China weakness, geopolitical risk & the U.S. Government shutdown are all weighing on U.S. economic growth expectations notes Bob Savage.

Markets are making a silk purse out of a sow’s ear. The FX market is watching the year of the Pig approach and wonders if the present risk-on mood will see a change. The British pound (GPB/USD) and Chinese yuan (CNY/USD) are not yet flashing the yellow signals that many assume would follow the headlines – where bad news bears down on prices. In the UK, the biggest defeat in House of Commons history has become a victory for the embattled prime minister with the pound higher even as the path to Brexit becomes harder. The hope is that there is a delay and/or a referendum.

The odds for such are prices at nearly 40%. This leads to UK May more likely to remain in office until June, with those odds over 50%. In China, the lack of progress on structural issues hangs over hopes for a bigger trade deal with the United States. The upcoming Chinese New Year celebrations distort the economy there and squeeze money.

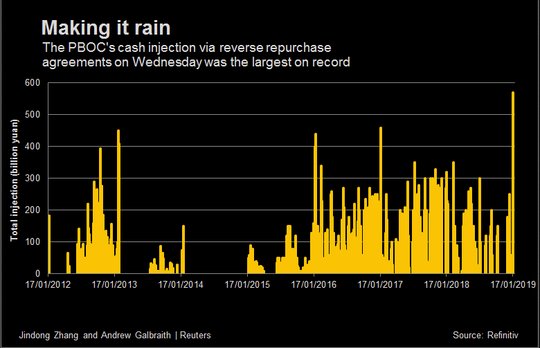

The People’s Bank of China adds a record $83 billion via reverse repos today – trying to offset the New Year squeeze and add to liquidity even after the Required Rate of Return (RRR) cuts have put another $116 billion estimated into the system, and still this isn’t enough. Further, China is seeing the easing of credit lead to the flows into less productive price gains – witness the 9.7% year-over-year house price jump in the big cities.

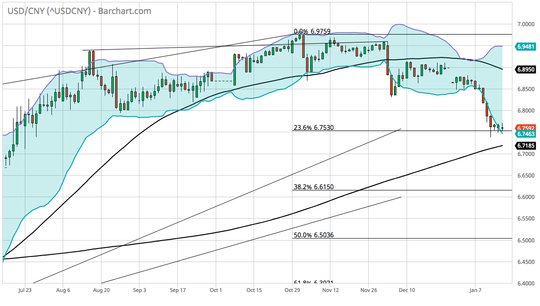

For the rest of the world, weaker Japan machinery orders, lower PPI, lower CPI in Europe and in the UK – all suggest that the disinflationary impulses from U.S.-China trade, lower oil prices, lower global trade orders – all are in the works for Q1 and leave central bankers looking a bit overdone on their quest for normalization. European Central Bank President Mario Draghi made that clear yesterday, Carney seems likely to say the same today and many of the Fed – including the hawkish Kansas City Fed President George yesterday pushed for a pause. We are in a world that is waiting for good news but can bear bad news until it overwhelms. Watch the USD/CNY as that barometer as the capital inflows that helped support it are clearly slowing and 6.71-6.73 holds.

Is the US government shutdown hurting growth expectations?

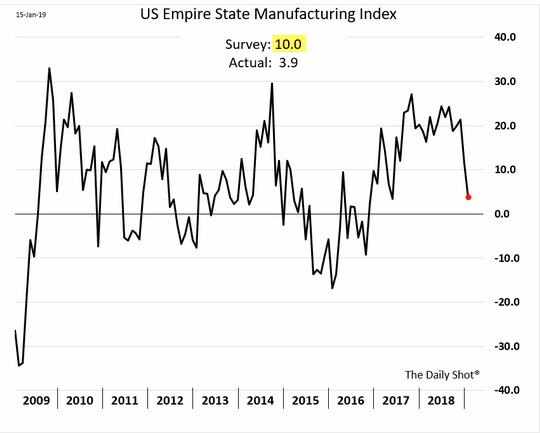

The effect of the historic partial government shutdown on markets has been modest, but now it’s beginning to hit at economic data releases and the information used by the FOMC to make its decisions. The feedback of private and FOMC surveys continue to show some economic strength for the consumer but the manufacturing sector – as shown from the NY Empire Fed yesterday is getting worse.

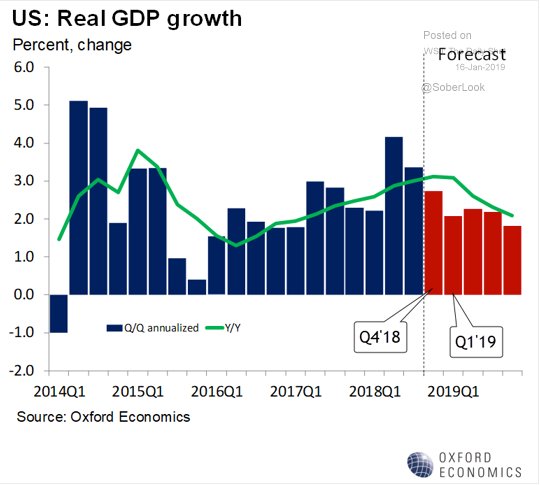

The other effect on GDP for a government shutdown is that the government spending shrinks (although it should bounce back somewhat if/when workers receive back pay). The forecasts for GDP are beginning to get marked down accordingly. The consensus on fourth quarter 2019 GDP is below 1.5%.