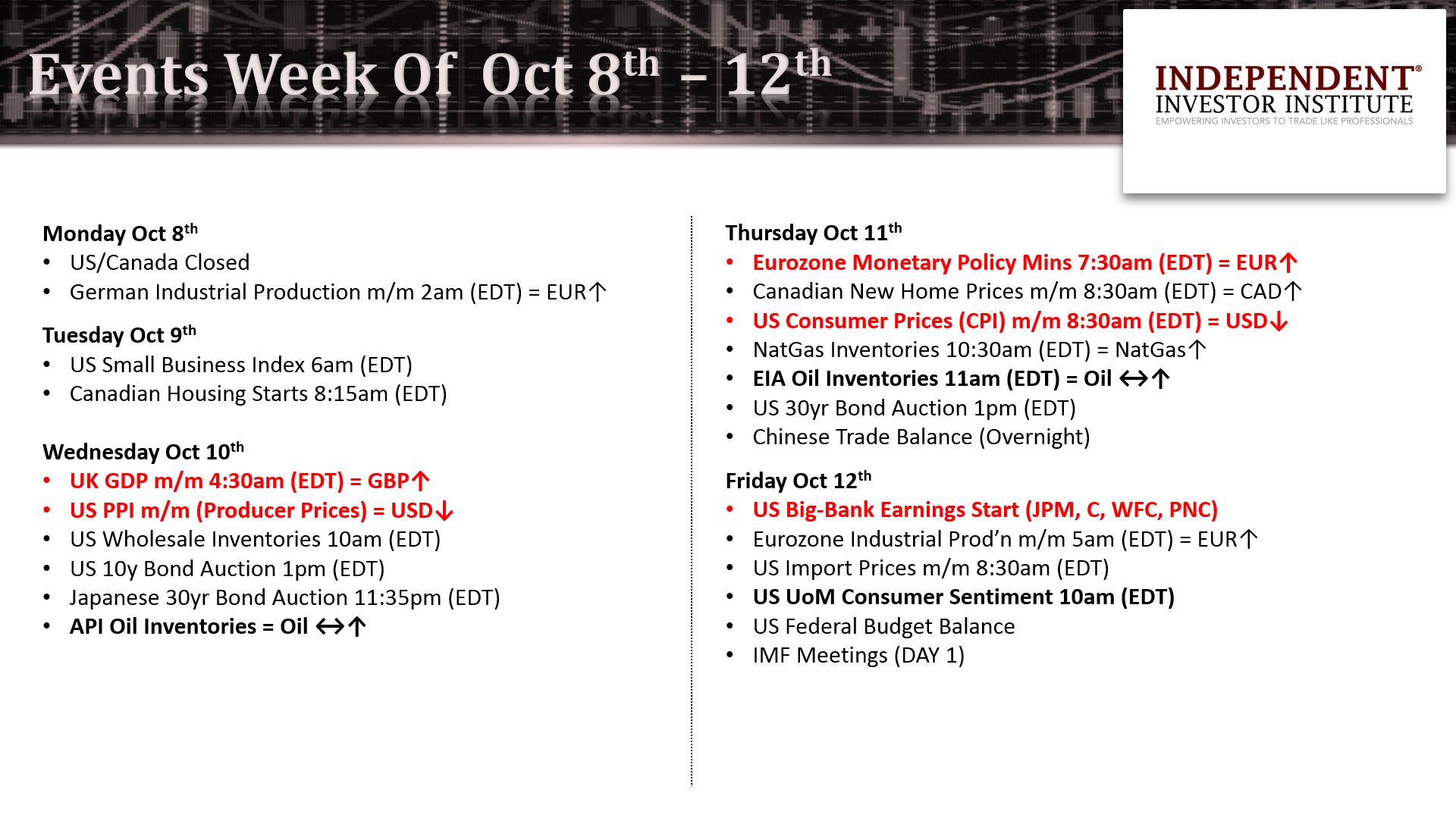

Has the perfect storm hit markets? Will the slide continue? Or is a relief-bounce ahead of us? This report will help answer these questions and prepare you for the week ahead, writes Ziad Jasani Monday.

At the Independent Investor Institute, our online community of active & affluent investors/traders were guided to lower short-to-mid-term long-side equity risk exposure as of Friday, September 21.

View my weekly strategy session video here.

Recorded: Oct. 5, 2018.

Duration: 1:29:03.

Through our suite of global macro analytics, we ascertained higher risk-levels leading into Jerome Powell’s FOMC Policy Statement on September 26, albeit we were optimistic, looking for a less hawkish tone from him. Powell sang a pro-growth and pro-interest rate normalization policy song and Mr. Market (Equities) sold-off.

Last week, Powell’s two informal speeches entrenched the same message, all the while Global Bond Markets (BND+BNDX) plummeted. The trigger for Bonds to run scared was a strong ADP-Nonfarm Private Payrolls Report on Wednesday, Oct. 3, which printed 230,000 vs. a consensus estimate of 185,000.

This sent the US Treasury yield curve into a bear steepening with break-outs to calendar year highs. In fact, a multi-decade downtrend on the 30-year Treasury yield was broken.

As Bonds walked the plank they destabilized Equity-Markets Globally, where selling begot more selling, despite a weaker official Payrolls Report on Friday, Oct. 5.

A hawkish Fed that believes U.S. growth is immune to higher rates and global growth decelerating is what the Market reacted to, and wage inflation was the tipping-point.

Equity Markets have told us they think the Fed is policy-error-land.

Has the milk been soured, or will the decade-long-equity-buying-party continue?

From a boom-bust cycle perspective, the stimulus Trump added into the economy (tax reform, infrastructure-spending) has certainly worked, but has wholly relied on deficits and federal debt growing to biblical proportions. Which in turn will lead to fiscal austerity programs in the future, and a weaker USD.

However, for now, especially with Kavanaugh sworn in as the 114th Supreme Court justice, markets are likely to turn more optimistic for midterm elections (Nov. 6th), and become more reliant on further deficit spending to justify growth.

From a monetary policy perspective, as the Federal Reserve continues to let the bonds they bought up during the decade long QE (Quantitative Easing) program, the lower demand-side economics play out for the Global-Bond Market. Which underpins a sustained rise in Treasury yields.

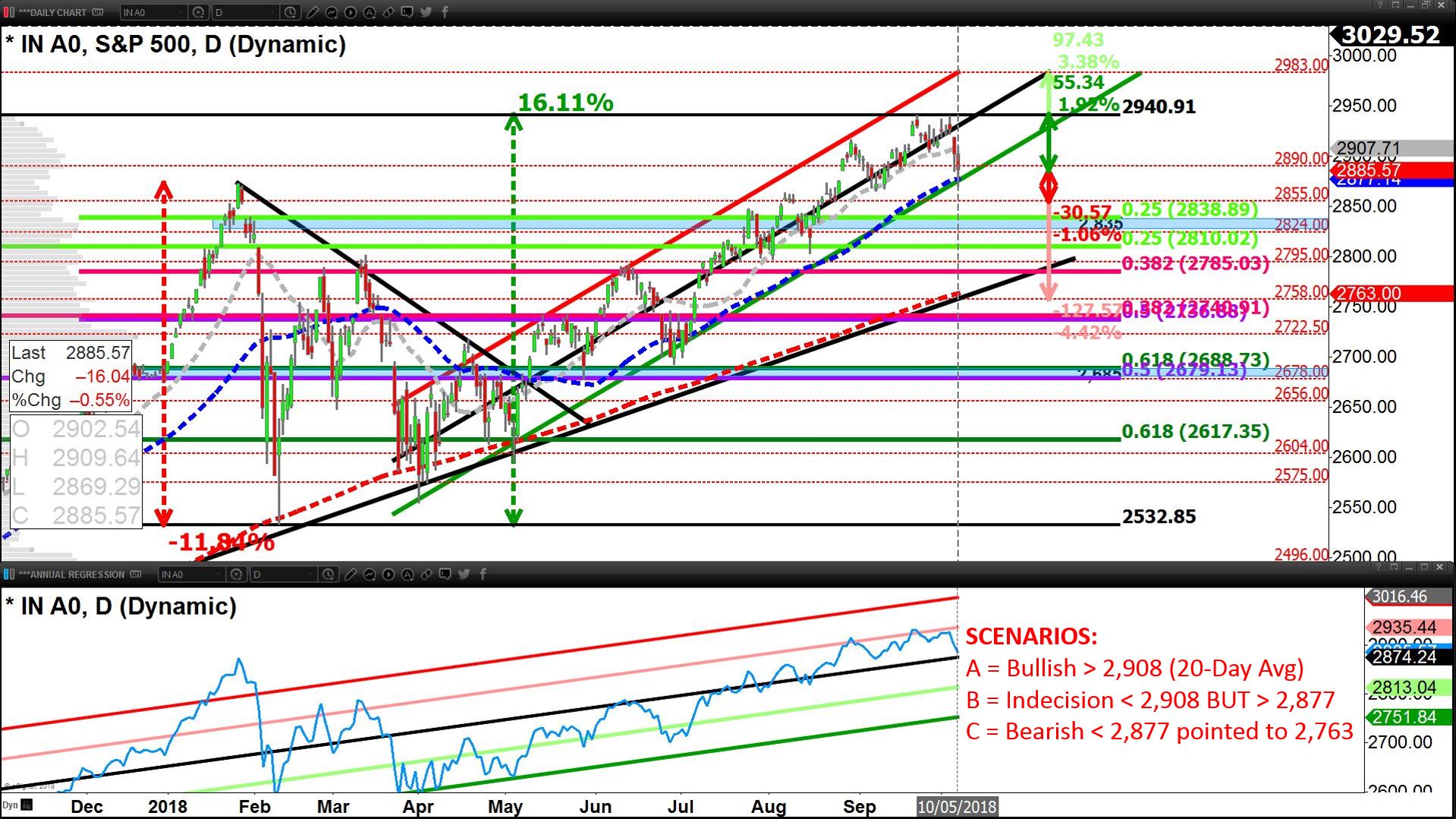

From a technical perspective, the world’s benchmark for equities (S&P 500) has shed -1.9% from September 21, 2018 all-time-highs, and remains in an up-trend channel starting March 2018, and above its 50-day average, all to be interpreted as still bullish.

From an earnings/fundamentals perspective, Q3 earnings are setting up to be another blockbuster for growth.

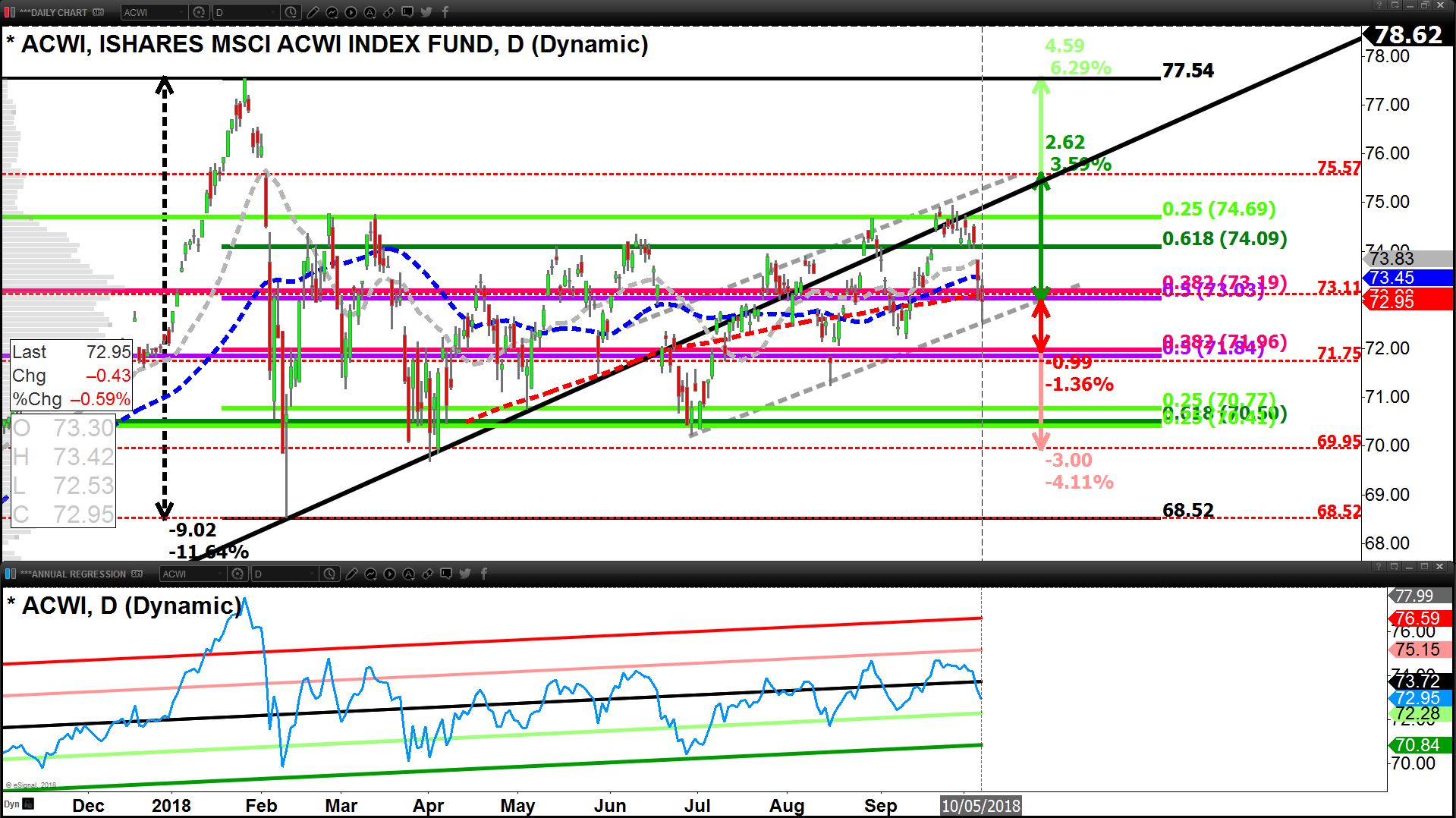

The Bottom Line: If Consumer & Producer Price Data come in cooler this week, a bounce for Stocks & Bonds becomes a reality; otherwise a test of the 200-day average (S&P 500) would be imminent, coupled with a 3%-4% drop in the Global Equity Market (ACWI).

Enjoy a complimentary-no-strings-attached 30-day subscription to Ziad Jasani’s Daily Insights. Simply send Ziad an email with FREE TRIAL in the subject: ziad.jasani@educatedtrader.com