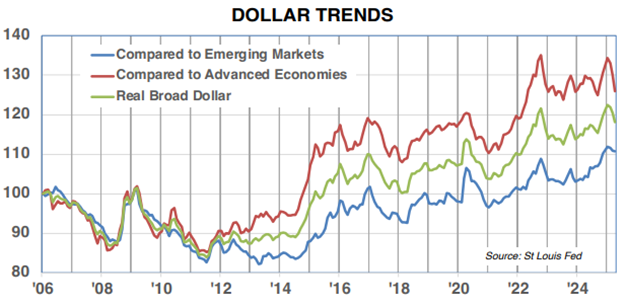

The dollar, the world’s dominant currency, has been in hot demand since the start of the pandemic. But that trend has started to unwind a bit in 2025. Year-to-date, the dollar has given back 3% against a worldwide trade-weighted index and 5% compared to an index of advanced economy currencies, notes John Eade, president of Argus Research.

Some of the slide can be linked to the economic uncertainty caused by President Trump’s trade and tariff policies, though reasons also include the swelling US federal debt, which is not a new trend. Sovereign wealth funds are rethinking their commitment to US assets as the cost of doing business in America increases and the balance sheet strains.

But we would hesitate to term the dollar at risk of losing its status as the global currency of choice. Even with the pullback this year, the dollar is 18% above its 20-year average value. The greenback is supported by the depth of a $27 trillion market, not to mention by the Federal Reserve and by the country’s time-tested political/economic system of democratic capitalism.

The alternatives (the euro, yen, or yuan) have their issues as well. For several reasons, we anticipate a relatively stable trading range for the dollar over the balance of the year.

For one, the dollar typically tracks GDP growth trends, and we think the US economic expansion is poised to ease in coming quarters as jobs growth slows. For another, the still-elevated valuation of the greenback implies that other currencies – and even gold or other commodities – are possibly undervalued. We would expect investors to bid up those values at a measured pace over time.