It’s easy for income investors to be attracted to Ellington Financial Inc. (EFC) and its big 13% yield. Even better, the company pays dividends monthly. But Ellington is a serial dividend cutter, cautions Marc Lichtenfeld, chief income strategist at Wealthy Retirement.

Ellington is a mortgage Real Estate Investment Trust, or REIT, that has been around for more than 30 years. It invests in both commercial and consumer mortgages in underserved markets. One of its founders, Mike Vranos, who’s currently the co-chief investment officer, was at one time considered the best-known mortgage-bond trader on Wall Street.

Mortgage REITs borrow money short-term and lend it out longer-term. The money they make is called net interest income (NII).

The good news is Ellington’s net interest income is moving in the right direction. In 2025, the company generated $190 million in NII, up 39% from the year before. NII is forecast to grow another 5% to $200 million this year and continue higher over the next couple of years.

Ellington paid shareholders $184 million in dividends in 2025, or 97% of its NII. Mortgage REITs have to pay out 90% or more of their profits by law, so I’m fine with any payout ratio that is below 100%. The payout ratio is forecast to rise to 98% in 2026.

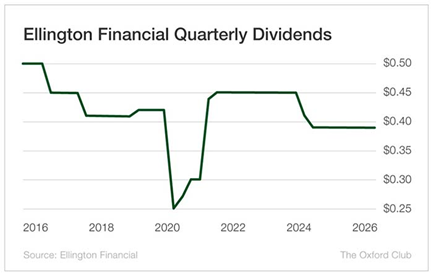

Here’s where there’s a problem: There have been four dividend reductions in the past 10 years – five if you group the payouts on a quarterly basis. In other words, when the going gets tough, Ellington shareholders receive lower dividends. The most recent cut came in March 2024 – from $0.15 per month to $0.13.

If Ellington Financial is able to continue to grow NII as Wall Street expects, the dividend should be fine. But if there is any downturn, management has shown it is very willing to reduce the payout to shareholders.