The bond market is betting the Fed will stave off recessions, reports Marvin Appel.

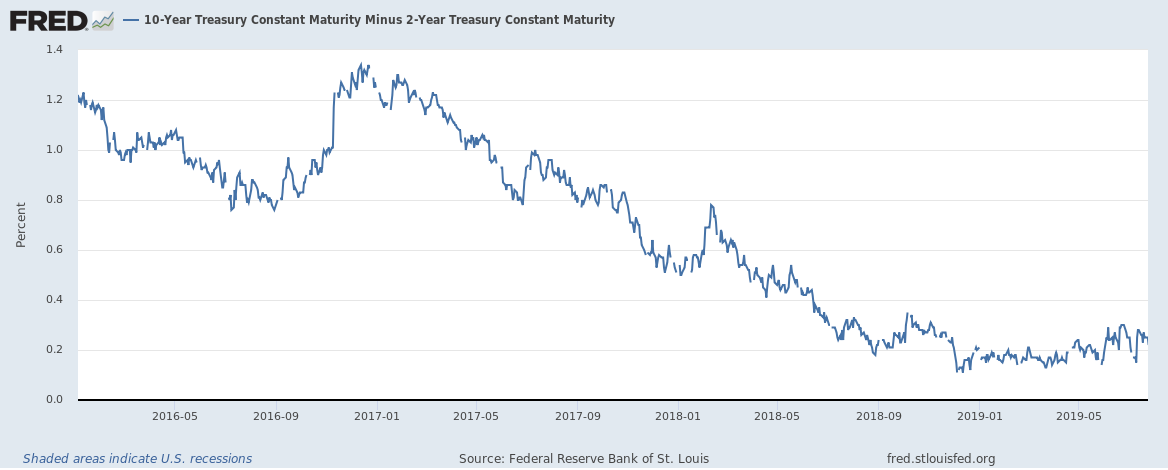

The Federal Reserve is expected to cut short-term interest rates by a quarter point on July 31, and the bond market is signaling wary optimism that the Fed will manage to stave off a recession. First, the difference between 10-year and 2-year Treasury note yields is drifting higher, now at 0.25%. At its low in December 2018, the spread was 0.11%. (See chart below.) Negative spreads in the 2-10 year yield curve have always seen subsequent recessions occur.

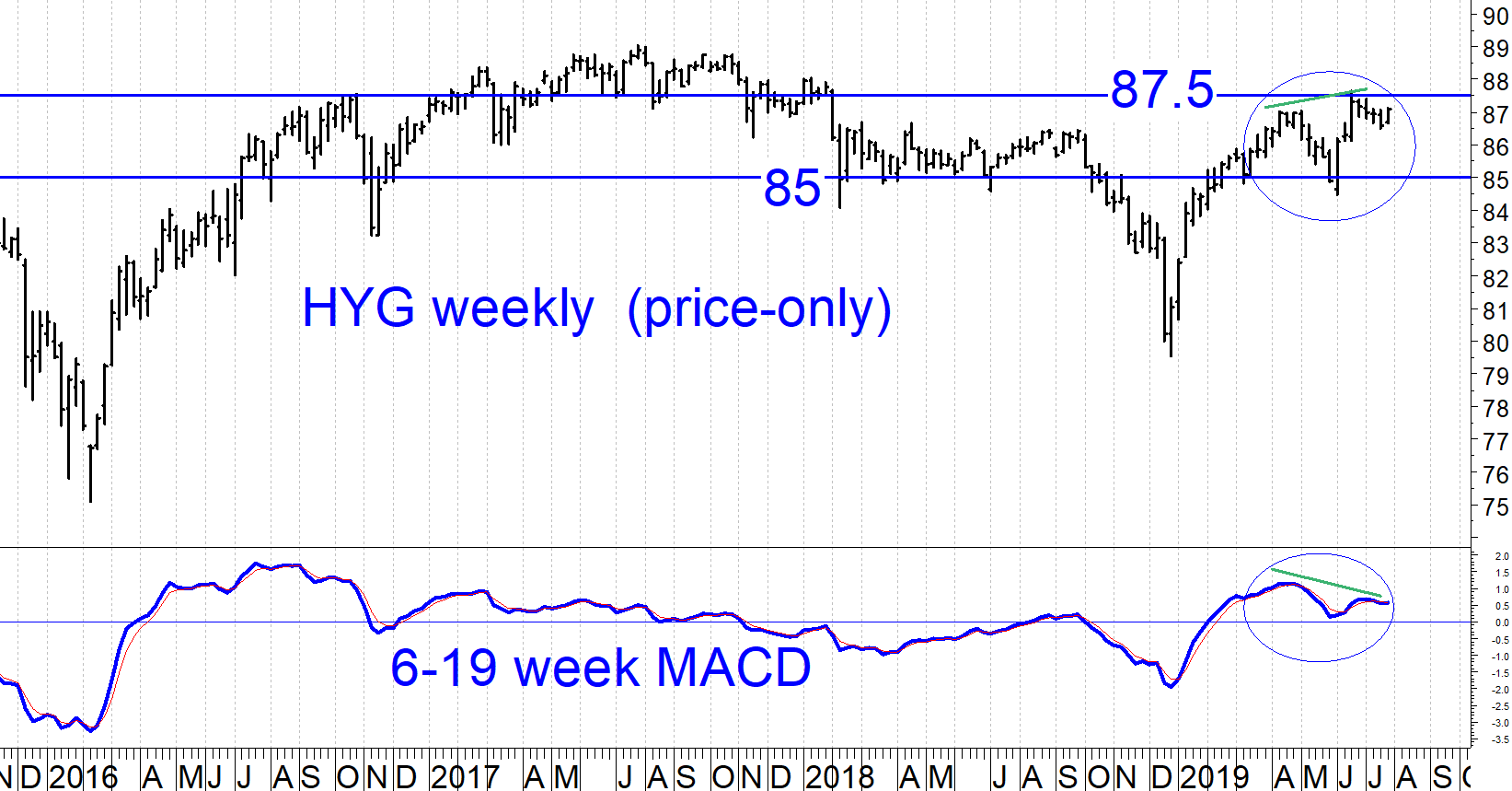

Second, corporate high yield bond funds remain in intermediate-term uptrends. High yield borrowers are relatively fragile and therefore sensitive to any slowdown in the economy. As a result, high yield bond prices can be a good early barometer of changes in the economy. Indeed, high yield bonds peaked four months before stocks in 2007.

However, high bond retracements are a less specific warning sign of recessions than yield curve inversions; There have been many high yield bond corrections without subsequent recessions, such as in 2011, 2015-2016 and the fourth quarter of 2018.

The chart below shows that the iShares corporate high yield bond ETF (HYG) is near the top of its 18-month range. It has formed a negative divergence with its MACD (circled), which could be a warning for the future. However, as long as the six- to 19-week MACD remains above zero, chart patterns notwithstanding, the intermediate-term trend remains favorable.

Thirdly, Treasury Inflation-Protected Securities (TIPS) have stopped lagging relative to nominal Treasury notes. The chart below shows the difference in yield between 10-year TIPS and 10-year Treasury notes, which is the amount of inflation the bond market is predicting for the coming 10 years. In the past month, inflation expectations have risen from 1.61% (the lowest since 2016) to 1.79%. Insofar as deflation and stagnation are the current fears, higher (but still modest) inflation expectations are a good sign.

Lastly, long-term interest rates themselves have stopped falling. The 10-year Treasury note yield has recovered to above 2%.

All of this evidence indicates that the bond market is becoming gradually more optimistic that the economy will avoid triggering a recession. This is in marked contrast to the signals the bond market generated in December, when high yield bond fund prices were falling, and the yield curve inverted. However, yields are still low by historical standards, as are inflation expectations, and the yield curve remains relatively flat. That means that inflation pressures should remain subdued and that economic growth should, unfortunately, be hard to stimulate much beyond the 2.5% level.

In this setting, investment-grade bonds are unlikely to provide attractive returns going forward. High yield bonds (both corporate and municipal) remain my favorite areas of the bond market.

Sign up here for a free three-month subscription to Dr. Marvin Appel’s Systems and Forecasts newsletter, published every other week with hotline access to the most current commentary. No further obligation.