Slower Chinese GDP growth along with uncertainty regarding U.S.-China trade talks is driving market risk according to Bob Savage. He's presenting at TradersExpo New York March 11.

The urge to get off the road and wait out the impeding storm has been in play since 2019 started. The FOMO (fear of missing out) was countered by the JOMO (joy of missing out) in December. Memories matter less today to markets, than moods drive them, but both are in the play-offs of bulls and bears as asset markets face a heavy week ahead.

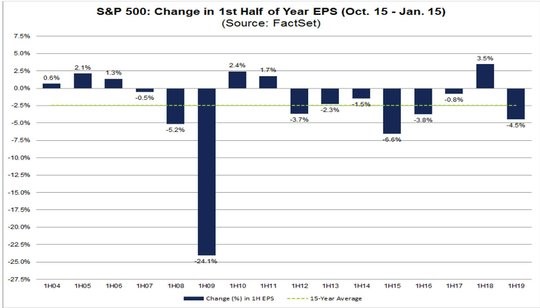

The wall of worry was climbed again last week as China/US trade deal hopes rose even as growth falls. The positioning for equities, FX and rates looks cleaner now than in the bearish start to the year but the momentum higher will need something more in the tank than hope to propel it further. In fact, the gloom over the last quarter has set into forecasts for Q1 leaving it harder to chase the market and believe in the price action. S&P 500 earnings estimates for the first half of 2019 are now the lowest in four years, according to Factset. The bottom-up EPS estimate for the first half of 2019 decreased by 4.5% (to $81.73 from $85.56) over the past three months. The price action up clashes with the mark down in earnings (see chart).

There are other anomalies to consider:

- The FOMC pause in rate hikes versus a cut and the slowing of orders and confidence and the bounce in 10-year yields against the probabilities of a FOMC rate hike in 2019.

- The weakness of survey data in Europe against the expectations of a soft-patch bounce back with German auto emissions

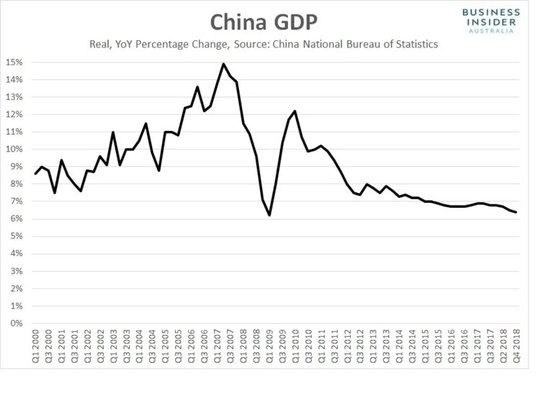

- The optimism in commodities against the weakest growth in China in 28-years based on the hopes for stimulus plans to work again

- The rally in the British pound (GBP/USD) against the worst vote outcome for a Prime Minister in the UK for over 100 years based on the hope for a Brexit delay and potentially reversal with another referendum.

Will China stimulus be enough?

The Chinese economic data for 4Q showed the slowest growth pace since 2009. The retail sales are near 18-year lows. Industrial production surprised to the upside, but fixed investments stalled.

Perhaps the most important headlines were about the US/China trade talks stuck on intellectual property issues. The net reaction of markets in Asia was positive but in Europe less so as the markets are in doubt of the veracity of the data and the power of the present stimulus overlaid against the fears of a breakdown in the trade talks. This puts this week and the craziness of the rally in risk against the well-worn fears listed above. The rally up in the USD/CNY overnight highlights the doubt in play and the need to hold 6.88 over the next few weeks as critical for those that yearn for the simplicity of buying and holding risk assets.

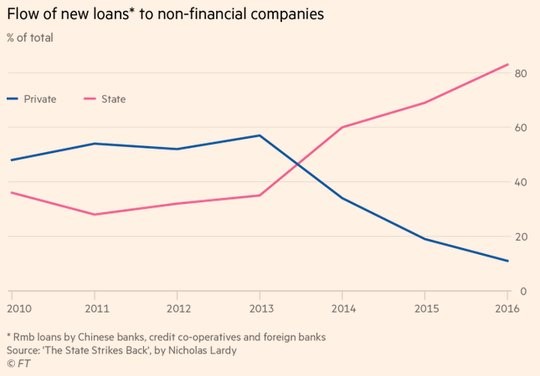

The feel-good moment for Asia post-GDP release came with the surprise uptick in China industrial production. The distraction is that electricity production zoomed higher while other things were less positive. The ability for China to grow out of the middle-income trap, to move from investment led to domestic led growth and to have a centrally controlled economy dictate the best allocation of resources for growth all that is in doubt and in play for 2019. The stimulus hopes, post the data release, remain central to global markets in 2019. The key concern is that the private sector is no longer part of the growth story (see chart).