This “mistrusted” bull market may end up confounding investors further as history suggests the S&P 500 Index (^SPX) could still post a double-digit gain for the full year, writes Sam Stovall, chief investment strategist at CFRA Research.

Through May 22, the S&P 500 had already recorded 18 new all-time highs in 2026. That matches the tally for the S&P SmallCap 600 and exceeds the totals for the Nasdaq-100, S&P MidCap 400, and Dow Jones Industrial Average. Since World War II, this year’s pace ranks as the sixteenth strongest through May.

(Editor’s Note: Sam will be speaking at the Investing in Alternatives Virtual Expo, scheduled for July 8-9, 2026. Click HERE to register.)

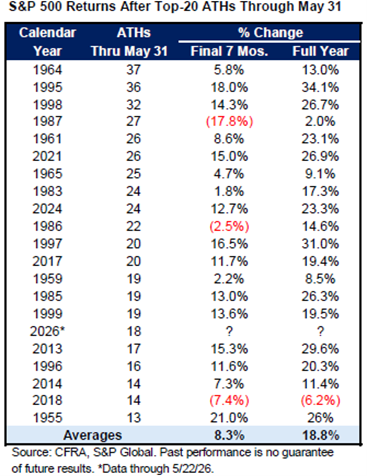

History suggests (but does not guarantee) those gains could lead to further upside. The top 20 years for new highs through May produced average full-year gains of 18.8%, with only one decline occurring in 2018 during a Federal Reserve tightening cycle. In addition, 17 of those years posted further gains averaging more than 8% during the final seven months of the year.

Several headwinds could still disrupt the rally, including higher oil prices feeding inflation pressures, rising bond yields, and the possibility that the Fed’s next move could eventually be another rate hike. However, with this Teflon market having already sidestepped many potential “potholes” that could have reversed its upward trajectory, this bull appears to have further to run.

Besides the broad benchmarks reaching multiple new highs, the S&P 500 energy, industrials, and materials sectors also accumulated admirable results. Only the real estate sector was left empty-handed.

Furthermore, even though only 41% of the 126 subindustries in the S&P 500 recorded new highs this year, construction and engineering, integrated oil and gas, and semiconductor equipment and materials posted impressive counts.