Investors are being forced to play a waiting game since the war isn’t over, Q1 earnings reporting season doesn’t (unofficially) start until April 14, and the next Federal Reserve policy meeting won’t occur until the end of April. Not surprisingly, investors are now wondering if they should buy, bail, or just bide their time, observes Sam Stovall, chief investment strategist at CFRA Research.

All sizes, styles, and ten of 11 sectors have fallen in price recently, along with 91% of the 155 sub-industries in the S&P 1,500. Despite the thickening fog of war and adverse potential impact from a prolonged spike in oil prices, investors may benefit in the long run by taking advantage of groups that now trade at attractive discounts to their 10-year average.

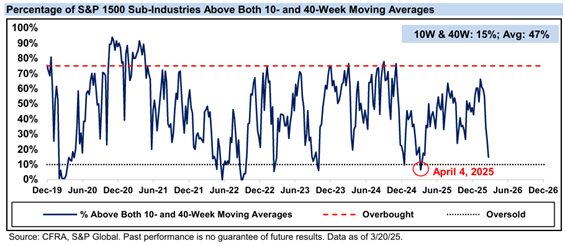

Meanwhile, last week saw a further slide in the week-ending percentages of the S&P 1,500 sub-industries trading above their 10- and 40-week moving averages, as well as above both averages. All three readings are now well below their long-term averages, and the reading for both has fallen to 15% from 66%.

Even though the percentage of S&P 1,500 sub-industries currently trading above both moving averages has slipped swiftly in the past month, it has not fallen below the 10% level, which typically indicates that the market is beginning to get washed out.

A reading of 5% or below implies that investors have thrown the baby out with the bath water. This percentage fell to 1% on April 4, 2025, a few days before the eventual bottom of the minus-19% “Liberation-Day” correction.