additional money to stocks, particularly over the near-term. One reason is seasonality…

Historically, the summer period from May 1 through October 31 has been the weakest part of the year on Wall Street. Most of the market gains typically occur during the winter months from November 1 through April 30.

Over the 58 years since 1960, the S&P 500 has averaged a gain of 6.8% for the winter period, while the summer average is only 1.0%.

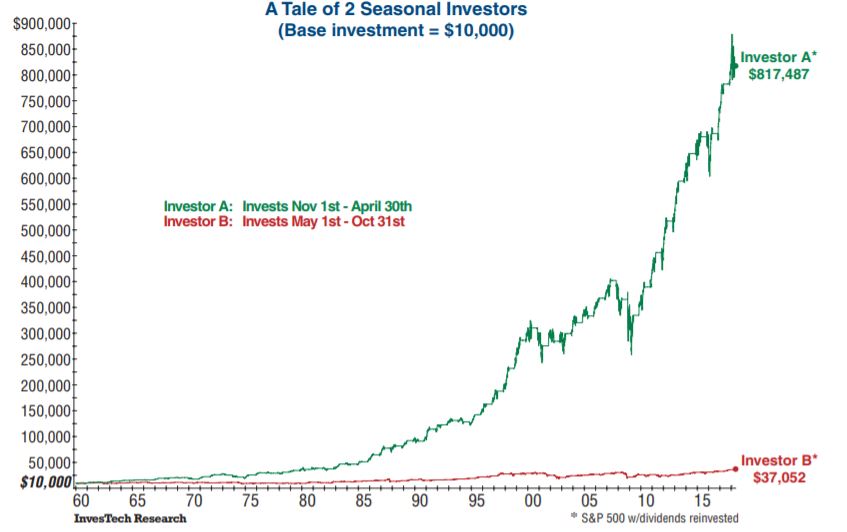

One of our favorite graphs illustrating this phenomenon is “A Tale of 2 Seasonal Investors” shown below, which illustrates this seasonal bias over the long-term. In this comparison, each investor starts with $10,000 in 1960 and invests in an S&P 500 Index Fund for six months each year.

Investor A chooses the November through April period, while Investor B invests during the opposite months from May through October. Over the 5+ decades shown, the difference in outcomes is dramatic!

Investor A sees an 81-fold increase in value, while Investor B’s portfolio has little more than tripled. Given this seasonal discrepancy, the quip “Sell in May and Walk Away” has become a Wall Street mantra.

Practically speaking of course, it makes sense to remain invested over both periods as summer gains, although often meager, contribute significantly to long-term compounding.

Even so, the six months from May through October seem to have a higher propensity for negative returns or selloffs than the winter period. Since 1960, the summer months have ended with 21 negative S&P 500 returns versus 14 for the winter months.

Of those negative periods, there have been 7 double-digit declines for the May-October period, compared to 4 such excessive drops for the November-April period.

Perhaps more important to investors looking for a market rally this year is the strength usually associated with the winter period. Not only does the six month November-April period end in positive territory more often than its summer counterpart, but the winter months since 1960 have tallied three times as many double-digit gains (21 versus 7) as the May-October periods.

Hypothetically, a rally to new highs in this current bull market, if it occurs at all, is more likely in the latter part of the year. In the meantime, with the tradition for summer weakness in the stock market and the uncertainty of the current environment, our defensive allocation is still appropriate.