Even relative to the market’s dovish expectations, the FOMC came off as worried about the U.S. economy, writes Matt Weller.

As we noted in our FOMC Preview report, the U.S. central bank was never going to make any immediate changes to policy, leaving traders to read Chairman Powell and Company’s tea leaves for implications about future tweaks. As it turns out, the tea leaves were clear: The Fed has undergone a major dovish shift.

Even relative to the market’s dovish expectations, the FOMC came off as worried about the U.S. economy:

- The median policymaker now expects U.S. GDP to rise just 2.1% in 2019 (down from 2.3% in December)

- The median CPI forecast for 2019 was also cut to 1.8% (from 1.9% in December)

- The median interest rate forecast for the end of the year is 2.25% to 2.50%, unchanged from current levels. And 11 of the 17 potential voters now anticipate that the central bank will remain on hold until 2020.

- Only one rate hike is expected in 2020, according to the median “dot plot.”

- The central bank will end its balance sheet runoff at the end of September.

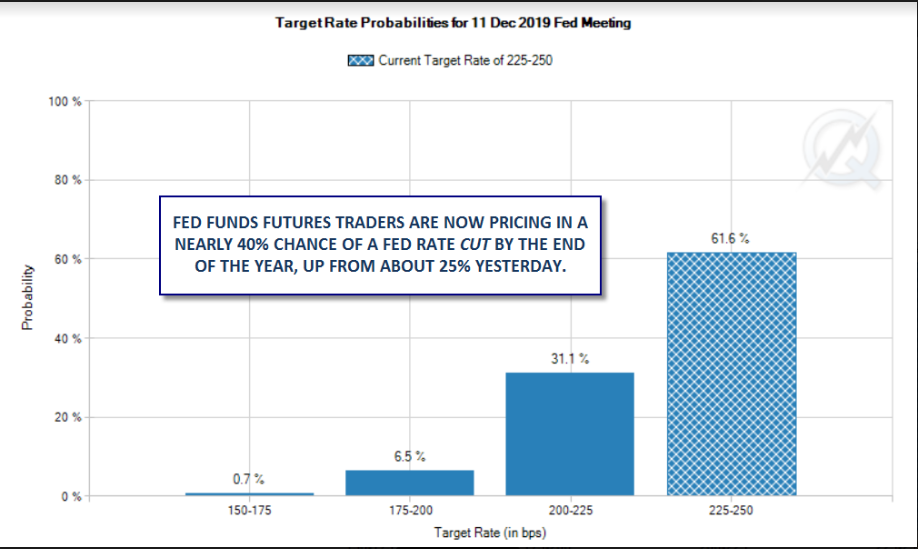

All of these tweaks signal that the central bank is concerned about the U.S. economy and traders have taken notice. According to the CME Group’s FedWatch tool, the market is pricing in nearly a 40% chance of a rate cut this year, up from around 25% prior to the FOMC meeting. Given the scope of the Fed’s negative revisions, we wouldn’t be surprised to see this number rise further in the coming days.

Source: TradingView, FOREX.com

Market Reaction

Not surprisingly, the big shift in the market’s outlook about Fed policy is also being felt in more traditional markets. The U.S. Dollar has fallen by at least 60 pips against all its major rivals, with the U.S. Dollar Index shedding 0.60% as of Wednesday at 3:00 pm CDT. Gold and crude oil have caught a bid on the weakness in the greenback, while major U.S. stock indices have recovered into positive territory on the prospect for lower interest rates in the future.

The biggest move has been in the bond market: The 10-year U.S. Treasury yield is dropping a full 9 basis points on the day to 2.53%; a close here would mark the largest single-day rally in bonds (fall in yields) since last May. Meanwhile, the two-year Treasury note is trading off by 8 basis points to yield just 2.40%.

While we believe that economic data in the coming months may show that the Fed’s dramatic shift is an overreaction, we wouldn’t be surprised to see continued weakness in the dollar, strength in stocks/commodities, and further drops in yields while the market catches up to the central bank’s new posture.