Stocks are flirting with 4,200 once again. Gladly it is no longer just large caps and usual tech suspects leading the way, says Steve Reitmeister, editor of Reitmeister Total Return.

Indeed, the rally is broadening out to smaller stocks and growthier stocks and thus seeing a lot more gains piling up in our portfolio.

Also of note is that the odd turn to defensive investing that took place last week because of a rise in coronavirus cases has quickly gone by the wayside.

There were some very short-lived flare ups last week with very little staying power. The first one I previewed above. That being the shift to defensive investing last week as worldwide coronavirus cases spiked to a new high. And yes, there were modest signs of an increase in the States.

This had some investors moving towards a risk-off investing approach with the most conservative names doing well. And the most aggressive names doing the worst. (And many of the names that benefit from the coronavirus fading away also took it on the chin like restaurants, airlines, cruise lines etc.

Gladly, a week later we see signs of improvement on the coronavirus. Especially if we take India out of the equation.

Later in the week we got a scare out of DC with plans of sharply higher capital gains rate for Americans making over $1 million per year. And yes, 80% of the stock market is owned by this very group of investors, which gave grounds for some pause and reflection.

Indeed investors have quickly moved past this as the DC sausage-making process could take a long time with final results being much more benign in the end. In fact, it's quite possible that no tax change ever gets pushed through given what will certainly be heavy opposition.

So this gets us back to viewing the market from more of a traditional standpoint. That being a focus on the fundamentals such as the economy and the results of Q1 earnings season.

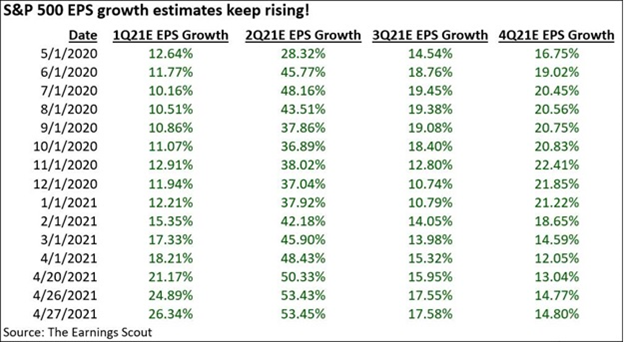

We are now entering the heart of earnings season, yet the early results already tell us we have another strong one on our hands. Below is a copy and paste from Nick Raich who used to be director of research at Zacks when I was there. Now he heads his own shop EarningsScout.com, which has its own beneficial views on earnings trends. Here is what you need to know from this morning’s comments:

In total, 153 companies in the index have now released results classified as 1Q 2021. 88% of those companies have exceeded their EPS estimates, on average, by +17.24%. This a significantly larger-than-normal beat rate. Actual 1Q 2021 vs. 1Q 2020 EPS growth for these 153 companies has been +41.57% with top-line sales rising +6.77%. Excellent results justifying the rally in stocks over the past year.

The main point is that the earnings trend has been rolling higher for quite some time. And since the early earnings reports are so strong, then the growth prospects for the entire market are on the rise. This is very bullish fuel.

Now onto a discussion of the economic data this week, which was also quite bullish. First up being the tremendous 150,000 drop in Jobless Claims last Thursday showing how quickly the economy is healing.

Then on Friday the PMI Markit Flash rose from 59.7 to 62.2 showing broad-based gains in both manufacturing (60.6) and Services (63.1). Sorry for repeating myself so much. But for those who are not aware, anything above 50 is a sign of economic expansion. And above 55 is considered a strong reading. And thus 62.2 is VERY, VERY impressive.

Beyond the strong manufacturing read above we also got two stellar regional manufacturing reports. That started on Monday as the Dallas Fed Manufacturing index climbed from an already impressive 28.9 to a shockingly good 37.3.

Tuesday, we find that the Richmond Fed Manufacturing Index held firm at a solid 17. For these reports anything above 0 is expansionary. And anything about 10 is impressive. So yes...please be impressed by this 17. And uber impressed by the 37.3 for Dallas.

Lastly was yesterday’s announcement that Consumer Confidence exploded higher from 109 to 121.7. This means consumers are downright giddy, which is strong foreshadowing of higher spending activity ahead.

So not only do these economic reports speak highly of the current situation, but the forward-looking aspects look even better. This should give investors pretty good confidence that they should continue expecting this bull market to push even higher.

Reity, does that mean we will be up to 4,500 or 5,000 soon?

Slow your roll buddy 😉

Indeed those are very attainable heights this year given a still-low rate environment that makes stocks so much more attractive to cash and bonds by comparison. Then lop on top the better-than-expected economic/earnings data and you have fertile soil for more stock gains.

However, with as many gains that are already in hand, I suspect the market will be a case of two steps forward and one back. And even at some point we may take two-three steps back in a real correction that wrings out excess allowing the market to progress higher in healthier fashion.

The timing of these events is unknown and unknowable. In general, we should have a bullish posture with a healthy mix of growing companies owned at attractive prices. That indeed is what we have in our possession. More on that part of the story next...

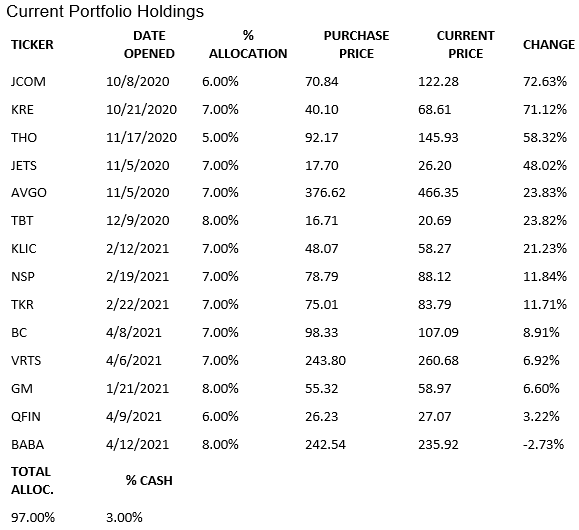

Portfolio Update

We crushed the market in Q1. Almost felt like we were blessed with the Midas Touch.

However, I warned everybody not to get used to comfortable. Meaning Mr. Market won’t allow that to happen for long. Sure enough we saw softer results to start Q2 as the market shifted back to the safety of large caps and most of our growthier positions languished.

Instead of shifting gears I knew it was right to stay put. That like a boomerang the market would come back in our direction. That certainly has been true the past week where we have produced a +4.59% return well ahead of the +1.25% of the S&P.

And now as we go back to the start of the year, we find that even with the early April lull we are still handily in the lead year-to-date at +25.83% vs. +11.47%.

No, it’s not 4 or 5X better than the market like it once was. That victory margin was never built to last. But certainly no shame in our game at this time and would happily take this lead over the market every year.

Now on with our look at the individual picks in the portfolio.

Earnings Season Comes to Life for RTR: Before our next commentary we have this slate of earnings reports coming out.

4/28 TKR & VRTS

4/29 BC

5/3 NSP

And not far behind is GM & KLIC on 5/5, then JCOM on 5/10 and QFIN on 5/24 (some of these are tentative dates).

So let’s have our traditional quarterly earnings conversation. If this were a road it would be a mountain road with some breath-taking views. But there would also be signs to watch out for all the twists and turns. And yes, the chance of falling rocks.

There is no getting around it. Earnings season comes with risk.

Gladly, the focus on the POWR Ratings, where it looks for consistency of growth and quality of strong operational results, greatly increases the odds that our companies will perform well during this trying time. So, you should expect the majority of our firms to do quite well and rise after their results.

Unfortunately we likely still have three-four that will need to be expunged from our portfolio for lackluster performance. That is fine as long as the rest end up in the winners column pressing out entire portfolio higher.

This healthy perspective will help you ride out the highs and lows of earnings season in the best possible fashion.

Brunswick (BC): Bit by bit analysts are coming out of the woodwork to talk up BC to investors. Last week it was the analyst from Jeffries labeled it a Buy with a $120 target. And today we get an upgrade from the analyst at Citigroup to a Buy with new street high target of $125. This has put a little fire under shares into their 4/29 announcement. Typically, this much analyst praise before earnings is strong foreshadowing of what lies ahead. If true, then we could easily be talking about $130+ price targets and plenty of reason to stay behind this powerboat company skiing our way to more profitable shores.

Insperity (NSP): Shares are quietly climbing higher once again. Certainly, the positive news from Thursday’s jobless claims is a plus for them given the correlation between more employed people at their companies and the fees they collect. Next Monday we will know for sure where they stand. Hopefully more evidence of growth giving shares a fighting chance to make it to $100 before the Q2 earnings report.

Kulicke & Soffa (KLIC): KLIC is getting some serious analyst attention. On back-to-back days got target price raises of $75 and $83 respectively. Yes, that is WAY ABOVE the current price, which explains why shares have been sprinting higher of late. Likely see a spot of resistance here at $60 after a nearly 50% rise in the past several weeks. Yet it seems there is a good reason that analysts are pounding the table on shares now with only a couple weeks to go before the announce earnings. Let’s hope this foreshadowing turns out to be true.

Note that we already have two semiconductor stocks in our portfolio when you add AVGO to the party. That is a pretty hefty allocation. However, Micron (MU) keeps popping up in my research as another great industry pick. If you want the roll the dice on this positive environment for semiconductors, then do consider MU as another quality choice.

360 Finance (QFIN): Our most volatile position is certainly living up to the billing of late. Yet easy to laugh off today’s losses given how quickly it rallied 25% over the previous two weeks. Put both hands on the reins of these shares so as not to be thrown off to easily. If so, it should end up a very enjoyable ride.

Alibaba (BABA): This giant is starting to wake up from its slumber. Don’t be surprised if it's in the upper $200’s by mid-year with $300 my target by year end.

Shorting Treasury Bonds (TBT): After wonderfully timing the breakout of Treasury rates above 1% it was a non-stop party in TBT shares. But after rates got to 1.76% a month ago, they took an extended round of profit-taking back down to about 1.5%. With that move we saw a little of the TBT gains get washed away.

Now the tide is coming back in. Rates are on the move again ending today over 1.6% helping TBT have a pretty solid session. Again, I will go on record saying that I will be shocked if rates don’t make it to 2% in the not-too-distant future as the economy heats up. And 2.5 to 3% is a likely range to end the year. If true, then there are a lot more profits to enjoy from TBT as the year progresses.

Timken (TKR): Shares are putting in some nice distance from the brief dalliance below $80. Now we are coming into their next earnings report before the market opens on 4/28. If I am being honest, this is a company that runs hot and cold during earnings season. Meaning you never know what you are going to get. The risk is evident in that picture. The reward is that others know this about TKR and if they have a strong result (which they should, given the strength of most manufacturing and industrial economic reports) then shares should start sprinting above $90 on their way to $100 over the next few months. Fingers crossed!

Virtus Investment Partners (VRTS): Also reports earnings 4/28 in the AM. Gladly VRTS has a more consistent history of earnings beats. In fact, they have a streak of 10 such strong reports in a row. In this case, the main ingredient in higher revenue and profit is the growth of assets for which a strong Q1 for equities virtually assures that outcome. So here I have less doubt of solid results. The bigger question is how long it will take for VRTS to make it closer to their average target price of $325. Or better yet the street high of $365. I look forward to watching it happen.

Learn more about Steve Reitmeister at StockNews.com