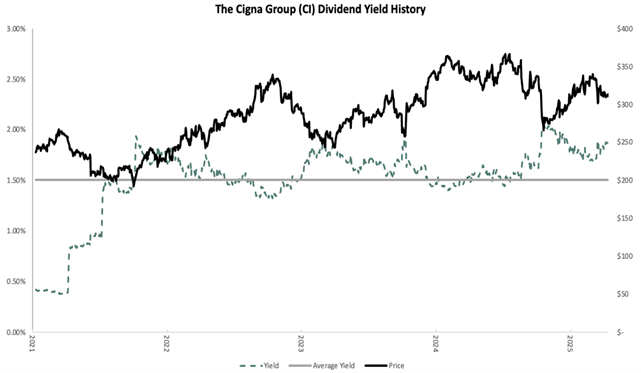

The Cigna Group (CI) is a leading provider of insurance products and services, including dental, medical, disability, and life insurance. Cigna has grown its earnings per share at an average annual rate of 12.2% over the last decade and at an 8.2% average annual rate over the last five years, highlights Ben Reynolds, editor of Sure Dividend.

The company operates in four business segments: Evernorth, which provides pharmacy services and benefit management; US Medical, which provides commercial and government health insurance; International Markets; and Group Disability. Evernorth contributes about 80% of annual revenue while Cigna Healthcare accounts for much of the rest. Cigna has annual revenue of approximately $250 billion.

On May 2, Cigna posted its Q1 results. Revenue grew 14.2% to $65.4 billion, which was a notable $5.1 billion ahead of estimates. Adjusted EPS of $6.74 compared favorably to adjusted EPS of $6.47 in the prior year, and was $0.39 better than expected.

Customer count was flat at 182.2 million over last year, but down from 186.8 million in Q4. Pharmacy customers fell 0.4% to 118.3 million, while medical customers fell 6%. Further, Evernorth’s revenue rose 16% to $53.7 billion, while Cigna Healthcare grew 9% to $14.5 billion on premium hikes.

Cigna raised its 2025 adjusted EPS guidance to at least $29.60, up slightly from $29.50. However, we remain cautious of this forecast due to President Trump’s May 12 executive order targeting pharmacy benefit managers (PBMs) like Cigna’s Express Scripts. The policy could pressure PBM revenue and margins, potentially leading to a guidance revision in the next earnings release.