Matthew Kerkhoff, options expert and editor of Dow Theory Letters, continues his 14-part educational series on understanding options and their role in investment portfolios. This series will run each Friday on MoneyShow.com through December, moving from the basics through increasingly more sophisticated strategies.

The goal of this series is to provide a basic overview on how options can be used to help protect and manage a portfolio.

Part 1 introduced calls and puts, and discussed some of the vocabulary associated with using options. Part 2 focused exclusively on call options, and included examples of buying and selling a call option. If you missed last week's article, consider reading Part 1 and 2 first to get caught up.

To read Part 1 and 2 click here

Today we’re going to focus on understanding put options in more detail, including examples of buying and selling a put.

In order to get your brain primed and ready to go, recall that:

A call option is the option to buy an asset at an agreed upon price on or before a particular date.

A put option is the option to sell an asset at an agreed upon price on or before a particular date.

Also recall that the “agreed upon price” is called the strike price, and the “particular date” in question is called the expiration date. Finally, remember our important rule of thumb: Option buyers have rights; options sellers have obligations.

Okay, let’s get started.

Buying Puts

When it comes to options, calls are all about the upside, and puts are all about the downside. If you recall from the last article, which focused on call options, we were either buying or selling the upside potential on an underlying security.

With puts, as we’re about to see, that’s all reversed. This time, whether we’re buyers or sellers of puts, the focus is going to be on the downside – either capitalizing on it as a buyer of put options, or accepting the risk of it in exchange for collecting premium, as a seller of put options.

FREE 14-part guide to options: The Basics to In-Depth Portfolio Strategies

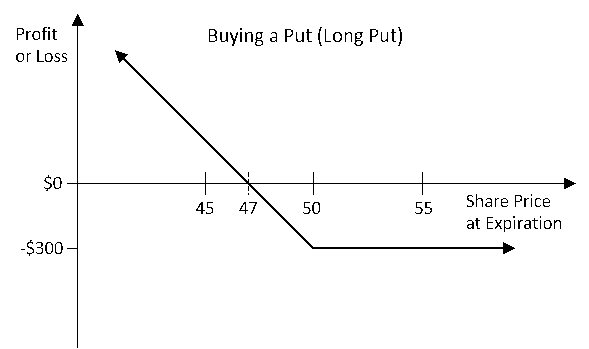

In this first example, we’re going to look at the profit and loss scenario that arises from buying a put option.

Suppose that ABC stock is trading at $50/share, and that we believe the share price may head lower in the near future. If we want to set ourselves up to profit from the downward move, what’s our best course of action?

In this situation, one way we could profit from the decline would be to sell short actual shares of ABC stock. But the problem with going that route is that it would leave us in an unlimited risk position. If we got it wrong, and ABC moved higher instead of lower, we could lose a fortune.

So what’s the better alternative? Buying a put option, of course. As you’ll see, this will allow us to profit from a downward move in ABC stock, but it will also (and this is the important part) create a situation in which our maximum potential loss is both limited, and known.

Since this is much more advantageous, let’s say we go this route and purchase a put option priced at $3, that has a strike price of $50. The chart below shows the payoff scenario from buying that put option.

The first thing to note is that this put option will cost us $300 (recall that one option contract represents 100 shares, and the put option’s price of $3 is on a per share basis).

In exchange for our $300, we have purchased the right (recall our rule of thumb) to sell 100 shares of ABC, on or before expiration, for $50 per share.

As mentioned above, what’s especially nice about buying a put option, as opposed to shorting a stock, is that our maximum loss is limited to the cost of the option we purchased. Notice in the chart above that if we do get the trade wrong, and ABC moves higher, the most we can lose is our $300.

This is because as option buyers we have rights, if we choose to exercise them, but we are under no obligation to do so. Therefore, while we could sell 100 shares for $50 per share to the seller of our put option, we’d have no reason to do so if we could sell those same shares for more in the marketplace. In this case, the put option we purchased would expire worthless, and we’d simply be out the initial $300 that we paid.

Next, it’s important that we determine our breakeven share price for this trade, which is $47 per share. Here’s how that works.

Our put option allows us to sell 100 shares of ABC stock at $50 per share. In order for us to recoup the initial $300 cost of the option, we need to be able to generate $300 in profit from this trade.

For that to happen, we would need shares of ABC to trade down to $47 per share, at which point we could buy 100 shares, which we would then resell (per our option contract) for $50 per share. The net gain of $3 per share would balance out the $3 per share cost of the option contract.

If we’re correct and ABC shares do lose value, then everything beyond $47 becomes profit. For the sake of the example, let’s say shares of ABC are trading at $44 per share at expiration. In this case, we would be able to purchase 100 shares in the market at $44, then sell them per the terms of our option contract for $50 per share.

The result would be a net revenue of $6 per share on 100 shares ($600). Since the put option initially cost us $300, we have a profit of $300, or 100%. And of course the lower ABC stock trades before expiration, the larger our profit is.

To summarize, here’s what we need to remember about buying put options.

* It’s a strategy to use when we are bearish on a stock or ETF

* The downside potential is limited (to the price or “premium” that we paid)

* There is limited upside potential (the most the stock can fall is to zero, which would represent the maximum profit from this trade).

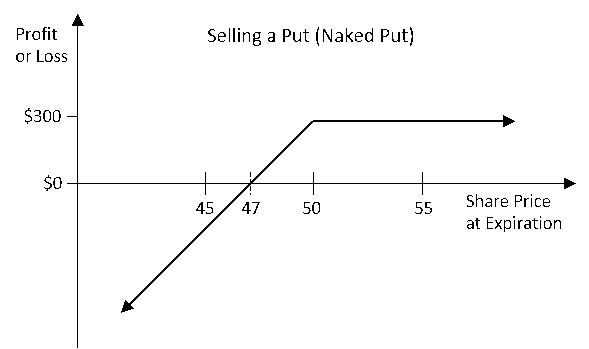

Now, let’s once again flip the script and go over what this trade would look like if we were on the opposite side, as the seller of the put option.

Selling Puts

Just as with calls, when we switch sides and become the seller of a put option, as opposed to the buyer, the payoff scenario reverses. In this case we have a smaller, limited upside, with the potential for larger losses.

The $300 that changed hands as part of this contract now goes to the option seller as premium. This is the most that the put seller can hope to make, and he or she will make this full amount if shares of ABC stock trade at or above $50 at expiration.

At a share price of $50 or above, the put seller gets to keep all the premium he received because the put option will expire worthless. As we discussed, from the put buyer’s perspective, there is no reason to exercise his right to sell shares at $50 if he can sell those same shares for that or higher in the marketplace.

Next, notice that the breakeven point from the put seller’s perspective is also $47. Since the put seller has obligated himself to purchase 100 shares at $50 (he has sold the right for someone else to sell him 100 shares at $50 per share), he would need to be able to sell those shares for $47 in the marketplace order to break even [($47 - $50) x 100 = -$300].

The seller of a put option is taking a neutral to bullish stance on a stock, and as a result, will suffer losses if the share price of the underlying stock (in this case ABC) heads lower. At a share price less than $47 at expiration, the put seller begins to accumulate losses.

The worst case scenario for a put seller is to have the underlying security go to zero. This would result in the put seller being forced to purchase 100 shares, which are essentially worthless (they have a market price of zero), at $50 per share.

The unprotected nature of this trade is why selling a put all by itself can be a dangerous proposition. This is why it’s called a “naked” put. But interestingly, and this is important - selling a naked put entails no more risk than owning the underlying stock. In either case the stock could go to zero, which would result in maximum losses. In the put seller’s favor is the fact that he or she at least earned some premium (in this case $300) which helped to offset some of the losses.

As promised, in the next few segments we’ll discuss how to hedge away some these excessive risks using either a position in the underlying stock, or another option contract.

But for now, let’s summarize what we need to keep in mind about selling put options:

* It’s a strategy for when we are neutral to slightly bullish on a stock

* There is limited upside (the premium collected)

* There is a large but limited downside (if the underlying stock price falls to zero, the put seller will suffer losses similar to that of someone who owns the stock outright)

At this point hopefully you now understand what a put option is, and how the benefits, rights and obligations vary between the buyer and seller, based on the terms of the contract.

Now that we’ve covered the basics of buying/selling both calls and puts, we can move on to some of the factors that affect option prices, beyond the value of the underlying stock. We’ll do this in our next segment. After that, we’ll begin to attack specific option strategies.