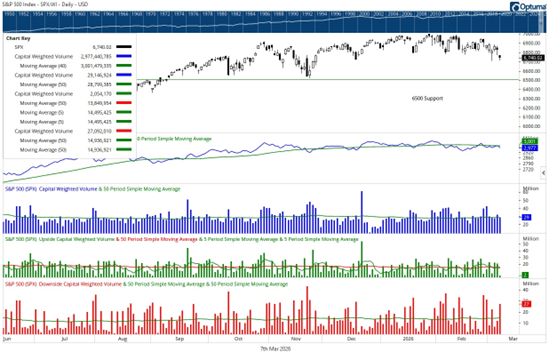

Markets entered last week under a cloud of geopolitical uncertainty as open conflict between Iran and Western allies injected a sudden fog of war into global markets. The initial reaction was swift. Despite the widespread pullback, markets largely held their intermediate defensive lines, writes Buff Dormeier, chief technical analyst at Kingsview Partners.

The week produced two decisive downside engagements. Tuesday, March 2 registered an 80% downside day on average volume. Friday escalated further with a 93% downside day, again on average volume.

S&P 500 Index (^SPX)

Despite the severity of the headlines and the sharp decline in price, the volume data tells a more measured story. For the full week, Capital Weighted Volume finished essentially balanced with 51% to the downside versus 49% to the upside on average total volume.

Capital flows, measured through Capital Weighted Dollar Volume, leaned slightly more defensive, with outflows accounting for 53% versus 47% inflows on modestly elevated weekly activity. In other words, while price retreated sharply, the battlefield statistics do not yet suggest wholesale liquidation.

From a technical perspective, the broader formations remain within their upward intermediate trends even as the short-term battlefield has grown more volatile. The market may be distributing shares under stress, but it is not yet showing the type of aggressive liquidation that historically accompanies major trend reversals.

In times of geopolitical conflict, markets often trade on emotion before returning to structure. Investors should monitor whether downside volume begins to expand meaningfully beyond the current equilibrium. Sustained downside participation would signal that distribution is gaining control of the field.

Conversely, if support levels continue to hold while breadth stabilizes, the broader trend may ultimately withstand the current fog of war. For now, discipline remains paramount. The battlefield has grown more uncertain, but the larger market campaign has not yet been decided.