Everything seems to be green across the board so it's time to put on the economist's hat and find bad news. Are stock prices overvalued compared to earnings, asks Ian Murphy of MurphyTrading.com.

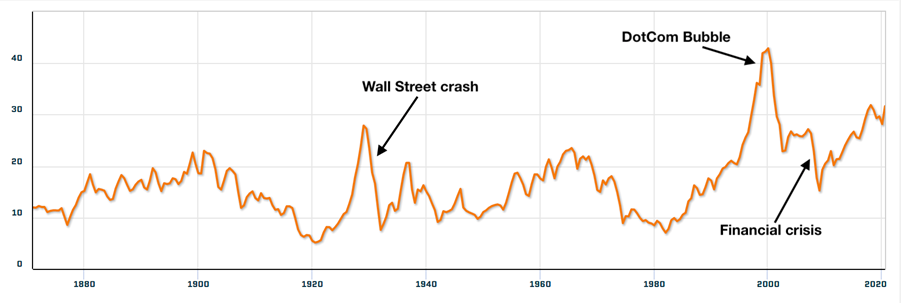

My preferred measure of price-to-earnings (PE) for US stocks is the Cyclically Adjusted PE Ratio (CAPE). Based on average inflation-adjusted earnings from the previous 10 years on the S&P 500 (SPX), it was introduced by Robert Shiller in his 2000 book, Irrational Exuberance.

Source: Quandl

The measure is not without its detractors who cite changes in business models and accounting practices in recent years, plus low interest rates and more mom-and-pop investors, but every PE measure has issues, so CAPE is as good as the next.

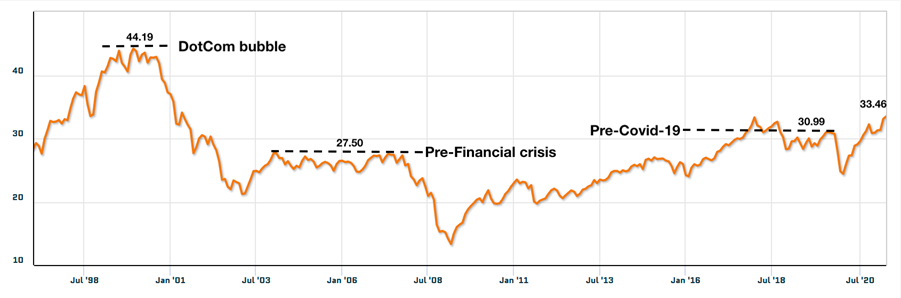

The ratio is currently at 33.46, which is higher than pre-2008 valuations, but 24% below the peak of the dotcom bubble. Assuming little has changed in the way firms do business since this time last year, valuations are looking lofty but there is still plenty of gas in the tank compared to the DotCom days.

Now, let's take off the hat. The previous paragraph was classic economist speak, it tells you what happened in the past, where we are today, and then hedges its bets on the future. It does not tell you when to buy, sell, or stand aside. And that's why traders follow a strategy, it tells you what to do (or not) and when to do it, all the time—PE ratios are just the background music.

Learn more about Ian Murphy at MurphyTrading.com.