Where do markets go from here? That depends on the headlines. Meanwhile, Oracle Corp. (ORCL) just beat both top- and bottom-line estimates for Q4, observes Keith Fitz-Gerald, editor of 5 With Fitz.

Anything that reintroduces FUD – fear, uncertainty and doubt – has the potential to be a downer. Anything that inspires confidence can create FOMO if there’s a sense that worries like tariffs, rates, and the economy can be relegated to the back seat, so to speak.

My POV is that we’ll see range bound conditions for a bit with an upside bias lurking under the hood as Wall Street tries to hide that from the investing public.

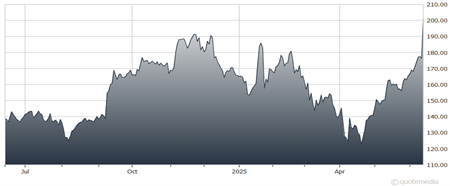

Oracle Corp. (ORCL)

As for ORCL…

- Revenue came in at $15.9 billion, an 11% increase year-over-year.

- Cloud services and support revenues jumped 14% YOY, reaching $11.7 billion.

- Cloud infrastructure (IaaS) revenue surged 52% to $3 billion, while SaaS-based cloud applications revenue grew 12% to $3.7 billion.

The company is expecting an even better 2026, with CEO Safra Catz forecasting that total cloud revenue growth will accelerate from 24% in FY25 to over 40% in FY26. Oracle Cloud Infrastructure (OCI) growth alone is projected to top 70%.

Hooyah!

I think there’s a very good chance that cloud revenue could accelerate even faster than Catz suggests, though. There’s already more than $1.5 trillion flowing into AI and the advanced manufacturing needed to make it all work.

Which means that Oracle could be a very interesting choice…a “sleeper” to paraphrase my grandfather, who would often refer to under-recognized baseball players having the potential to significantly outperform expectations.