Brexit negotiations are still affecting forex markets, reports Adam Button.

The British pound loses all of its post-elections rally after Prime Minister Boris Johnson said he would not extend the transition period allowed for reaching a trade deal with the EU beyond December 2020 (see chart).

U.S. economic data on Monday was mixed as the market eases back towards evaluating the growth outlook. The euro is again the top performer on Tuesday, with EURUSD rising for the third straight week, something it has done only twice over the last 18 months.

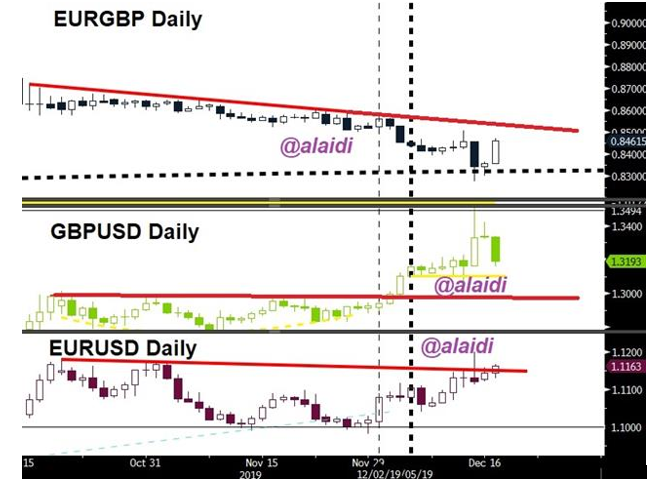

UK employment data was mixed, showing fresh declines in unemployment but weakening wage growth. Ashraf summarizes the EUR-GBP-USD situation in his tweet below. U.S. Industrial production and housing starts/permits are next.

Cliff-edge Headlines are Back?

Johnson's insistence to complete a trade deal by Dec 2020 is viewed by the media as "taking Brexit through Cliffedge", because it implies forcing a Brexit trade deal on WTO terms even if no trade deal is reached within 12 months. This has led to GBP selloff, especially as EU negotiators said it's highly unlikely a Canada-style trade deal could be completed within 12 months. Whether Johnson is using the threat of a hard Brexit to rush through negotiations with the EU remains to be seen.

Global PMIs

The next leg in broad markets will depend on the strength of global growth indications in 2020. It will be weeks before we have a better idea of how strong the economy is but the market is already pricing in at uptick in growth. It's clear now that most data points have stabilize since September but few have turned aggressively upward.

On Monday, the Markit US services PMI was at 52.2 compared to 52.0 expected. That's an improvement from the 50.7 low in October but still well-below 56.0 in February. On the manufacturing side, the index was at 52.6 compared to 52.6 expected. That's flat from the prior month and there was no improvement in new orders.

Along the same lines, the Empire Fed manufacturing index was at +3.5 in November compared to +4.0 expected. It remains squarely in the doldrums.

One spot that's inarguably turning higher is housing. The sensitivity to interest rates in the past two years has been remarkable. The homebuilder’s sentiment survey rose to a 20-year high on Monday at +76 vs +70 expected. In a global sense, U.S. home prices are still relatively low so that sector could be a sustained source of growth, especially with the Fed firmly on the sidelines.

Globally, the picture is also mixed. Markit's eurozone manufacturing PMI deteriorated to 45.9 in December compared to 47.3 expected. That was just a shade above the September low. In contrast, weekend industrial production data from China was a bit stronger than anticipated.

Adam Button is co-owner and managing director of ForexLive.com and a contributor at AshrafLaidi.com. You can see Ashraf’s daily analysis at www.AshrafLaidi.com and sign up for the Premium Insights. Ashraf's Tweet on indices here.