Stocks popped in early trading after key economic data was released. Gold and silver are mixed, oil is up, and Treasuries and the dollar are flattish.

Today’s Consumer Price Index report was the last major potential obstacle to a Federal Reserve interest rate cut next Wednesday. Economists expected both the headline and core CPI to rise 0.3% in November. And both the headline and core CPI rose...0.3%. That was good for year-over-year inflation rates of 2.7% and 3.3%, respectively.

Since we didn’t get any surprises, the Fed will almost certainly cut rates by another 25 basis points to a range of 4.25% - 4.5%. After that meeting, the Fed has early-2025 gatherings Jan. 28-29 and March 18-19. Markets currently expect the Fed to skip a cut at one of those meetings to see how past moves filter through the economy. But incoming data could change that outlook.

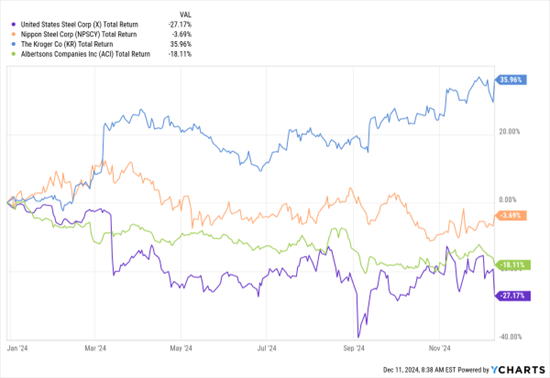

X, NPSCY, KR, ACI (YTD % Change)

Data by YCharts

The government and the courts appear to be getting in the way of two potential mergers as the year winds down. Shares of US Steel Corp. (X) tanked yesterday after reports the Biden Administration would move to block the company’s acquisition by Japan’s Nippon Steel Corp. (NPSCY). The $15 billion bid is currently being reviewed by the CFIUS committee that examines all foreign purchases of US companies for national security risks.

Meanwhile, an Oregon court sided with the Federal Trade Commission (FTC) in its lawsuit against the $25 billion merger of Kroger Co. (KR) and Albertsons Cos. (ACI). The FTC successfully sued to stop the deal, arguing it would reduce competition in the grocery industry and drive consumer prices higher. While the companies can technically appeal, their attorneys suggested earlier that the companies would call the transaction off if they lost.