Toronto-based Franco-Nevada Corp. (FNV) finances mines instead of operating them. And I like that a lot. It means Franco collects cash flows from mine production — without such “wildcards” as exploration costs, permitting worries, environmental fallout, or cost overruns, writes Bill Patalon, chief stock picker at Stock Picker’s Corner.

Those are very real problems miners face. But with this strategy, those problems stay with the operator; Franco-Nevada has financial claims on what the miner churns out. It makes money in two ways…

- Royalties: 2% to 5% of a mine’s revenue, usually for the multi-decade life of that operation.

- Metals Streams: In return for an upfront cash payment to the miner, Franco-Nevada gets the right to buy a percentage of the production, usually at a mere 20% to 30% of the metal’s spot price.

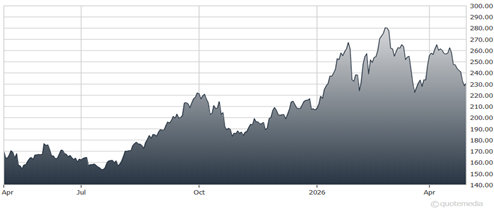

Franco-Nevada Corp. (FNV)

On the royalty front, if a mine produces $1 billion worth of gold, a 3% royalty agreement pays Franco $30 million a year — automatically. On the streaming side, if gold is $2,500 and Franco-Nevada’s stream price is $500 an ounce, the per-ounce margin is $2,000.

Revenue hit $1.82 billion last year — a record result buoyed by the surge in metals prices. Operating cash flow approached $1.49 billion. Once metals resume their surge — as we believe they will — those results could get even better.

Analysts have a one-year target price of $306.33 on Franco-Nevada, a projected gain of 32% from its recent price of $233. And the “high estimate” is $354 — which would be a 52% gain.

That’s just for starters. It’s the “investment leverage” that’ll really pay off: As gold soars in price, Franco’s flow of cash will increase. That’s money it can deploy to strike new deals, pay down debt and — ultimately — return cash to shareholders via buybacks or with dividend payouts.

Recommended Action: Buy FNV.