The S&P 500 and Nasdaq Composite Index rose to fresh record highs on Friday, and stocks are trying to add to those gains in the early going today. Crude oil, gold, and silver are losing some ground along with Treasuries. The dollar is largely unchanged.

The latest jobs data helped add to bullish sentiment. The economy created a greater-than-expected 206,000 jobs in June, but the previously released numbers for April and May were revised down by 111,000. Unemployment also rose slightly to 4.1%, while average hourly earnings climbed just 3.9% from a year earlier – the smallest gain in three years.

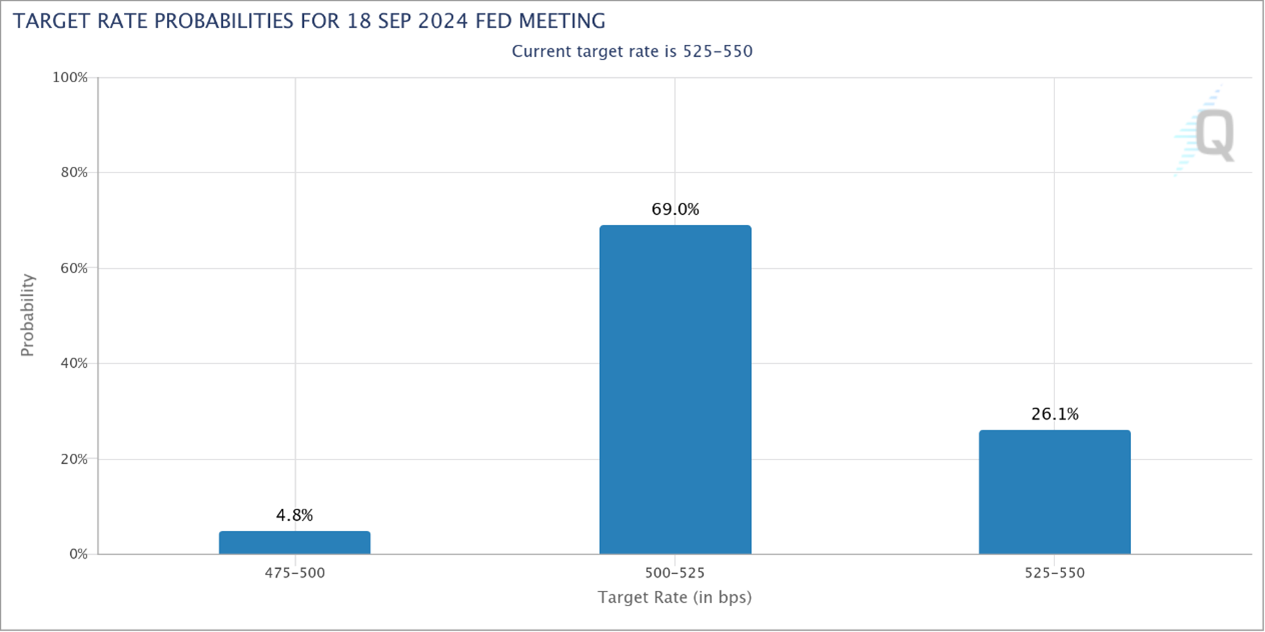

September Rate Cut Chances Rising on Cooler Jobs Data

Along with other recent reports, Friday’s one suggests the economy is cooling without collapsing. That is reducing inflationary pressure – and opening the door to Federal Reserve interest rate cuts later this year. Rate futures markets are now pegging the chances of an initial 25 basis point cut in September at around 69%, up from just 47% a month earlier.

Q2 earnings season will kick off Friday, with “Big Finance” names like JPMorgan Chase & Co. (JPM), Wells Fargo & Co. (WFC), and Citigroup Inc. (C) all reporting their latest numbers. Earlier in the week, we’ll also get key inflation data in the form of the Consumer Price Index. Plus, Fed Chairman Jay Powell will testify on the state of the economy before Congress Tuesday and Wednesday.

In a surprise result, France’s right-leaning National Rally party under Marine Le Pen plunged to third place in follow-up parliamentary elections, winning only 142 seats. The left-leaning alliance New Popular Front ended up winning the most seats at 178, while centrist President Emmanuel Macron’s coalition took second at 150.

Since no individual party or coalition won a clear majority, the nation will be operating with a hung parliament for a while. But French markets held their recent rebound because Le Pen’s party didn’t secure a win.