Plenty of warnings signs of a slowing economy, but no definitive top in sight, says Marvin Appel.

The latest data from Europe and the United States revive recession fears, knocking the wind out of a mid-March stock market rally and sending 10-year Treasury note yields to their lowest level (2.42%) in more than a year. Stocks and high yield corporate bonds tanked in response to recession fears during the fourth quarter of 2018, so the question is whether last Friday’s nearly 2% decline in the S&P 500 represents the start of a potential replay. Markets are giving mixed signals.

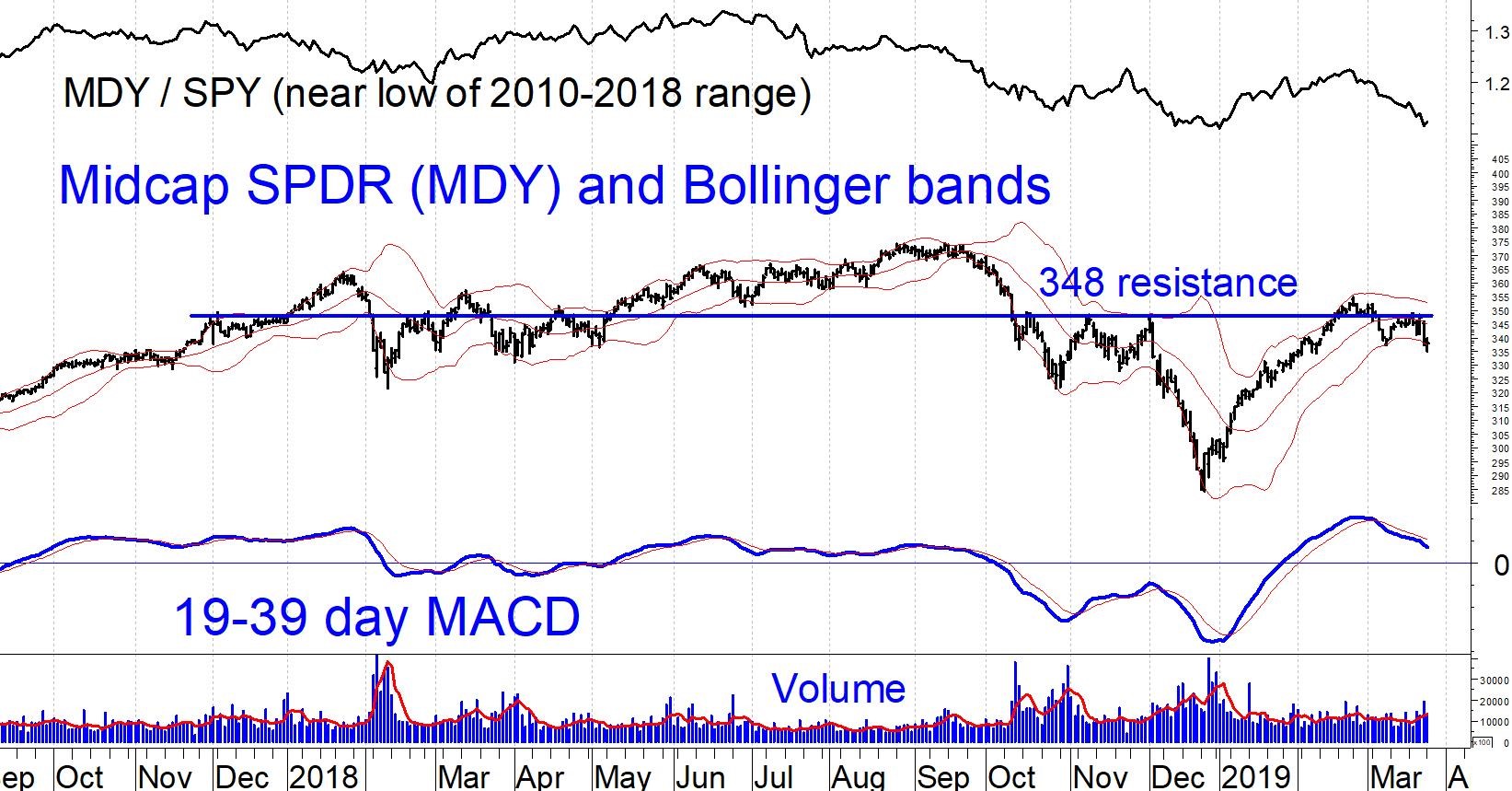

The chart (below) of the SPDR S&P MidCap 400 exchange trade fund (MDY) looks pretty worrisome. Price has formed a falling double top, and the mid-March rally failed around 348, the same level that capped MDY in October and November last year. Unlike the S&P 500 SPDR (SPY), which remains above its 200-day moving average, MDY hasn’t been above that key average in three weeks. MACD is on a sell signal, but since there are no confirmations by negative divergences or multiple signal line crossovers, it is a clear sell signal.

Fortunately, other U.S. indexes are looking better than mid- and small-caps. SPY made a new high as recently as March 21, as did QQQ; both remain above their 200-day moving averages. However, for real reassurance about the impact of recession fears, look to the bond markets.

On the Treasury front, the iShares Treasury Inflation-Protected Securities ETF (TIP) have slightly outperformed nominal Treasury notes, iShares 7-10 Year Treasury Note ETF (IEF) so far this year. If recession fears were acute, IEF would be stronger than TIP as was the case in the fourth quarter of 2018. That said, the drop in Treasury yields (both nominal and TIPS) is a vote of pessimism regarding the U.S. economy. Moreover, the gap between two-year and 10-year Treasury note yields is a mere 13 basis points (0.13%).

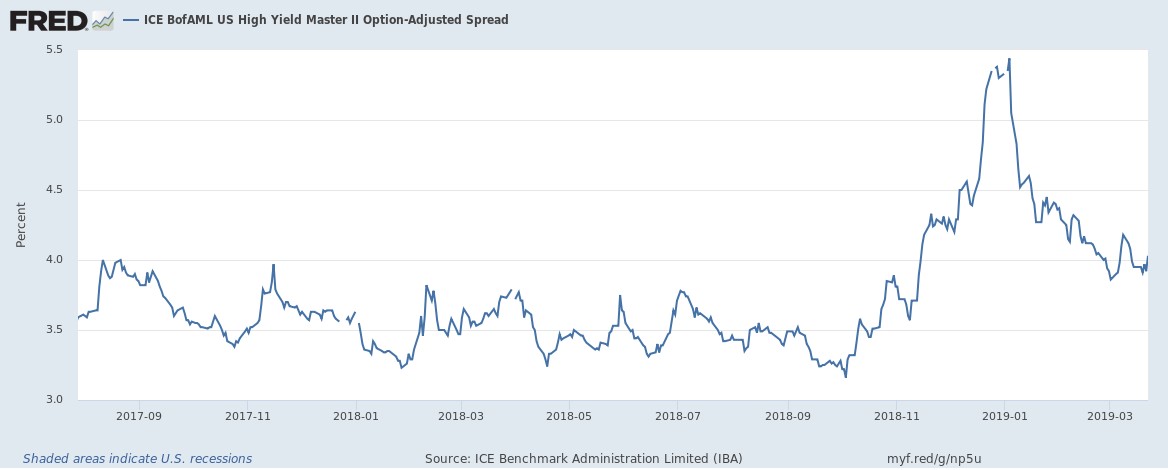

On the corporate high yield front, the yield spread between Treasuries and junk bonds has been stable in the area of 4% for the past two weeks. High yield bond fund prices have also been behaving well, with many making new highs on March 21. However, it is worrisome that floating rate bond funds have been soft, with most at least 25 basis points below their Feb. 28 highs. Floating rate bond funds would be directly hurt by a Fed rate cut, as there would be a parallel decrease in their yields.

We are seeing definite warning signs: weakness in small- and mid-caps, declining long term Treasury yields, a flat yield curve and weakness in corporate floating rate bond funds. However, large-cap U.S. equities and corporate high yield bonds remain steady. My own expectation is that we will see a recession in the U.S. within the next year or two, and that such a recession will be preceded by a stock market correction and a decline in corporate high yield bonds. However, it is too early to call a market top now. I expect to see slow gains in stocks (or an overall sideways market) with continued volatility for months to come. We have positioned our clients with relative caution given that our U.S. and foreign equity models are on buy signals. Take this as a sign that I continue to distrust the stock market.