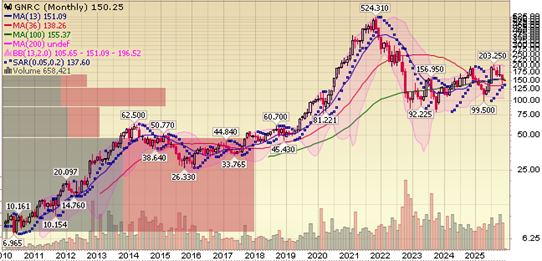

Generac Holdings Inc. (GNRC) delivered a softer-than-expected third quarter, with revenue of $1.11 billion, down 5% year-over-year and missing estimates by about $79 million. On the surface the numbers look ugly, but the story is far less dramatic than the headlines suggest, writes Tom Hayes, editor of HedgeFundTips.

Adjusted earnings per share were $1.83, down 19% YOY and missing by $0.37. The miss forced management to lower full-year guidance. Net sales are now expected flat YOY (previously plus-2% to 5%) and adjusted EBITDA margins are tracking to about 17% (previously 18%-19%).

But the entire shortfall was driven by an unusually quiet hurricane season that weighed heavily on Generac’s highest-margin, bread-and-butter Home Standby business. While great weather is a win for almost everyone, when your core product only sells when the lights go out, sunshine can be a gut punch to demand.

Generac Holdings Inc. (GNRC)

Q3 delivered the lowest outage hours since 2015, running 75%-80% below the long-term average, all against a tough comp from last year’s three major storms and the highest outage quarter since 2012. Tough setup…zero help from Mother Nature…entirely predictable outcome.

Zoom out and this “weak” quarter is pure noise. We didn’t buy Generac to play the weather-prediction business. We bought a high-quality secular compounder with 75%-plus share in a market where US household penetration is still only around 6.5%. Every additional point of penetration is a $4 billion opportunity waiting to be captured.

Until that math changes, we’re happy to hold the “Kleenex of generators” and leave the weather forecasting to someone else.