When it comes to Federal Reserve interest rate cuts, it helps to remember the old saying: “Be careful what you wish for!”

Right now, the Trump Administration is clamoring for big rate cuts – and soon. Wall Street is looking for somewhat more moderate rate cuts to begin before long, too. But SHORT-TERM rate cuts don’t always deliver LONG-TERM yield relief. In some cases, you get the exact OPPOSITE.

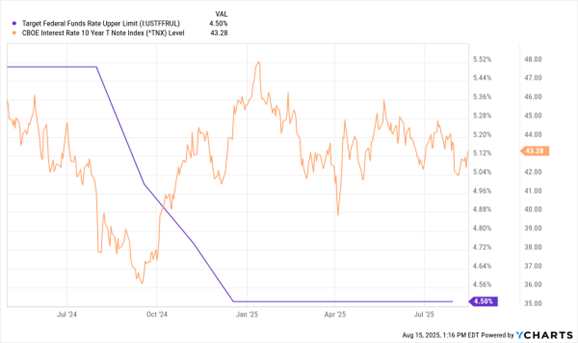

Take a look at the MoneyShow Chart of the Day. It shows the upper limit of the federal funds rate target range in blue – and the CBOE 10-Year T-Note Index (^TNX) in orange – from May 2024 through present day. The TNX index is simply the 10-year Treasury Note yield times 10, so 43.28 = a yield of 4.328%.

Fed Funds Rate Upper Limit, 10-Year Treasury Note Index

(May 2024 - Present)

Data by YCharts

What do you notice here? The Fed slashed the federal funds rate target range by a more-aggressive-than-usual 50 basis points at its September 2024 meeting. It then cut it twice more by another 25 bps, once in November and once in December.

What happened to long-term yields in response? They SOARED! TNX shot up from around 36 to 48 in just a couple of months. Oops.

More recently, all the chatter about deeper, earlier Fed cuts isn’t helping long-term yields. If anything, it’s HURTING at the extreme end of the yield curve. Case in point: The yield on the 30-year Treasury Bond was hovering around 4.93% on Friday, UP from 4.79% at the start of 2025.

WHY can that happen? Because the Fed only directly controls very short-term rates. Long-term yields rise and fall based on market perceptions of future economic growth, inflation risk, policy risk, currency risk (when it comes to foreign debt holders), and more. If bond investors think Fed cuts NOW will boost those risks LATER, they’ll sell bonds and yields will rise.

Stated another way: All the pressure on the Fed to cut, cut, cut could HURT bondholders and borrowers, not help them. So, yeah. Be careful what you wish for!