There were two big lessons from the TMT bubble of the 1990s. First, waiting to worry about earnings until after the infrastructure is built is a mistake. Second, even though the race to build networks was the focus on the mania in the ‘90s, it was the businesses built on those networks which captured all the value, writes Eoin Treacy, editor of Fuller Treacy Money.

The AI companies have largely avoided that issue in this cycle. They are prioritizing revenues even as they spend oodles of cash on expansion.

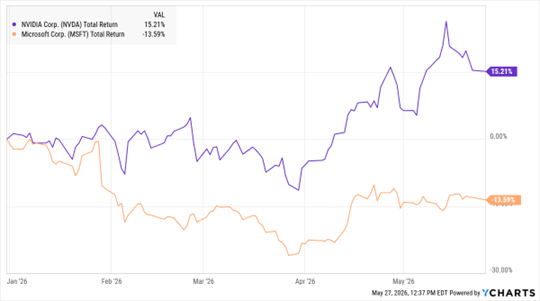

NVDA, MSFT (YTD % Change)

Data by YCharts

When I see a company like Nvidia Corp. (NVDA) or Microsoft Corp. (MSFT) put cash into startups, they are investing on the potential gains to be developed from building the compute capacity. These are akin to options strategies. They may work out and they may not.

The last challenge is that no two companies deploy the same depreciation schedule on their chips. That either means they do not know how long they will remain useful, the loads are calculated differently, or the answer is very inconvenient.

The other significant difference between now and the ‘90s is that computing capacity demand is still ahead of supply. AI labs are struggling to keep up, so it would be difficult to make the argument that they are overbuilding at present.

Bottom line: No two bull markets are identical. The primary risks in the AI buildout are the persistence of revenue growth, efficiency gains in AI, and the longevity of the chips.